Fixed Income Outlook for 2025

12 DEC, 2024

By Schroders

Authors: Julien Houdain, Global Unconstrained Fixed Income Director; Lisa Hornby, US Fixed Income Director; Abdallah Guezour, Emerging Market Debt and Commodities Director, Schroders

Global Outlook

Julien Houdain, Global Unconstrained Fixed Income Director, and Lisa Hornby, US Fixed Income Director

As we enter 2025, the calendar will change, but the driving forces in the markets will remain the same. The evolution of economic fundamentals and the impact of political changes on them will continue to be crucial.

Without a doubt, changes introduced by the incoming US administration will have a significant impact on the markets, but it is also important to note that fiscal plans in Europe, the UK, and China will play a key role in shaping the overall economic cycle and central bank strategies.

These factors will likely create a favourable environment for fixed income, benefiting both from broader economic trends and the elevated starting point for yields. Fixed income now earns its place in portfolios not only for its attractive income potential but also for its capital appreciation prospects and its ability to serve as a diversifying asset against more cyclical market segments.

First, let’s pause and take a look at the US economy before this year’s presidential elections. Growth was strong, inflation was improving (i.e., decreasing), and the labour market was near equilibrium. The economy had returned to balance, and the much-debated soft landing was occurring, a scenario in which economic growth slows but does not contract, and inflationary pressures ease. The key question for 2025 is: can this momentum be maintained?

There is a high level of uncertainty about economic policy as we approach 2025. Key themes on the US political agenda, such as tighter immigration controls, a more relaxed fiscal policy, fewer regulations for businesses, and tariffs on international goods, suggest an increasing risk.

These factors could dampen any improvements in core inflation numbers and might lead the US Federal Reserve (Fed) to halt monetary easing earlier than expected. In other words, we see the risk of a no-landing scenario increasing, where inflation remains sticky, and interest rates may need to stay higher for longer, although this is not our base case.

The likely impact of a Trump administration on economic growth is less clear. Firstly, as mentioned, it was already quite good. While it has the potential to improve, it’s worth noting that we are starting from a high base. Measures such as reducing regulation and improving fiscal impact could foster this. These measures include making smarter investments in key areas such as infrastructure, education, and healthcare to stimulate economic growth, create jobs, and ensure that public funds provide the best benefits to citizens. However, stricter immigration policies that result in fewer available workers or significant disruptions in global trade due to increased tariffs could, in contrast, hinder growth.

The pace, scale, and sequence of these various policies will play a key role in guiding the direction of the markets.

Although the potential growth and inflationary momentum from US government policies have led us to increase the risks of a no-landing scenario, bond valuations have improved to offer more cushion against these risks.

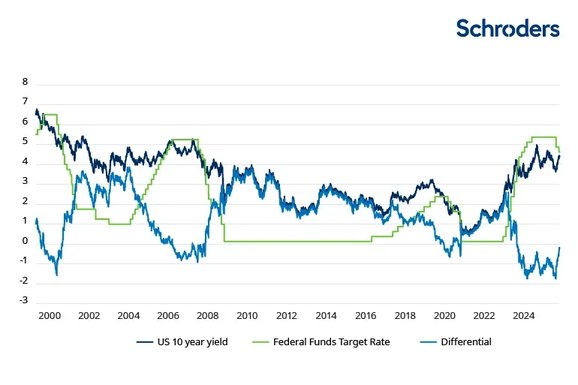

We are likely to begin the year with US Treasury yields on 10-year bonds above 4%, and real yields (net of inflation) above 2%, an attractive income level we haven’t seen since the 2008 financial crisis.

Chart 1: Official interest rates and 10-year yields are realigning, removing the disincentive to holding bonds

Furthermore, with the decline in official interest rates, the negative carry (when the bond yield is lower than the financing cost of holding that bond position), which has been a hindrance to bond ownership in recent years, has disappeared for all maturities except the shortest.

Additionally, at lower inflation levels, the diversification benefit of bonds increases, providing a more efficient hedge against weaknesses in cyclical assets. Bonds also appear cheap compared to alternative assets, with current yields exceeding the expected returns of the S&P 500.

With this dynamic, bonds can serve a dual function in a portfolio: they can provide an attractive income source and create resilience in a diversified portfolio.

Chart 2: Fixed income yields are attractive compared to equity yields

Elsewhere in the world, the worsening trading environment will amplify existing weakness in the industrial cycles in both China and Europe. We believe more political support is needed to counteract this, particularly if further signs of slowdown are observed in the services sector. The less fiscal policy does, the more monetary support will be required.

So far, the policy response has been moderate in both regions, but the upcoming German general elections could bring a shift towards a significant reevaluation of fiscal policy’s role in Europe. It remains to be seen which path will be chosen.

