How have the 2024 elections affected emerging markets?

17 JUL, 2024

By Schroders

Author: Andre Rymer, Senior Strategist, Strategic Research at Schroders

While in developed markets the election cycle is just beginning, in emerging markets the elections scheduled for 2024 have already concluded.

Late May and early June saw a spike in market volatility in several emerging markets (EMs) in the wake of key national elections. The most notable example is Mexico, which experienced a sharp sell-off in equities and currencies. There was also a rally in bond yields following the results of the presidential and legislative elections in early June.

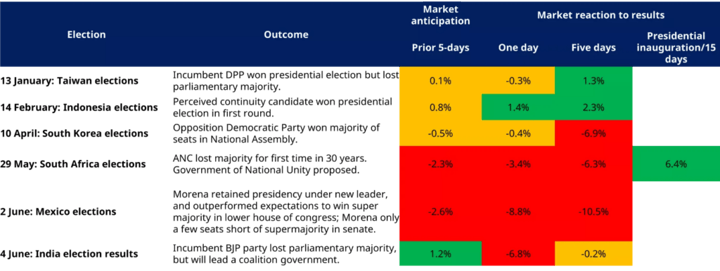

Elections were held in markets accounting for more than 50% of the MSCI Emerging Markets index, with mixed results, as summarised in the table below. We assess the results, market reaction and longer-term policy implications for these markets.

2024 Full MSCI EM elections - mixed results

Mexico

On June the 2nd, presidential and general elections were held in Mexico, which resulted in Claudia Sheinbaum as the winner. Sheinbaum is the successor backed by President Andrés Manuel López Obrador (AMLO), who served a term limit.

Sheinbaum exceeded expectations and was elected president with the highest percentage of votes since 1982 and will take over from AMLO on October 1st of this year. However, the results of the congressional elections were more surprising, as Sheinbaum's Morena party won a supermajority in the lower house of Congress. She was only a handful of seats short of a majority in the Senate. This opens up the possibility that Morena will be able to pass constitutional reforms. The fact that there is a one-month period during which the new Congress will overlap with the end of AMLO's term has increased market concerns. AMLO pushed for constitutional reform during his term, including a proposal (later rejected) to prioritise the state electricity company over private companies in electricity production. The congressional election results and associated risk caused the MSCI Mexico index in US dollar terms to fall 9% on the day of the results. This included a 4% drop of the peso against the US dollar. Five days after the elections, the market was down almost 11% in dollar terms.

South Africa

South Africa held a general election on May the 29th. Opinion polls had indicated that the African National Congress (ANC) party, which has ruled South Africa since 1994, would see its share of the vote decline, but would gain enough support to stay in power. In fact, the ANC's vote share fell from 57% in 2019 to 40%, much worse than expected. The main opposition, the Democratic Alliance (DA), reached 22% of the vote, slightly above 2019. The vote share shifted mainly to the MK Party (15%), founded only six months ago and led by former ANC leader and president Jacob Zuma. The Economic Freedom Fighters (EFF) came fourth with 10%. These results reflect a split in the ANC vote: these two parties are led by former ANC members and combining their share of the vote with that of the ANC would reach 65%, close to the ANC's historical share of the vote.

Uncertainty increased after the election result, when the ANC lost its majority. The equity market fell by more than 3% in US dollar terms the day after the election, as the results became known, and the rand (South African currency) fell by 2%. Five days after the election, the market was down 6%. The undecided results ushered in a period of high uncertainty, although financial markets were somewhat resilient to the circumstances and did not reflect the most negative scenarios. According to the Constitution, the ANC had two weeks after the election to agree on a coalition or confidence and supply agreement with other parties. Several permutations were possible, but with very different implications for the political trajectory.

The equity market and the rand have rallied following the announcement of the Government of National Unity and the inauguration of President Ramaphosa. The MSCI South Africa is up 2% in US dollar terms so far this year (as of 27 June 2024). The rand has also rallied, with the 10-year government bond yield down to 10.2%.

President Ramaphosa proposed a ‘National Unity Government’, inviting all parties to come to the table. The EFF rejected the plan, given the inclusion of the DA, and MK has indicated that it would not work with the ANC as long as it is led by Ramaphosa. Thus, the ANC, the DA and the smaller parties form the GNU. It looks like a shrewd move on the part of the president, as the optics show MK and the EFF rejecting the GNU, as opposed to the ANC opting to go into coalition with the DA. Ramaphosa has since been re-elected president by parliament and sworn into office.

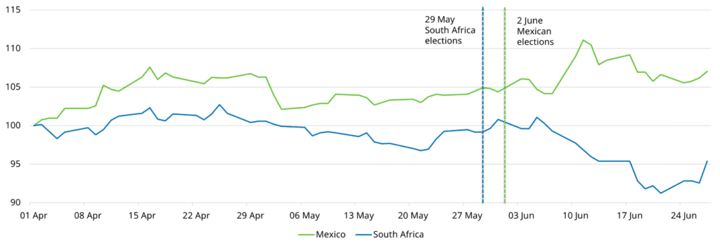

Mexico and South Africa 10-year government bond yields volatile since elections

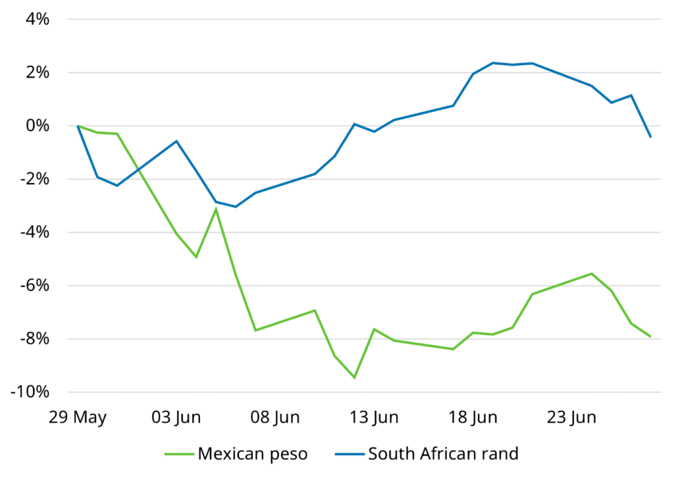

The Mexican peso has been notably weak, while the rand has held up better

India

India's general election was held between 19 April and June 1st, and the official results were announced on June 4th. Prime Minister Modi's Bharatiya Janata Party (BJP) was expected to be re-elected with a large majority.

