The evolution of ESG factors: this is how sustainable practices are changing in developed credit markets

26 JUN, 2024

Author: Samuel Grantham, Investment Director at abrdn

This year marks the 20th anniversary since the ESG environmental, social and governance concept was introduced in the influential report “Who Cares Wins” by the United Nations Global Compact. In the two decades since then, ESG issues have become one of the main concerns in investment matters. During this period, the application of the ESG concept has evolved significantly. Below, we outline some of the recent changes we have observed in developed credit markets.

We see three distinct but interrelated trends in the recent application of ESG analysis: the growing role of social and environmental considerations; the role that regulation is playing in driving -and shaping- demand in credit markets; and a shift from general exclusions to more refined approaches that allow sustainability-concerned investors to have a greater impact in the real world.

The G gives way to the S and the E

In the last two decades, ESG analysis has mainly focused on governance. The G in ESG is the most "conventional" element and its impact has been more easily understood. This has made it easier for investors to consider governance as the most important metric from a financial point of view. Strong governance practices are vital for the sustainability and long-term success of a company. Investors have focused on factors such as board composition, executive compensation, and risk management policies. These factors are considered to provide a picture of the overall health and stability of the company, so they have become important in credit analysis.

However, in recent years, investors have increasingly recognized the importance of environmental and social factors. In 2021, the rating agency Moody's noted that social factors were cited as the key element in 84% of ratings, largely due to the impact of Covid. In 2022, as the effects of Covid subsided, this figure dropped to 69%, but it was still much higher than in the years before the pandemic. In 2019, the comparable figure for private sector shares was 20%. 25% of the 2022 ratings that cited ESG factors as main factors mentioned environmental risks, which is more than double the 12% of mentions in 2021.

Together, these statistics suggest that the importance of social risks is gaining ground over governance ones and that environmental ones are gaining ground. Thus, in the current changing global landscape, the E and S within ESG are increasingly important drivers of long-term value creation and effective risk management.

The role of regulation

The growing importance of environmental and social factors is reshaping attitudes towards ESG investments, especially in Europe. The region's sustainability regulations surpass those of other developed markets, especially the American one. Non-compliance can reduce profitability and increase financing costs. It can also expose companies to changes in consumer preferences and stricter regulatory measures. Conversely, those that demonstrate excellence in sustainable practices can achieve better results. For fund managers like us, this represents a critical factor for generating returns and its importance is going to increase.

The tightening of ESG regulations is significantly affecting the cost of financing across all sectors. In the case of the oil and gas sector, uncertainty about the energy transition, including the risk of stranded assets, has led to a drop in long-term bond valuations compared to historical levels. In addition, the sector faces dubious credibility emission reduction targets and cases of "greenwashing". These challenges are compounded by doubts about the scalability and effectiveness of technologies such as carbon capture and storage. Meanwhile, investments in viable and scalable technologies, such as renewable energies, are often deemed slow and insufficient, hindering the sector's progress towards sustainability goals.

Although this change aligns with society's goals of promoting sustainability, there are implications that must be taken into account, especially for industries that facilitate the transition. In the utilities sector, for example, increased scrutiny over the use of fossil fuels in power generation, driven by regulations such as the EU's Sustainable Activities Taxonomy, is causing investors to move away from carbon-intensive companies. The emphasis on carbon intensity targets and benchmarks aligned with the Paris Agreement further intensifies this trend, redirecting capital towards lower carbon footprint alternatives.

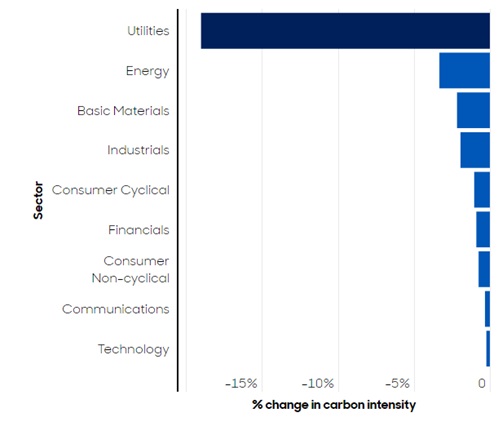

However, this regulatory impulse can have unintended consequences, especially if it causes investors to completely avoid high-emission sectors. There is a risk of penalizing companies that are leading the transition to cleaner practices, which could hinder progress towards sustainability goals. Public service companies that are actively investing in renewable energy infrastructures could face higher financing costs due to persistent links with fossil fuels. Despite this challenge, it is expected that the public services sector will achieve the most significant reduction in carbon emissions by the end of the decade, as shown in the following graph. Although some entities still depend on coal generation, many of the main public service companies are gradually phasing it out by 2030.

Graph 1: Percentage reduction of sectoral emissions by 2030 (scopes 1 and 2)

Although certain industries justify higher financing costs due to their adverse environmental impact, this approach risks stagnating the transition process and disincentivizing innovation in critical sectors. Thus, while regulation is fundamental to incentivize sustainable practices, it is essential to adopt a nuanced approach to ensure that the transition is effective and equitable across all sectors.

