European telecoms: leverage points to decade lows as the decline in capital investment continues

12 JAN, 2026

By Nidhi Marwaha and Rohit Nair, Corporate Ratings Analysts at Scope Ratings

European telecommunications operators are on track to record their lowest level of leverage in a decade, as the fixed capital investment cycle is set to continue declining over the next two years, provided there are no major expenditures on mergers and acquisitions or technology.

Modest revenue growth and a strong reliance on debt-funded capital investment have resulted in leverage at most telecom companies remaining at moderate to high levels in recent years. We expect average capital expenditure to fall to 16% of revenues in 2025–2027, from a peak of 25% in 2021, when spending on 5G spectrum and licenses reached its highest point. Forecasts for Scope’s rated portfolio of ten European telecom companies suggest that deleveraging will be a priority. We anticipate that aggregate net debt to EBITDA will decline to around 2.5x by 2027, from 2.7x this year and a peak of 3.3x in 2021/2022.

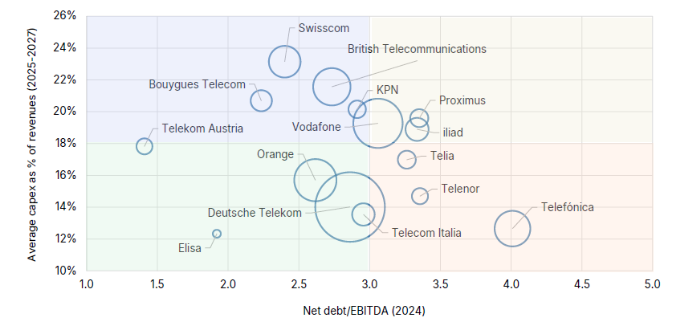

Chart 1: Debt reduction: a group of European operators could significantly reduce leverage

Capex/revenues 2025–2027, net debt/EBITDA 2024, average annual capex 2025–2027 (bubble size)

Image containing diagram

Source: Capital IQ, Scope estimates.

5G spectrum auctions accounted for between 7% and 10% of capital investment in 2019–22. European operators also increased capital spending to upgrade their networks for 5G and fiber-to-the-home. By the end of 2024, capex had enabled European operators to achieve 5G coverage of 87% of households, gigabit-capable coverage of 82.5%, and FTTH coverage of 70.5%, approaching the EU’s 100% target for 2030.

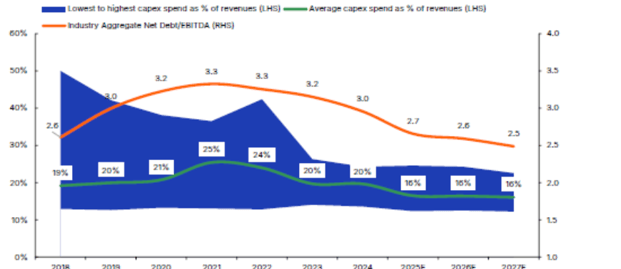

Chart 2: The decline in telecom investment in Europe promises greater deleveraging

The sector faces an investment trough toward the end of the decade following the debt and investment peaks of 2021–22.

Based on a sample of 15 large European telecom companies, we expect the reduction in average capital spending—24% lower in 2025–2027 compared with 2020–2024—to persist through 2028–2029, freeing up close to €30 billion in cash per year. The combination of normalized capex and growth in free operating cash flow (FOCF) will create an opportunity for issuers to improve their credit profiles, provided they balance discretionary spending (for example, higher shareholder remuneration and increased M&A activity) with debt repayment. This is important, as deleveraged balance sheets will position companies well for the next wave of capex needs for 6G, which is likely to pick up toward the end of the decade.

Opportunity to improve credit profiles and shareholder remuneration

With lower capital investment requirements, we expect most operators to allocate between 60% and 100% of free operating cash flow to dividends and share buybacks over the next two to three years, leaving some room for deleveraging and acquisitions in segments such as fiber-optic networks, enterprise services and cybersecurity, and artificial intelligence.

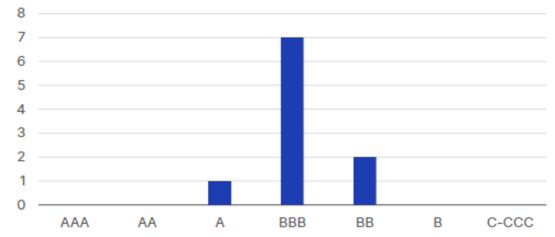

The credit profiles of telecom companies rated by Scope are concentrated in the BBB category and have shown a consistently positive trend over the past two years. We believe credit profiles will remain stable or improve further in the coming fiscal years.

Chart 3: Scope of European telecom companies: distribution of ratings by category

Measured by number of ratings

Source: Scope