Intelligence is the new steel: a new perspective on the DeepSeek moment

31 MAR, 2026

Carlo Gioja, Senior Portfolio Manager at Plenisfer Investments, part of Generali Investments.

The race for artificial intelligence is unfolding in very different ways.

On one side of the Pacific, U.S. technology companies are investing vast amounts of capital in advanced chips and model development in pursuit of Artificial General Intelligence, or “God in a box.” This is driving up equipment prices and stretching corporate budgets.

On the other side of the ocean, China is working to make AI inference widely available at the lowest possible cost and to accelerate its large-scale adoption.

These very different approaches are driven by both cultural elements and structural differences.

Historically, companies in China have never developed the habit of paying for software. The SaaS (Software as a Service) sector in China has long struggled with monetization and, even today, its revenues are roughly an order of magnitude lower than those in the United States. As a result, direct monetization of large language model (LLM) products through retail and corporate subscriptions is much more difficult in China, forcing model developers to pursue the open-source route.

More importantly, structural differences between the two economies also shape strategic decisions. While the United States has the most advanced AI chips, China has a much larger installed energy capacity. While China struggles to manufacture advanced chips—having been cut off from leading global semiconductor equipment suppliers—the United States faces a significant energy supply bottleneck, making AI deployment more difficult and expensive.

To some extent, the AI race comes down to whether the United States will solve its energy problems before China figures out how to manufacture the chips.

In January 2025, China’s DeepSeek appeared out of nowhere with the launch of R1, a model that roughly matched the performance of OpenAI’s then-leading model, o1, but at a fraction of the cost. The release of R1 demonstrated that low-cost, open-weight models can come very close to the cutting edge and be good enough for most commercial applications. Suddenly, the “winner-takes-all” dreams of leading U.S. AI labs seemed far less certain.

A year later, China still lacks advanced U.S. chips, and Chinese models remain heavily censored, refusing to respond to any mention of Tiananmen Square—a constant source of amusement for Western skeptics. DeepSeek and other Chinese developers have reportedly been caught “cheating” by using leading U.S. models to train their own.

However, innovation is born from scarcity.

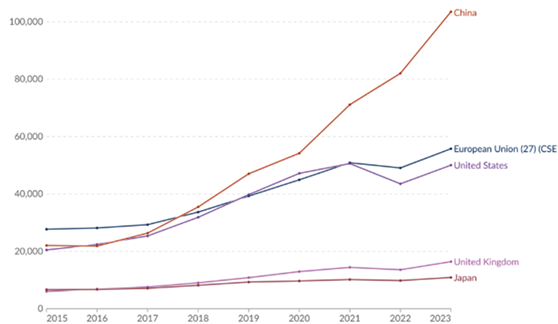

The lesson of the “DeepSeek effect” was not that ambitious startups were cutting corners, but that algorithmic innovation can compensate for hardware limitations. What if the DeepSeek moment is not just a technical breakthrough, but a symptom of an ecosystem reaching critical mass? The growth in AI scientific output highlights the rapid expansion of China’s research and innovation ecosystem in recent years.

Annual academic publications on AI by region

China’s 15th Five-Year Plan (2026–2030) focuses on “embedded AI” as a strategic national objective: the rapid integration of AI into as many products and services as possible, as quickly as possible. In line with this goal, AI models are treated as national infrastructure—a foundational commodity for the entire economy, much like electricity or steel.

In 2025, the country added approximately half a terawatt (TW) of capacity, about 50% of the entire U.S. power grid. Under the “East Data, West Computing” initiative, workloads are being shifted from the developed eastern coast (Shanghai, Shenzhen) to energy-rich western regions via high-speed data and power lines. To address monetization and adoption challenges, local governments have increased subsidies for token usage and cloud storage. These subsidies are explicitly intended to “buy time” for the domestic chip industry to catch up with Nvidia’s leading chips in terms of energy efficiency. The national government is also sending a clear signal that domestic companies should purchase domestic hardware.

Meanwhile, Chinese labs have become exceptionally fast followers, finding innovative algorithmic solutions that reduce computing requirements while achieving comparable performance. Within weeks of Anthropic’s release of Opus 4.6—which triggered market panic about the “old” software industry—Zhipu AI unveiled a model with comparable high-end performance, aiming to significantly reduce inference costs. Shortly after Google introduced Genie 3 for world simulation, ByteDance launched Seedance 2, capable of turning a simple storyboard into a full cinematic trailer with sound and dialogue. As of this writing, DeepSeek is expected to release its V4 model, which will likely further reduce inference costs.

The promise of open source and rapid large-scale adoption (“embedded AI”) is that greater adoption leads to better hardware economics, better data, more edge cases, and more algorithmic innovation—creating a virtuous cycle that leads to better models.

Thus, rapidly scaling adoption is not just about using existing capacity—it is also a way to accelerate model development. If the next generation of agents can learn to manage a manufacturing line, operate autonomous robots, or conduct pharmaceutical trials, the resulting productivity gains could offset the initial investment, making Chinese products and services far more globally competitive.

A generation ago, the global economy became dependent on cheap Chinese manufacturing. What if it became dependent on Chinese computing?

It may be tempting to assume that current geopolitics will make China’s approach unsustainable, limiting the global expansion of these technologies. While the real estate crisis continues to weigh heavily on economic growth, and the challenges facing the country’s AI strategy are real—the decision-making process is far from perfect, and the lack of transparency around state support for training and inference makes straightforward economic analysis extremely difficult.

However, as investors, we also observe that even a scenario of partial success is far from being priced in. According to Bloomberg data, the MSCI China is currently trading at 12 times expected 2026 earnings, compared to the S&P 500 at 22 times, with roughly comparable mid-double-digit expected growth. If Beijing’s AI bet succeeds, Chinese productivity could accelerate significantly over the next decade.

The beneficiaries will not necessarily be AI infrastructure providers or model creators. The government’s goal is for the benefits to flow into the broader economy and spread across many sectors, such as manufacturing and healthcare. In the 2000s, the state subsidized the production of critical resources like steel, enabling domestic firms to dominate industries such as shipbuilding, logistics, and modern manufacturing. Now, the real value of Chinese AI may also be captured further down the value chain by companies that use low-cost inputs to strengthen their competitive advantages even further.