Hong Kong China Equities: Finding Value Amid the Reopening

In 2023, many of the headwinds that have been dragging the Chinese equity market down over the last two years may turn into tailwinds. Indeed, Chinese equities have faced a number of challenges, from the risk-focused regulatory tightening on certain sectors, to COVID lockdowns hindering domestic activities, to weakness across the property markets. But with the reopening of the economy at the end of 2022, the bear market has ended and the outlook for Chinese equities looks positive. At the same time, China’s government has committed to focusing on growth, suggesting that a number of supportive policies are likely to follow.

Economic Reopening to Support Consumption

The zero-COVID policy was a key factor in stalling China’s economic engine in 2022. However, toward the end of the year, the government began to rapidly unwind restrictions, resulting in a rebound in China’s domestic consumption. Going forward, this recovery is likely to continue, for a number of reasons. For one, Chinese household savings in 2022 grew by $123.7 billion, and a sizable portion of this is likely to turn into pent-up demand in the year ahead. In addition, the Chinese government prioritized “increasing consumer demand” at the 2022 Central Economic Work Conference—suggesting the potential for further stimulus aimed at boosting consumer sentiment, from tax cuts and purchasing incentives, to the issuance of consumption vouchers.

Regulatory Tailwinds for Property and Tech

Internet companies and property developers are also likely to be supported by a potential easing of regulations going forward. This is another facet of the government’s concerted efforts to bolster domestic activities and consumer sentiment. In particular, property developers’ balance sheets are receiving much-needed lifelines in the form of credit provisions from Chinese banks. Nearly a dozen supportive policies have already been introduced since late 2022 to improve balance sheet quality and housing affordability. Homebuyer sentiment will likely improve as a result, along with valuations and fundamentals across the sector.

Similarly, the policy stance toward internet companies turned supportive in the second quarter of 2022 when approval of new gaming licenses resumed. Looking ahead, as consumer sentiment gradually improves, platform companies could emerge with a higher wallet share of offline spending as well—largely because consumers have become more reliant on platform apps for their day-to-day activities.

Areas of Long-Term Opportunity

The key strategic directions envisioned for China includes objectives such as the dual circulation model of economic development, sustainable development, innovation and modernization, and improved social wellness. These initiatives will likely shape long-term opportunities in the companies and sectors that have exposure to the themes.

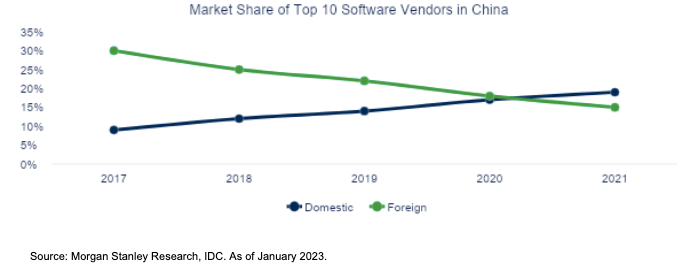

Domestic Brands Dominate

A key priority of the dual circulation model initiative is internal circulation, which aims to cultivate a strong domestic economy with locally produced goods and services comprising a significant portion of domestic consumption. As a result of these efforts, local brands have become more competitive through improved quality of products and services, and we believe an increasing number of these brands are likely to outperform in areas such as sportswear, software, automobiles, and consumer goods.

Figure X: domestic brands dominate china’s software industry

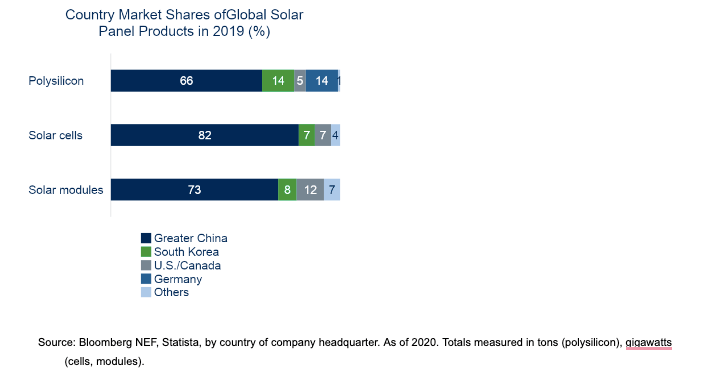

Chinese Companies Increase Value-add in Global Supply Chains

The external circulation aspect of the dual circulation initiative aims to enhance China’s competitiveness within the global supply chain, and improve Chinese companies’ entry into higher value-add segments. This requires leveraging China’s supply chain advantage, and its position as the world’s largest market, to foster innovation and broaden. The external circulation aspect of the dual circulation initiative aims to enhance China’s competitiveness within the global supply chain, and improve Chinese companies’ entry into higher value-add segments. This requires leveraging China’s supply chain advantage, and its position as the world’s largest market, to foster innovation and broaden product distribution globally. In particular, China produces some of the largest cohorts of STEM graduates every year, enabling Chinese companies to dominate a number of forward-looking industries. For example, over two-thirds of the production within the global solar panels supply chain are manufactured in China.

Figure X: chinese companies lead forward-looking industries

Increasing Focus on Sustainability and High-quality Growth

As China’s focus is shifting from high-speed growth to high-quality growth, efficiency improvement and risk mitigation are becoming key priorities for optimization. As a result, there is a growing focus on sustainable development, including expanding renewable energy infrastructure and reducing waste. While this will help mitigate climate-related physical and transitional risks, it will also shape opportunities in companies that are drivers of the transition to a low carbon world.

Key Takeaway

Looking ahead, given ongoing uncertainties around company earnings and global economic growth, volatility is likely to remain elevated. But as the short and long-term factors shaping the Chinese economy continue to unfold—from an economic reopening, to a recovery in fundamentals, to policy support—we believe the outlook for Chinese equities is positive. In our view, the market consolidation is presenting attractive entry points for investors to gain exposure to the world’s second largest economy and equity market.

For Professional Investors / Institutional only. This document should not be distributed to or relied on by Retail / Individual Investors. Any forecasts in this material are based upon Barings opinion of the market at the date of preparation and are subject to change without notice, dependent upon many factors. Any prediction, projection or forecast is not necessarily indicative of the future or likely performance. Investment involves risk. The value of any investments and any income generated may go down as well as up and is not guaranteed by Barings or any other person. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

Barings is the brand name for the worldwide asset management or associated businesses of Barings. This document is issued by the following entity: Baring International Fund Managers (Ireland) Limited), which is authorized as an Alternative Investment Fund Manager in several European Union jurisdictions under the Alternative Investment Fund Managers Directive (AIFMD) passport regime and, since April 28, 2006, as a UCITS management company with the Central Bank of Ireland.