Energy crisis: who is most vulnerable and why

8 MAY, 2026

By Schroders

By Irene Lauro, Senior Economist for Europe and Climate Specialist at Schroders

The energy crisis triggered by the closure of the Strait of Hormuz is reverberating across the global economy, and the full extent of its impact remains unclear, likely bringing complex consequences. The energy crisis unleashed by the closure of the Strait of Hormuz at the end of February 2026 is rippling through the world economy, and the total magnitude of its effects is still uncertain, with potentially far-reaching implications. This marks the second major energy crisis of the 2020s, at a time when many economies are still adapting to the first one, triggered in 2022 by Russia’s invasion of Ukraine.

Looking back at similar crises in the 1970s highlights the potentially deep consequences that can persist for decades. As nations and trade blocs rush to strengthen their energy supplies, new policy strategies are being adopted, with effects spreading across all sectors and asset classes. For investors, this creates new risks but also opportunities. For example, it could lead to a reassessment of policies related to hydrocarbon projects. At the same time, it could strengthen the case for a “decarbonization dividend,” since locally produced low-carbon energy would reduce dependence on imports.

Asian economies are likely to be the hardest hit by this crisis. They import more than 80% of the oil and gas shipments that pass through the Strait of Hormuz, making them highly vulnerable to supply disruptions and sharp price increases. Europe’s direct exposure is smaller. It imports only around 5% of its crude oil and 13% of its liquefied natural gas (LNG) through the Strait, but it is far from insulated. Energy prices are set in global markets, and competition for LNG cargoes — with Europe and Asia bidding head-to-head — could keep prices elevated for longer.

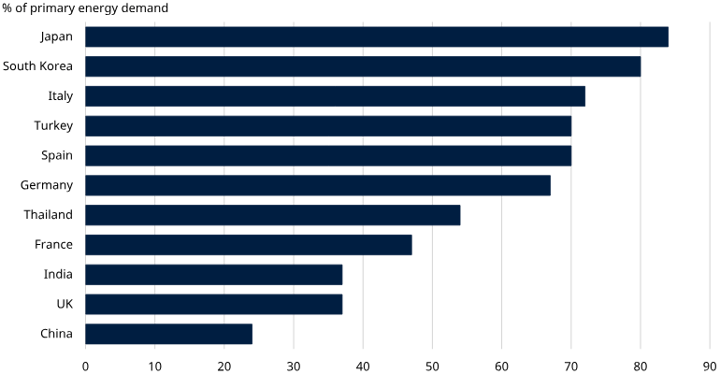

Vulnerability is greatest where dependence on imports is highest. In Asia, Japan appears to be the country most exposed to rising fossil fuel prices, importing 84% of its energy demand, followed closely by South Korea at around 80%. In Europe, Spain, Italy, and Germany import more than two-thirds of their energy. With trade routes disrupted and energy costs rising, these economies face a classic stagflation threat: weaker growth combined with renewed inflationary pressure.

Net fossil fuel imports

Source: EMBER, Schroders Economics Group, April 2026.

A crisis accelerating structural change

Energy crises rarely end with a simple return to previous prices. More commonly, they force a rethink of energy strategy, as governments and companies urgently reassess resilience, diversify supply, and accelerate investment in energy systems that are less volatile and less exposed to geopolitical disruption. We have seen this pattern before.

History repeats itself: the oil crises of the 1970s

The 1973 oil embargo and the subsequent 1979 supply crisis exposed a deep vulnerability at the core of industrialized economies: overwhelming dependence on imported fossil fuels from geopolitically unstable regions. The result was not merely a temporary rise in fuel prices, but a structural shift in the energy policies of many oil-importing nations.

In the early 1970s, fuel consumption was extremely high and industry was booming, until supply was abruptly restricted. Governments were forced to implement urgent measures to curb consumption, and households and businesses had to change their behavior. The lesson was clear: when energy security is threatened, policy responses can be swift and far-reaching.