At the same time, in the UK, there have been several changes in government policy, notably with the expected Labour Party Budget. The surprising fiscal boost complicates matters for the Bank of England, delaying the expected date for inflation to return sustainably to target. That said, we believe that market valuations largely reflect this impact on inflation, and bets on rate cuts have been significantly reduced in recent times. This revaluation makes gilts attractive, despite the ongoing macroeconomic volatility. This disparity in fiscal trajectories creates relative value opportunities in bonds, currencies, and asset allocation. Being flexible and proactive in managing these investments will be key to capturing the excess returns these opportunities offer.

Cautious on credit, but finding value in securitised assets

A starting point of reasonable valuations, strong growth, and central bank easing has created a perfect cocktail in 2024 for cyclical assets, such as corporate bonds. Yields have been good, especially in the high-yield space.

This year, we have seen credit spreads tighten, basically the difference in yield between safe investments and riskier ones. Many segments of the market, including US investment-grade and high-yield companies, are now trading with narrower spreads than at any point since the pandemic. This trend suggests that investors are increasingly confident and willing to invest in higher-risk assets. This spread tightening has been driven by a combination of solid economic growth, strong demand for fixed income, and expectations for a continued favourable macroeconomic backdrop.

We expect credit fundamentals to remain solid in 2025. This, combined with high yields and steeper yield curves (the yield curve steepens when the difference between long-term and short-term interest rates widens), should continue to attract flows into credit.

Valuations are likely to hold, though the scope for further compression is more limited. In other words, while credit spreads may remain expensive, the scope for them to widen further is limited. Therefore, we are more cautious with these assets in multi-sector portfolios and have focused on shorter-duration corporate bonds when they provide good income with limited duration risk (i.e., limited sensitivity to changes in credit spreads).

Among the various industrial sectors, we prefer banks, as their valuations, in our view, have been more compelling than those of industrials, capital positions remain solid, and steeper yield curves should improve banks’ net interest margins.

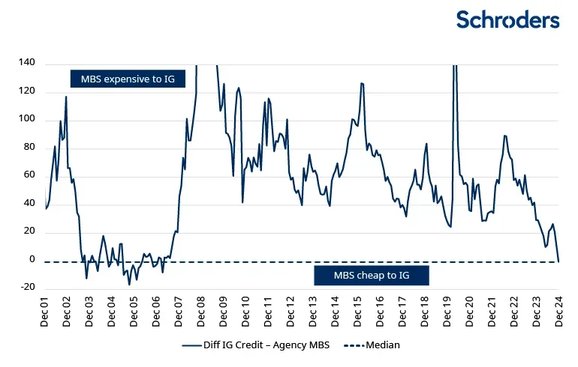

Better opportunities exist in securitised assets, such as agency mortgage-backed securities (MBS). Agency MBS are issued by government-backed entities and are backed by a pool of mortgages. Like investment-grade corporate bonds, these high-quality assets continue to provide a good income stream, but with historically attractive valuations. Demand for this sector is also likely to increase, given the less stringent regulatory environment in the US, which allows US banks to purchase these securities in their asset portfolios.

Moreover, as the Federal Reserve lowers interest rates, part of the $7 trillion in record money market balances in the US is likely to find its way into this segment of the fixed income universe. We believe these types of assets have greater capital appreciation potential and pose less idiosyncratic credit risk. As such, they remain our preferred choice within asset allocation.

Chart 3: Agency mortgage-backed bond valuations are more attractive than investment-grade credit

Finally, we are in favour of incorporating a certain degree of liquidity. With the valuations of most credit sectors at the tightest levels in history and political uncertainty quite high, it is very likely that periods of volatility will provide a good opportunity to deploy capital at less expensive levels. We are incorporating this liquidity in several ways, such as through high-quality short-term asset-backed securities, short-term corporate bonds, and US Treasury securities.

Emerging Market Debt

Abdallah Guezour, Head of Emerging Market Debt and Commodities

Emerging market debt (EMD) showed relative resilience in 2024, despite the pressures from rising yields on developed market government debt, geopolitical instability, uncertainty surrounding the US elections, and concerns about China’s growth.

A significant divergence in performance was observed between hard-currency debt (debt denominated in a stable currency such as the US dollar) and local-currency debt (debt denominated in the issuer’s local currency). Hard-currency debt, both sovereign and corporate, offered reasonably attractive total returns. This was due to the high yields generated by high-yield issuers—those typically with lower credit ratings, indicating a higher risk of default compared to investment-grade bonds.

Conversely, local-currency debt, which performed better in 2023, underwent a significant correction due to currency weakness and the rise in government debt yields, particularly in Brazil and Mexico, where concerns over fiscal policy have affected investor confidence. However, as international investors invest relatively little in local debt markets, these concerns may be somewhat exaggerated and already reflected in the lower valuations of local government debt.

Optimism Amid Uncertainty

Looking ahead to 2025, despite the current global uncertainty and the specific challenges of some countries, the trend of narrowing spreads between emerging market sovereign and corporate bonds is expected to continue. This means that the difference in yields (or interest rates) between these bonds and safer investments, such as developed market bonds, is shrinking, indicating growing investor confidence in EMD.

