Global dividends poised for another strong year, though H2 growth may moderate

13 OCT, 2025

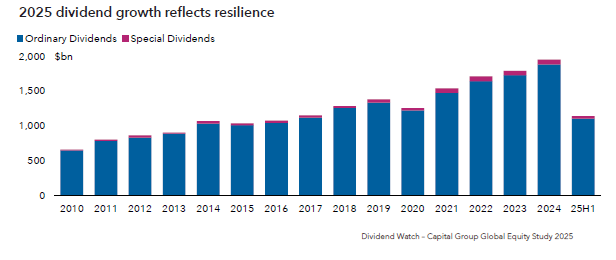

After a solid first half, 2025 is shaping up to be another good year for global dividends. The United States, where payouts are distributed evenly across quarters, appears set to maintain the current encouraging trajectory. Momentum is also evident in Japan, among Spanish utilities, in Taiwanese technology and shipping, and across Singaporean banks.

Where momentum is building

Regional and sector dynamics remain broadly supportive. In the U.S., the even quarterly cadence of distributions underpins steadier visibility into the second half. Japan continues to exhibit market-wide resilience on payouts, while Spanish utilities add defensive income support. In Asia, Taiwanese technology and shipping stand out as bright spots, alongside sustained strength from Singapore’s banking sector.

Why growth may slow in H2

Special dividends have remained high over the past four years but were slightly lower in the first half of 2025. By their nature they are unpredictable, and long-term averages suggest they will be lower year over year in the second half, weighing on overall growth. Seasonality also shifts the mix toward regions where dividend growth is currently slower—specifically the UK, China, and Australia—making it reasonable to expect a softer growth pace in H2 versus H1. On the currency side, if the U.S. dollar holds around current levels through the remainder of the year, it would continue to provide an FX tailwind to headline income totals.

Companies with a growing stream of income that accumulates over long periods of time offer real advantages that are often not apparent to short-term investors. Over the long term, we observe that the returns of companies that pay dividends are attractive and exhibit lower volatility. Companies are often tested in various economic conditions, including major market events such as the global financial crisis and, more recently, the pandemic. Companies that can consistently increase their dividends over the long term remain attractive investments.