Beyond the screens

Exclusions have been a staple of sustainable investment for a long time. By excluding companies that do not meet certain ESG standards, sustainable fund managers aim to align their portfolios with the values of their investors. However, the effectiveness of this approach has been questioned. For example, when investors remove from their portfolios companies with an irregular environmental history, they abandon the possibility of directly influencing them, thus they may lose the opportunity to achieve real change.

Having said that, in recent times we have witnessed a shift towards a more holistic approach. Since 2020, ESG integration has surpassed negative selection as the most popular strategy in sustainable investing. By "ESG integration" we mean the inclusion of these issues in all analysis and investment decisions. Exclusions still have a place: they are not controversial in areas such as tobacco and gambling. But by adopting an integration approach, investors can avoid ruling out certain companies as unsuitable for investment based on retrospective data. In sectors where practices are improving, investors are increasingly looking beyond the blanket exclusion of companies lagging in ESG matters and towards a more nuanced awareness of these types of risks, with future hypotheses integrated into decision-making to complement investment logic.

Another way to look at it is through environmental and social impact. If those companies that are at the beginning of their "green transition" were abandoned by investors concerned about sustainability, they would have far fewer incentives to adopt environmentally friendly practices. Here it is important to consider the impact that fund managers can have. If you, as a sustainable investor, back a "pure and hard" renewable energy company, you are basically asking it to continue doing what it already does. On the other hand, if you invest in a cement manufacturer and encourage it to set up pilot plants with net zero emissions, your positive impact will be much greater.

In the same vein, investors could exclude steelmakers, due to their high carbon emissions. But steel is vital for the construction of clean energy infrastructure. Therefore, a company that is moving to a low-carbon steel production or, ultimately, to net zero emissions, is reducing its own emissions and helping to reduce emissions more generally by providing materials for renewable energy projects. If investors bet on them, they are promoting a positive direction.

One of the beneficiaries of the move towards integration has been EDP, a Portuguese public services company that sets and consistently meets ambitious emissions targets. As it currently generates 5% of its revenue from coal, it is not investable for strategies that operate with coal generation thresholds. But the listed company will gradually phase out its coal operations over the next two years and reduce its emissions by 98% compared to 2015 levels by 2030, when it should be one of the world's largest wind power producers. Therefore, investors can aspire to achieve a greater positive impact by having EDP in their portfolio than by excluding it. By supporting it, they are helping to accelerate the energy transition.

Focusing on those names that are near the start of their ESG journey also offers the prospect of higher returns. A recent Barclays study indicates that the highest returns come from companies that make the greatest improvements in sustainability, not those that already have a high ESG score. If a strategy focuses exclusively on ESG "champions", it may be missing important profitability opportunities.

The performance opportunity in data gaps

For credit investors, a final aspect is whether the same ESG standards can be usefully applied to all issuers. The differences between high-yield issuers and investment-grade issuers are particularly relevant here. High-yield issuers, which are often smaller or younger companies, may lack specialized ESG teams, green bond frameworks or resources to prepare sustainability reports.

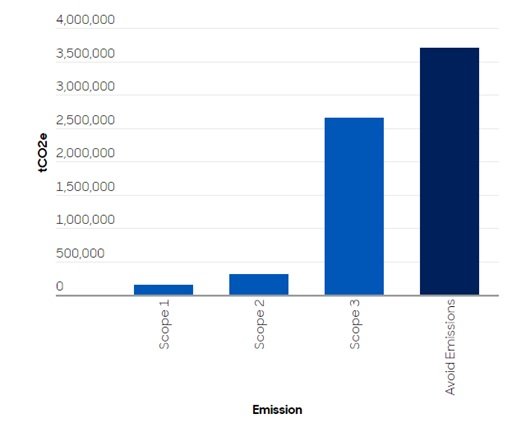

This means that companies committed to sustainability may go unnoticed by investors because they lack the means to demonstrate their ESG credentials. A recent example is Ardagh Metal Packaging, which produces highly recyclable metal beverage cans. Until very recently, the company was a laggard in its ESG disclosures. But it is very much aligned with sustainability principles, especially in the areas of the circular economy and waste reduction. In 2022, it is estimated that its recycling efforts prevented 3.7 million metric tons of CO2 equivalent emissions compared to virgin materials, as shown in the following graph.

Graph 2: Ardagh's metal packaging emissions (tCO2e)

This underscores the importance of ESG being more than a box-ticking exercise. In-depth analysis is an irreplaceable element. And investors who can uncover companies with good ESG practices, but whose disclosure is limited, have the opportunity to achieve better results by investing before the improvement in disclosure finally attracts greater market attention.

Healthy Evolution

Although the ESG concept has been criticized in some sectors, it enters its third decade in good health. However, as ESG investing matures, best practices continue to evolve. The market shows that investors continue to refine and improve their sustainable investment approaches to increase profitability, mitigate risks, and ultimately improve social and environmental outcomes for all.