Eurozone Equities: a differentiated approach for portfolios

29 MAY, 2026

By Joao Saraiva from Vanguard

- Exposure to eurozone equities isolates monetary, fiscal, and earnings dynamics that would otherwise be diluted in pan-European indices.

- Decisions regarding index composition create significant differences in country, currency, and sector exposure among European equity ETFs.

- Portfolio managers should pay close attention to index scope, country selection, and macroeconomic consistency—details that can materially influence performance across all phases of the economic cycle.

Structurally Coherent Equity Exposure

At its core, the eurozone represents a specific combination of shared monetary policy, increasingly coordinated fiscal frameworks, and a high degree of economic integration. For equity investors, this coherence matters. Eurozone companies operate under a single-currency regime overseen by the European Central Bank, directly influencing financing conditions, earnings translation, and valuation dispersion.

From a portfolio perspective, this environment creates a more clearly defined macroeconomic exposure than broader European indices, which combine eurozone and non-eurozone markets. Equity returns are less affected by intra-European currency noise and more directly linked to eurozone growth, inflation, and economic policy outcomes. For portfolio managers working with currency exposures, regional risk budgets, or factor allocations, this distinction can improve index transparency and exposure intentionality.

The FTSE Eurozone Index is explicitly designed around this premise. It includes large- and mid-cap companies domiciled in countries that have adopted the euro, aligning equity exposure with the region’s monetary and macroeconomic framework. This is not a tactical strategy, but rather a structural asset allocation decision.

Differences Between Eurozone Exposure and “Core Europe” ETFs

Many “core Europe” equity ETFs track broader benchmarks such as the MSCI Europe or the STOXX Europe 600. These indices include major non-eurozone markets—primarily the United Kingdom, Switzerland, Sweden, and Denmark—each with its own currency, central bank, and economic policy dynamics. This can significantly alter both country weightings and sector composition, often in ways that are not immediately apparent to investors.

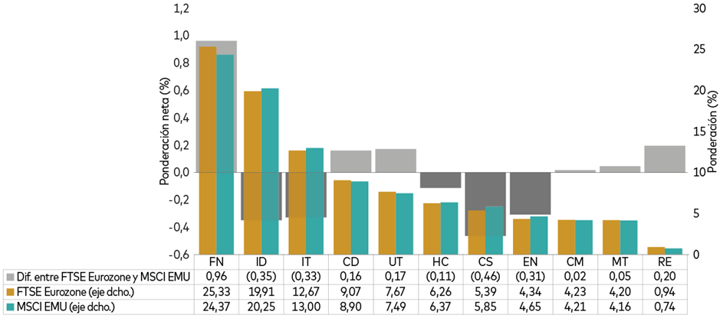

For example, benchmarks that include UK and Swiss equities tend to increase exposure to financials, pharmaceuticals, and global exporters with substantial non-European revenue streams. By contrast, eurozone-focused indices generally place greater weight on sectors more closely tied to the domestic economy, such as industrials, banking, and consumer cyclicals, whose earnings are more directly linked to eurozone activity. This can lead to a differentiated factor and earnings profile.

This divergence becomes particularly relevant when European equities are used as a core building block rather than a standalone allocation. A eurozone ETF can complement global developed-market exposure without inadvertently increasing exposure to UK or Swiss equities already present elsewhere in the portfolio. This helps avoid unintended concentration and may improve regional balance.

Eurozone Focus Influences Sector Weightings

FTSE Eurozone Index vs. MSCI EMU Index by weighting

Why Index Design Matters: Country Selection Is Key

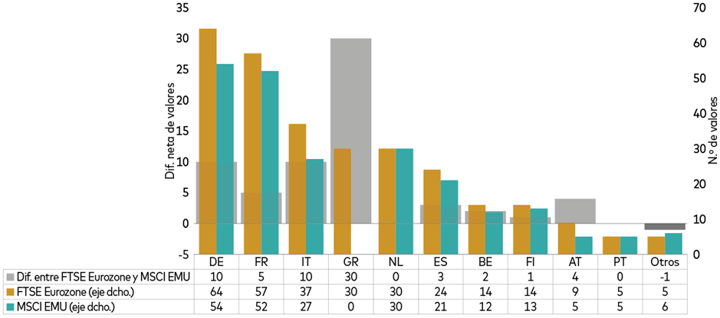

One of the more technical—but portfolio-relevant—features of the FTSE Eurozone Index is the inclusion of Greece. Greece is a full member of the eurozone but is excluded from many European equity benchmarks due to classification or liquidity criteria.

The FTSE Eurozone Index includes Greek equities, resulting in a small but deliberate allocation. Although Greece represents a modest weighting, its inclusion reflects an approach focused on economic definition and completeness rather than exclusion based on legacy classification standards. If an investor seeks exposure to eurozone equity risk, excluding a eurozone country constitutes an artificial omission. Over time, these details can matter, particularly if smaller markets undergo structural change, capital-market deepening, or cyclical recoveries.

This is not about expecting enhanced returns specifically attributable to Greece. Rather, it reflects a philosophy that prioritizes completeness and economic definition over inherited exclusions—an approach aligned with disciplined portfolio construction.

Country Allocation Makes a Difference

FTSE Eurozone Index vs. MSCI EMU Index by number of constituents

Key Considerations for Portfolio Managers

For portfolio managers, the question is not whether to invest in Europe, but how. When selecting an index—and therefore an ETF—several considerations should be evaluated:

- Macroeconomic alignment: Does the index reflect a single monetary and economic policy regime, or multiple regimes?

- Currency clarity: Is exposure to different currencies deliberate or incidental?

- Overlap control: Does the index duplicate exposures already present through global or regional allocations?

- Index completeness: Are all eurozone members fully represented, including smaller markets such as Greece?

Each of these factors can influence allocation behavior across economic cycles. Eurozone exposure may be particularly suitable for investors who frame investments in terms of regional blocks, risk-factor decomposition, or macroeconomically driven portfolio construction.