Different responses; different outcomes

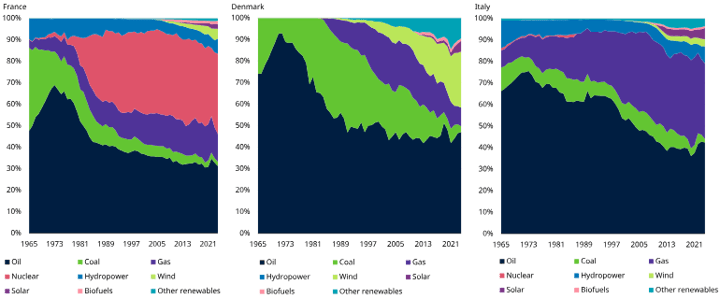

France and Denmark demonstrate that rising fossil fuel prices can drive long-term energy transitions, making energy security a national priority and favoring domestic supply over imports.

France responded decisively by launching the Messmer Plan as a direct reaction to the oil crisis. The result was the fastest large-scale nuclear expansion in modern history, reshaping the country’s electricity system for decades.

Denmark followed a different path. It intensified exploration in the Danish sector of the North Sea, achieving natural gas self-sufficiency in 1984 and oil self-sufficiency in 1993. At the same time, Denmark became one of the pioneering economies in commercial wind energy during the 1970s. This helped lay the foundations for an industry that later gained global importance, with Danish manufacturers and component suppliers playing a central role in wind turbine supply chains.

Italy offers a very different example. Rather than significantly reducing its dependence on imported fossil fuels, it continued relying heavily on energy imports, pursuing a policy focused more on diversification: shifting from oil imports toward gas imports, mainly from North Africa and Russia. This period saw a broader shift across Western Europe toward Russian gas, with pipelines linking the Soviet Union to Western Europe and laying the foundation for a dependence that grew substantially in later decades. By 2021, Russia supplied approximately 45% of the EU’s total gas imports (including both pipeline gas and LNG). This dependence became a critical energy security issue following Russia’s invasion of Ukraine in 2022, prompting a sharp decline to 19% by 2024. Europe was once again forced to diversify its energy supply, partially replacing Russian gas with U.S. LNG.

Energy consumption by source

The decarbonization dividend: security and sustainability

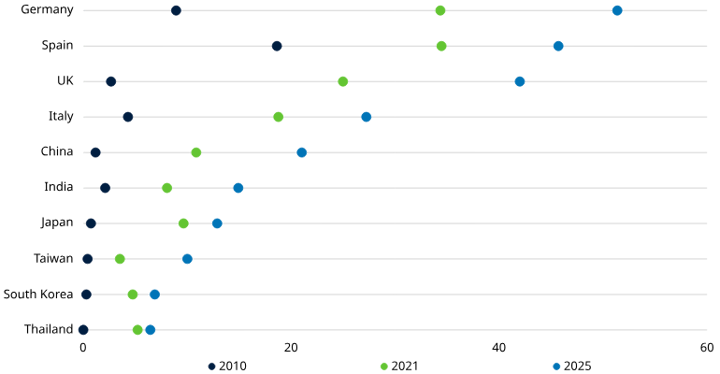

Russia’s invasion of Ukraine highlighted that energy security is another major force driving the transition away from fossil fuels. Renewable energy is not only a pathway to reducing emissions; it also limits dependence on imports.

The surge in gas prices following the Russian invasion prompted another rethink of energy strategy, and the EU committed to gradually eliminating its dependence on Russian fossil fuels, diversifying gas supplies, and accelerating the deployment of renewable energy.

Share of electricity generation from renewable sources (%)

Source: EMBER, Schroders Economics Group, April 2026.

In Europe, the momentum has been significant. In 2025, wind and solar power generated more electricity in the EU than fossil fuels for the first time, reducing Europe’s vulnerability to external crises such as the one currently affecting many economies. Asian countries were also hit by the 2022 energy crisis due to rising energy prices. As shown in the chart above, this led to a greater share of renewable energy in electricity generation across Asian economies, as the relative cost advantage of renewables over oil and gas became increasingly evident.