Indeed, early exit polls, released on June 3rd, suggested that this scenario had played out as expected. However, it did not. The official election results showed that while the BJP-led National Democratic Alliance retained its parliamentary majority, the BJP had lost its single-party majority. Prime Minister Modi will remain in power, but with a weaker, albeit solid, mandate.

Market sentiment around the election results was volatile. Exit poll data triggered a 4% rise in US dollar terms. However, the release of the official results the following day caused the market to fall by almost 7%. Five days after the election, the market had effectively recovered and had risen in dollar terms if one looks back, before the exit poll rally.

In the longer term, the structural drivers of economic growth remain in place, but the election results imply a closer balance in parliament. This is likely to require greater consensus, which could be seen as a positive outcome. However, there is a greater risk of populism, if the BJP seeks greater rural support, and possible delays in implementing policies and reforms that require legislative changes.

So far this year, the MSCI India index has returned 17% (as of June the 27th), outperforming emerging markets in general. This performance has been driven by strong performances in the consumer discretionary and industrial sectors, in particular.

South Korea

On April 10th, general elections were held in South Korea to elect members of the 300-seat National Assembly for a new four-year term. These elections, which are held midway through the presidential term, are often seen as an indicator of public approval.

Pre-election opinion polls pointed to a close contest between President Yoon's People's Power Party (PPP) and the main opposition Democratic Party (DP). In the end, the polls proved to be inaccurate, with the opposition winning 175 seats and gaining a majority. The initial market reaction was muted, but five days after the election, equities were down almost 7 per cent in dollar terms.

Together with allied parties, the PD has an absolute majority, which should allow it to pass laws. However, it lacks a sufficient majority to remove the president from office. The results may put the brakes on some of President Yoon's most ambitious policies. The Corporate Value-Up programme, launched earlier this year, aims to encourage companies to take action in cases of low valuation against their global peers. This includes improving corporate governance standards. Regulatory changes in this regard are still awaited, but it seems unlikely that Congress will pass tax incentives.

So far this year, the MSCI Korea index is broadly flat in US dollar terms, relatively underperforming emerging markets in general, largely explained by the weaker won. Industrials and materials sectors remain the main drags on the market this year.

Indonesia

Presidential and general elections were held in Indonesia on February the 14th. Prabowo Subianto, who was Minister of Defence, won in the first round, according to initial quick counts on February 15th. Official results later showed that Subianto had won 59 per cent of the vote, eliminating the need for a run-off. Subianto will take over as president in October from Joko Widodo, who had completed a maximum of two five-year terms. The result was largely in line with opinion polls.

The initial result was welcomed by equity markets, which rose by more than 1% in US dollar terms on the quick count, and by 2% in the five days following the results.

However, so far this year, the MSCI Indonesia index is down 12% (as of 27 June 2024). The election results seemed to remove uncertainty in the long-term political outlook and pointed to a continuation of the reforms initiated under the previous president. However, the external outlook has deteriorated against the backdrop of a stronger US dollar.

Indonesia has twin current and fiscal deficits and, despite benign inflation, the central bank was forced to raise its policy rate in April to support the currency. Moreover, Prabowo has yet to announce a cabinet and there remains some uncertainty about the extent to which policy might deviate from Widodo's.

Taiwan

Taiwan held presidential and parliamentary elections on January 13th. The Democratic Progressive Party (DPP) retained the presidency under the new leadership of William Lai Ching-te, but lost its majority in parliament.

Unlike the DPP's last two presidential election victories under Tsai Ing-wen (who had completed a maximum of two terms), its vote share fell to 40 per cent from 57 per cent and 56 per cent in 2020/2016 respectively. The main opposition party, the Kuomintang (KMT), also saw its vote share fall, with the Taiwan People's Party (TPP) being the main beneficiary. In Taiwan's legislative elections to the Yuan parliament, the PDP lost its majority, with the KMT winning 14 seats, with a total of 52 seats, to the PDP's 51.

A key risk heading into the election was the possible future policy and impact on cross-strait relations with China. This outcome, in line with expectations, is expected to somewhat limit the policy agenda during this presidential term. Political stability, especially regarding foreign policy, and the absence of a significant deterioration in relations with China remain crucial for the long-term market outlook.

Markets reacted accordingly, with MSCI Taiwan almost flat in dollar terms on the day of the results. Five days after the election, the market had advanced more than 2%. Year-to-date (to 27 June), Taiwanese equities have returned 28% in US dollar terms, driven mainly by the strong performance of the Information Technology (IT) sector, which accounts for 77% of the index.

Election uncertainty behind us?

Emerging market elections scheduled for 2024 are over. Results in the largest markets by market capitalisation, India and Taiwan, are neutral/positive for investors. Otherwise, some uncertainty remains, especially in Mexico, but also in South Africa, regarding the ability of the National Unity Government to enact reforms.

Emerging markets have just handed over the election baton to developed markets, with important elections in the second half of the year in the UK (general), France (legislative) and the US presidential elections in November. The latter, in particular, will be closely watched, given their implications for US foreign and trade policy.