GMO’s 7-Year forecast: Deep Value and Small Caps lead in a low-return world

24 JUL, 2025

By Joanna Piwko from RankiaPro Europe

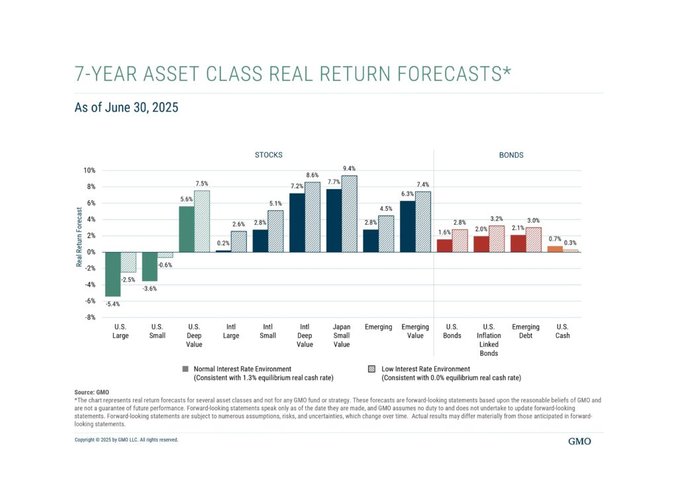

GMO has released its latest 7-Year Asset Class Forecast as of 30 June 2025, offering a comprehensive outlook on expected real returns across global equities and fixed income markets. For institutional investors, asset allocators, and fund selectors across Europe, the forecast offers timely insights amid a complex macro backdrop.

The forecast is built around two structural regimes: a normal interest rate environment (anchored to a 1.3% equilibrium real cash rate), and a low-rate environment (0.0% real cash rate). Here, we focus on GMO’s base case—the normal interest rate scenario—which reflects their long-term expectations based on historical mean reversion and valuation models.

Equities: Value, Small, and Emerging Markets Take Center Stage

GMO’s model continues to favor equity markets with lower valuations and more attractive fundamentals, with a clear tilt toward deep value, small-cap, and emerging market segments:

| Asset Class | 7-Year Real Return Forecast (Normal Rate) |

|---|---|

| Japan Small Value | 7.7% |

| International Deep Value | 7.2% |

| Emerging Value | 6.3% |

| U.S. Deep Value | 5.6% |

| Emerging Markets Broad | 2.8% |

| International Small | 2.8% |

| International Large | 0.2% |

| U.S. Small | -3.6% |

| U.S. Large | -5.4% |

Japan Small Value tops the chart with a 7.7% annualized real return forecast—highlighting deep undervaluation, corporate governance improvements, and demographic tailwinds. International Deep Value and Emerging Value follow closely, reflecting global dislocations in price-to-fundamentals metrics.

Notably, U.S. equities remain the most overvalued in GMO’s model, with U.S. Large Caps expected to deliver -5.4% real returns and U.S. Small Caps at -3.6%, reaffirming GMO’s long-held caution toward overextended U.S. valuations. However, within the U.S., Deep Value pockets are expected to outperform meaningfully with 5.6% real returns.

Fixed Income: modest gains, led by inflation protection and EM debt

While returns in fixed income remain muted, GMO sees modest real yields in select areas:

| Asset Class | 7-Year Real Return Forecast (Normal Rate) |

|---|---|

| U.S. Inflation-Linked Bonds (TIPS) | 2.0% |

| Emerging Debt | 2.1% |

| U.S. Bonds | 1.6% |

| U.S. Cash | 0.7% |

GMO’s view suggests that TIPS and Emerging Debt offer slight advantages over traditional U.S. bonds, particularly as inflation volatility remains a risk. Cash, while positive in real terms under the normal rate scenario, still provides the lowest return profile among investable asset classes.

Implications for European asset allocators

The forward-looking picture laid out by GMO implies several actionable themes for professional investors:

- Global Value Rotation: With U.S. large-cap growth stocks looking increasingly stretched, GMO strongly advocates for a rotation toward value-oriented and non-U.S. equities—especially small-cap and deep value opportunities in Japan, Europe, and EM.

- Emerging Markets Repricing: After years of underperformance, emerging market equities and debt are positioned for a relative comeback, offering both valuation support and positive real returns in a diversified portfolio.

- Selective Fixed Income: In a normalized rate environment, inflation-linked bonds and EM sovereigns could serve as resilient fixed income components, especially for investors concerned with purchasing power preservation.

- Avoiding Overvalued Segments: The continued negative outlook for U.S. Large and Small Caps underlines the risk of crowding into the most expensive segments of global equity markets.

Closing thoughts: discipline in the age of dispersion

GMO’s 7-Year Forecast continues to advocate for valuation discipline, global diversification, and contrarian thinking—principles that resonate in today's uncertain environment. While headline U.S. markets may dominate media and flows, the best forward-looking opportunities, according to GMO, lie elsewhere: value over growth, international over U.S., and small over large.

For professional European investors navigating long-term portfolio construction, the message is clear: now is not the time for complacency. Instead, consider rebalancing toward those unloved corners of the market that GMO believes are poised to deliver the most attractive risk-adjusted returns through the end of this decade.

This article is for informational purposes only and does not constitute financial advice.