How was the Q2 reporting season?

21 AUG, 2024

Author: Chiara Robba, Head of Equity LDI at Generali AM, part of Generali Investments Ecosystem.

This earning season has been quite volatile both in Europe and in the USA. There are two main reasons: on one side still the high market concentration in few names/themes have caused pronounced negative reactions when the Company reporting were missing numbers. The second factor of volatility during this reporting season is related to softening macro data on both sides of the Atlantic, with an increased probability of recession in the US over the next 12 months.

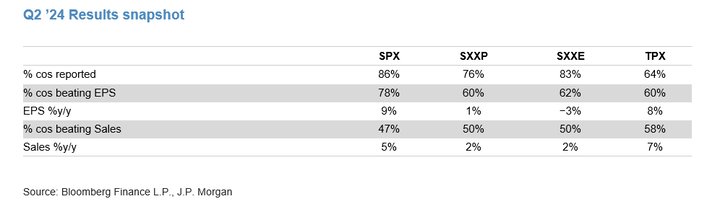

Looking more into the details of the 2Q24 reporting, overall more than 75% of the companies in US and in Europe have already released numbers, with higher beat to consensus EPS in US rather than in Europe.

Moreover, the 2Q results have shown +5% sales growth in US compared to +2% in Europe and +9% EPS growth in US with only 1% in Europe, therefore showing more margin resilience in US so far.

In particular, European domestic exposed companies reported better than the international ones, especially if we look at the European Companies more exposed to China, which is still suffering from macro subdued growth. In this context, Defensive sectors like Healthcare and Utilities, have reported better than the Cyclical ones with Consumer Discretionary and Industrials that have seen negative EPS revisions. It is a matter of fact that since the beginning of July, Luxury Goods, Semiconductors and Automobile are the industries that saw the biggest negative revisions to earnings. Their exposure to China has triggered some concerns also on the possible effects of increased global tariffs in the case of a Trump re-election in November.

Real estate, Healthcare and Utilities saw the biggest positive revisions in the last month, both for the FY2024 as well as 2025, benefitting also from an increased probability of rate cuts from the Central Banks. These are the sectors that have a negative correlation to rates, so they should benefit the most from a revised expectation of Fed and BCE rate cuts post the weakening of macro data points.

On the Cyclical side, Banks have continued to see an overall positive reporting with continue upgrades to EPS. Nevertheless, concerns on the macro-outlook have weighted on the share price reaction as the sector was well owned and some investors decided to took profit post the strong performance since the beginning of the year.

One of the areas of concern during this reporting continues to be the status of the consumer, as there are first signs that the pricing elasticity in some sectors is fading. We saw during the reporting some weakness both in the high-end consumption, with warnings from Luxury Companies (Burberry, Kering, Hugo Boss, but also LVMH being not immune), and also in the low-income consumption (Ryanair, Nestle and in some extent also Unilever).

In the context of an inflation that has been stickier that originally expected in all the geographies except China, consumers have been able to absorb prices increases thanks also to the exceptionally high level of savings accumulated during the Pandemic. It seems that now this is coming to an end.

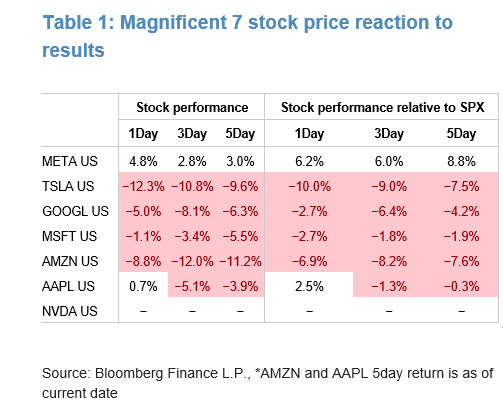

Where we have seen the highest volatility during the reporting so far is in the Tech sector, as raising doubts about AI returns on huge capex expenditures have hit Semiconductor’s names both in US and in Europe.

Nevertheless, investors must wait until the end of August for Nvidia’s reporting before having the final say on the Tech’s outlook.

Overall, the messages coming from the Companies post the reporting is prudent as visibility on the 2H of the year looks low at the moment: consumption is slowing, geopolitical tensions are increasing and liquidity during the summertime is usually low.

The recent market pull back, triggered by unwinding carry trade positioning on the Yen post the BoJ rate increase and higher probability of recession in the US, it is not considered a strong entry point to the market yet.