What impact will the rates environment have in the European banking sector?

28 AUG, 2024

After the minutes of the last Fed meeting, and particularly after Jerome Powell's speech in Jackson Hole, it is almost a given that the Federal Reserve will begin the cycle of rate cuts at its next meeting in September. After an intense period in which the price of money was high, which is a very positive situation for the banking business, they are facing a context of falling rates. How will the European banking sector react to the cuts?

Author: Thibault Nardin, Global Industry Analyst, Wellington Management

Of course, interest rates remain a key part of the debate. European financials have typically been a strong sector for alpha generation. There are 44 countries in Europe and the 44 banking sectors all work differently. While this is not great for economic efficiency in Europe, it creates compelling potential for uncovering mispricing and divergence in fundamentals. As rates go down, I expect further divergence in terms of the path of return on equity and dividends for banks from different countries, which should translate into more share price dispersion across the sector.

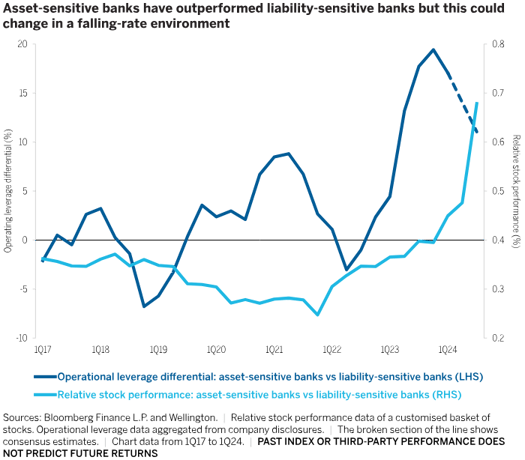

Asset-sensitive banks (in general, Iberian, Italian, Greek and Irish banks) — which are more vulnerable to falling rates given the shorter duration of their assets versus their liabilities — have benefited from the “higher-for-longer” scenario year to date (Figure 1) and have the highest free-cash-flow generation over the short term. However, they are at peak profitability and have re-rated the most in recent months. In contrast, liability-sensitive banks (in general, Benelux, French, German and UK banks) have weaker earnings momentum, and trough or mid-cycle levels of free-cash-flow generation but, in my view, can expect higher earnings growth and resilient profitability in a falling-rate environment. For these reasons, looking out over the next three to five years, I think the risk/reward profile of liability-sensitive banks looks better than that for their asset-sensitive peers.

Figure 1

European banking sector is in an environment of ongoing change and growing dispersion. The sector remains a fertile ground for active investors with the research expertise to separate the likely winners from the losers.