How could Kevin Warsh lead the Federal Reserve?

2 JUN, 2026

By Álvaro Peró from Capital Group

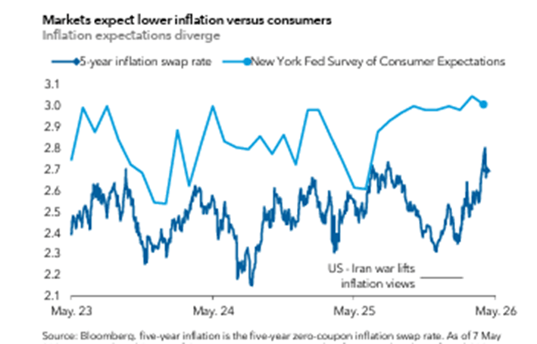

Kevin Warsh assumes leadership of the Federal Reserve at a complex moment. Inflation has risen amid the conflict between the United States and Iran, labor markets are uneven, and signs of growing internal dissent within the Fed are emerging. In this environment, the path toward lower interest rates is less clear, increasing the importance of both monetary policy decisions and market expectations.

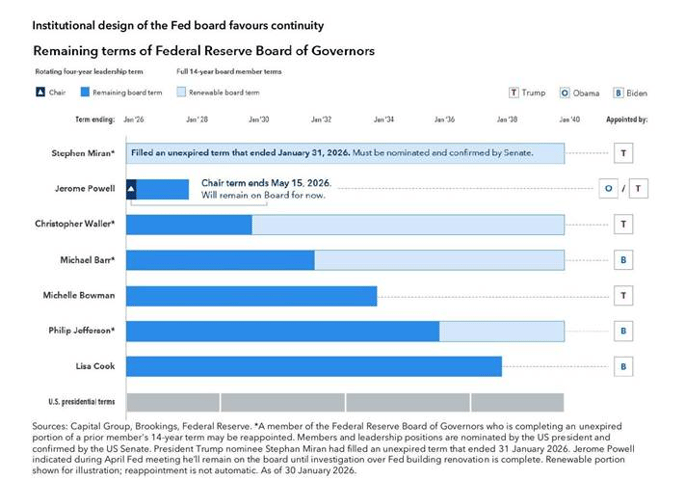

It is important to note that Jerome Powell has indicated that he will remain on the Fed's Board of Governors until the investigation into the central bank's building renovation is completed. Members of our fixed income team continue to expect institutional continuity at the Fed, which should limit political influence over the central bank.

The collective judgment of the Federal Open Market Committee (FOMC) and the Board of Governors remains central to policymaking. Governors serve staggered 14-year terms spanning multiple presidential administrations, providing protection against short-term political pressures and limiting any single president's ability to unilaterally redirect monetary policy.

Although leadership changes can influence communication and risk tolerance at the margins, they do not replace the existing monetary policy framework. Markets should focus on the underlying fundamentals of the U.S. economy, rather than on who occupies the Fed chairmanship, as the primary driver of monetary policy.

A Fed Chair Focused on Cutting Rates Takes Charge

A rate cut before year-end remains possible, although it is subject to more conditions than before. Rising oil and gas prices have dominated headlines, but renewed supply-chain pressures—including indirect effects from chemical and industrial inputs—could add moderate upward pressure to core Personal Consumption Expenditures (PCE) inflation in the coming months. These cost pressures are also likely to weigh on consumption, potentially slowing growth.

As a result, the Fed will have to balance the risk of slower growth against elevated inflation over the next six to twelve months. Market-implied probabilities of rate hikes have increased since the beginning of the year, but they appear exaggerated relative to underlying fundamentals.

A sustained cycle of rate increases would likely require a more persistent inflationary impulse, possibly driven by a combination of strong demand, tighter labor markets, and significant wage growth that challenges the current view of contained underlying inflation.

Even in that scenario, our rates team considers the probability to be a tail risk—closer to 10% than to the higher levels implied by options markets—which reinforces the case for maintaining some duration exposure.

At the same time, progress on inflation remains uneven. Core PCE inflation was already above 3% before the U.S.–Iran conflict, and underlying inflationary pressures remain a key focus for the FOMC. If the assumption that supply shocks will dissipate without affecting wages or broader inflation proves incorrect, the Fed's ability to remain patient could be tested. Until then, policy is likely to remain data-dependent, with a bias toward easing once sufficient confidence in disinflation has been achieved.

Beyond Rate Cuts

Warsh may face challenges in containing long-term interest rates because of his views on the Fed's balance sheet. While policy rates influence the short end of the yield curve, long-term yields are determined by inflation expectations, fiscal dynamics, global demand for U.S. Treasury securities, and term premiums. Tools such as quantitative easing and Operation Twist¹ put downward pressure on those premiums, and Warsh has been critical of the Fed's balance-sheet size.

Overall, compared with previous cycles, the Fed is operating with more limited policy tools. Interest rates remain only modestly restrictive while inflation continues to run above target, limiting the Fed's ability to ease policy preemptively. Furthermore, bank reserves are near what has historically been considered the Lowest Comfortable Level of Reserves (LCLoR). Therefore, if Warsh wished to reduce the balance sheet while cutting rates, banks' demand for reserves would also need to decline.

Banking deregulation could contribute to that process to a limited extent, although it would likely be gradual and approached cautiously by the Fed. The institution still has tools such as its Standing Repo Facility and Treasury bill purchases for reserve management, providing a safety net as it attempts to reduce reserve levels over the long term. The U.S. Treasury is also considering investing its cash balances in the repo market to mitigate volatility in funding markets.

The Elephant in the Room: U.S. Debt

U.S. federal debt now exceeds the size of the economy, and the annual deficit is running at levels traditionally associated with extraordinary periods such as the pandemic or major military conflicts. The scale of the debt and persistent deficits raise important questions about how the Fed will manage this environment.

High debt levels can constrain fiscal flexibility and increase market sensitivity to interest-rate movements, placing greater pressure on monetary policy as a stabilization tool during periods of stress.

For now, the size of the debt does not appear to be a major concern for markets, possibly because investors view it as manageable or as a longer-term issue compared with other immediate macroeconomic factors. Strong demand for Treasury securities, the central role of the U.S. dollar in global finance, and sustained growth driven by investment in artificial intelligence support confidence in the government's ability to meet its obligations.

However, markets could shift their focus if financing that debt becomes more difficult. If borrowing costs remain elevated, deficits do not decline, or confidence in the fight against inflation weakens, pressure could gradually emerge through higher yields and increased volatility, tightening financial conditions.

These factors, together with the possibility of a rapid depreciation of the dollar should its reserve-currency status come into question, could limit policymakers' room for maneuver.

Conclusion

Ultimately, Warsh takes office in an environment characterized by greater inflation uncertainty, an uneven labor market, geopolitical pressures, and high debt levels—factors that may constrain the flexibility of monetary policy. Although he is expected to differ from Powell in his communication style, the policy trajectory is likely to remain data-dependent and institutionally driven. For investors, the bias toward a more accommodative policy stance remains in place for now, although the path forward has become more conditional.

¹ Operation Twist refers to a Federal Reserve strategy of selling short-term Treasury securities and buying long-term Treasury securities to lower long-term interest rates without expanding the Fed's balance sheet.