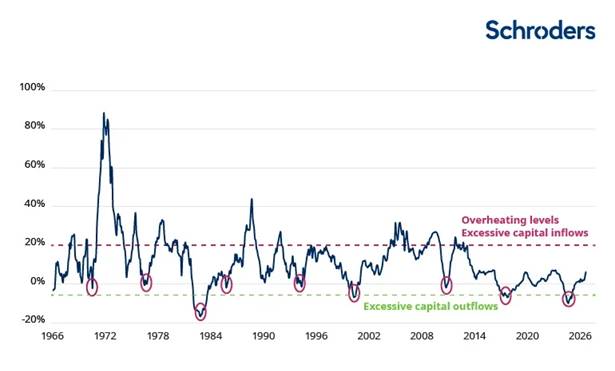

This optimism is largely driven by encouraging signs of growth in emerging markets and the strong financial health of many of their issuers. Additionally, the increase in foreign exchange reserves in emerging markets, highlighted in Chart 4, underscores the positive impact of the macroeconomic adjustments made in recent years.

CHART 4: Annual Growth in Foreign Exchange Reserves (Year-on-Year %)

Although these improvements are already reflected in the historically tight spreads of investment-grade emerging markets, attractive opportunities can still be found in the high-yield sector. Countries such as Argentina, Egypt, Nigeria, Ivory Coast, Senegal, Sri Lanka, and Pakistan are examples of nations still offering attractive sovereign spreads, while continuing to make good progress with their macroeconomic adjustments after recent crises.

Assessment of Strengths, Challenges, and Opportunities in Emerging Market Companies

Emerging market companies are also entering 2025 from a strong position, as for the first time in over a decade, they have received more credit rating upgrades than downgrades. This sector is likely to benefit from expectations of a resilient US economy in 2025, accommodating domestic and international capital markets, and still-healthy corporate balance sheets, as credit metrics are generally stronger than pre-crisis levels. As a result, default rates are expected to continue improving and to fall to a healthy 2.7% in 2025, down from the current level of 3.6% and the long-term average of 4.4%.

Although macroeconomic conditions are expected to remain favourable in 2025, the new Trump administration promises to bring an uncertain investment and operational environment for emerging market companies. Sector selection will be crucial. Among the emerging market corporate sectors facing scrutiny from the new administration are the automotive, electric vehicle battery manufacturers, chip makers, and Chinese tech companies.

On the other hand, depending on whether tariffs are applied and how they are ultimately implemented, investment in nearshoring—i.e. relocating business processes or services to a nearby country—could continue to benefit companies in countries like Mexico and India. Ukrainian companies could also stand to gain significantly if a ceasefire with Russia is achieved.

Local Emerging Market Debt: Preparing for Currency Risks and the Evolution of Global Trade

Finally, after the revaluation of local emerging market debt in 2024, this sector is beginning to offer even more attractive re-entry opportunities. Local emerging market yields look very appealing from a valuation standpoint, as real yields (the annual return on an investment, adjusted for inflation) remain at historically high levels in several emerging countries.

We expect inflation in emerging markets to remain well-controlled, mainly due to deflationary pressures from China and the expected decline in global energy and agricultural prices, resulting from oversupply in these commodity markets.

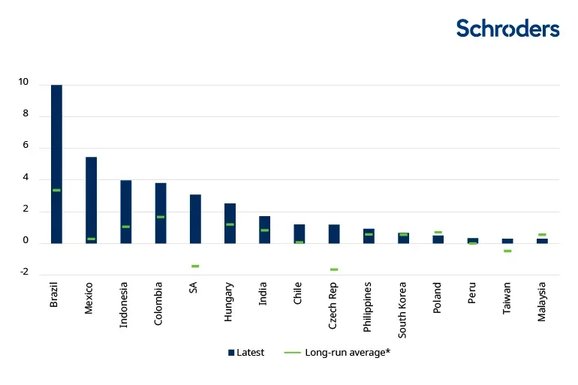

Recent fiscal concerns in several emerging markets have already been reflected in what investors expect from official interest rates and how yield curves are taking shape. Chart 5 illustrates that expected inflation-adjusted interest rates, known as ex-ante real rates, in major emerging markets are currently much higher than in the past. This suggests that investors are pricing in the potential impact of these fiscal challenges.

There is renewed focus on fiscal stability in countries like Brazil, where recent market challenges are encouraging more disciplined policies. Yields on ten-year local government debt in Brazil (12.8%), Mexico (10%), Colombia (10.7%), South Africa (10.4%), Indonesia (6.9%), and India (6.9%) are well-positioned to provide potentially high returns in 2025, making them attractive options for income generation and portfolio diversification.

However, it is important to consider active currency risk hedging in these local fixed-income markets, especially given the current strength of the US dollar and the potential for a new global trade war following the inauguration of the new Trump administration in early 2025.

CHART 5: Ex-Ante Real Rates in Emerging Markets - One-Year Market-Implied Official Interest Rate - Consensus One-Year Inflation Forecast