European retail bankruptcies on the rise

15 JUL, 2024

Author: Claudia Aquino, analyst at Scope Ratings

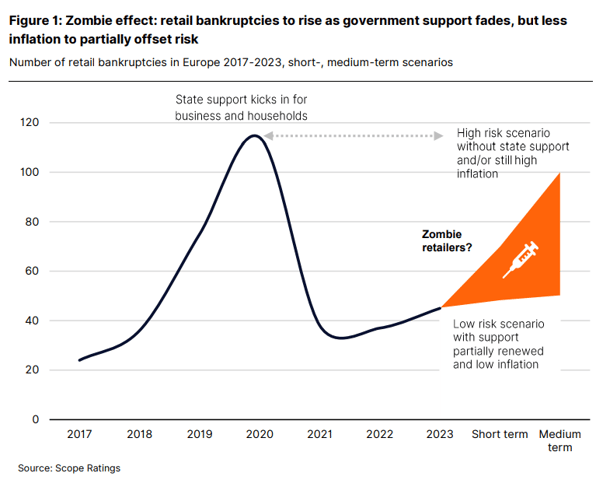

This year, credit risk remains elevated in the European retail sector, especially in the discretionary segment. Moreover, there are no signs of a reversal of last year's upward trend in corporate bankruptcies in 2024, after defaults increased in the first quarter.

The outlook for more corporate bankruptcies in the sector follows the large withdrawal of direct and indirect public support for companies during last year's pandemic and energy crisis, which, as in other sectors, supported many companies that would otherwise have gone bankrupt.

The impact is visible in the sharp decline in bankruptcies in the sector in 2021 compared to the previous year and their subsequent increase, especially in 2023, in a trend that extended into the first quarter of this year.

We expect defaults to increase further in the second half of the year.

E-commerce continues to disrupt traditional retail activity and the rising cost of living, with inflation slowly receding from last year's highs, is putting a strain on the financial results of many companies in the sector. All this against a backdrop of declining public support.

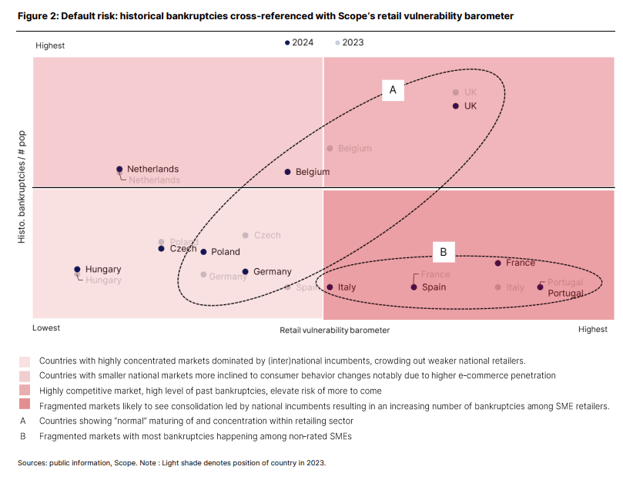

Scope's retail vulnerability barometer analyses the outlook for retail default in Europe.

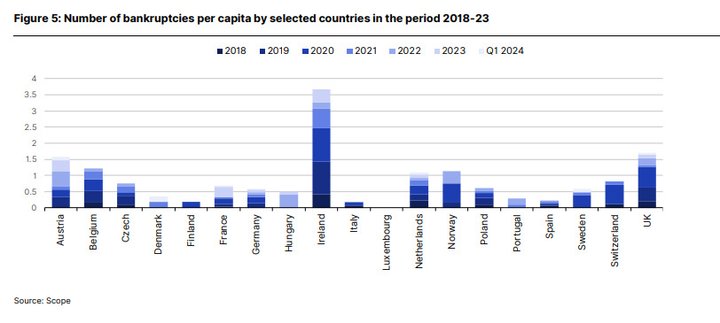

The risks facing retailers today are unevenly distributed across Europe, a phenomenon reflected in our analysis of bankruptcy rates over the past six years and in Scope's Retail Vulnerability Barometer (RVB). Fragmented markets, such as France and Portugal, and ultra-competitive markets, such as the UK, are where vulnerability to retail default remains particularly high.

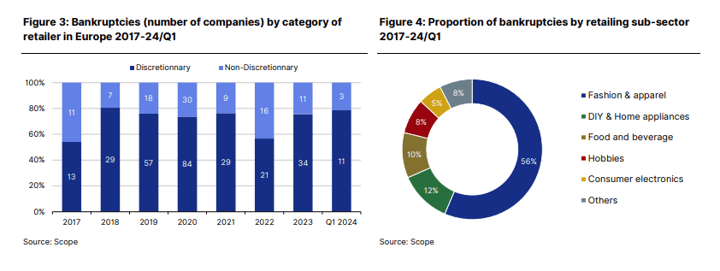

Credit risks vary across the different sub-sectors

The fashion segment accounts for 57% of all bankruptcies in our dataset, partly reflecting the sector-specific risk. Shops are often located on or near high streets, in close competition for visibility and footfall, and often need integrated or nearby warehouses to ensure continuous supply of goods.

Property leasing costs are therefore relatively onerous compared to other retail sub-sectors.

Other discretionary retailers - DIY shops and appliance sellers - face similar, albeit less severe, risks and have slightly lower bankruptcy figures than their fashion counterparts (13% of the total). Businesses in this category tend to have seasonal sales - think garden centres and DIY specialists who rely on summer trade - which makes cash flow erratic.

They are also vulnerable to competition from multi-product online retailers for whom seasonality is not an issue, such as Amazon.com, Germany's Otto and France's Cdiscount.

Food retailers still top the list of vulnerable companies

Food retailing ranks relatively high on our list of bankruptcies. Some companies in our sample were long-established businesses, such as Iceland, the UK frozen food retailer that filed for bankruptcy in several European countries in 2023, and Pepco, which filed for bankruptcy in Austria in February 2024.

Other troubled companies, such as Flink, which filed for bankruptcy and exited Austria, were relatively new to the market. They were mostly home delivery and online grocery services that boomed during the pandemic, but lost their appeal afterwards, and have struggled to cope with high operational and delivery costs.

Moreover, the expansion of these new food retail companies is proving difficult as inflation has accelerated, borrowing costs have risen and the big players have countered with competitive product offerings. There is also the continuing competition from discount chains. Lidl and Aldi have gained significant market share in the UK and have gained popularity in the US in the wake of rising food prices.