INVESCO: “Hic et Hung” when the market paraphrases “here and now”

26 MAY, 2026

By Daniel Zanin from Invesco

In the last two years, more than dividends and multiples, what has mattered is the desire for future earnings.

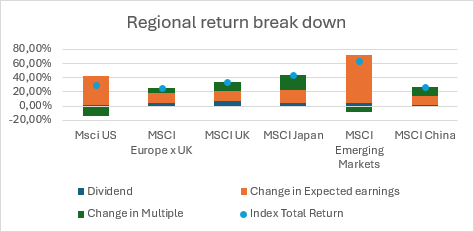

When you put global index performance under the microscope and break it down using a DuPont-like logic, a much less “rational” dynamic emerges than is usually described: the dominant component of returns has not been dividends, nor multiple expansion, but changes in expectations about future earnings.

In other words, the market did not move simply by evaluating the “Hic et Nunc” – the here and now – but rather by thinking in terms of “Hic et ‘Hung’” – the here and suspended. Investors have continuously updated what could exist, not what is. This is precisely the space of desire. Lacan would say that we never truly desire the object itself, but rather what that object promises to fill: a lack, a distance, a tension toward something that is not yet there. Applied to markets, this means that we do not just buy earnings, margins, or cash flow; we buy stories about earnings, narratives about margins, growth expectations.

The chart makes it clear: while dividends and multiples play secondary and more unstable roles, it is earnings revisions that explain the bulk of returns across different regions. This is equivalent to saying that the real driver has not been the object itself – the current level of earnings – but the movement of desire around that object, meaning the way the market has progressively redefined what it expected from the future.

This also helps reinterpret a seemingly well-known dynamic: earnings revisions attract flows, and flows reinforce revisions. This is not just an informational mechanism; it is a desiring mechanism. Because desire, in the Lacanian reading, is always mediated by others: we desire what is recognized, what is shared, what circulates as a “credible promise.” Thus, over the past two years, the market has progressively built and reinforced certain narratives – such as earnings resilience, margin stability, productivity, innovation – and it has done so through the most direct channel possible: by raising earnings expectations. That is where capital has concentrated, because that is where desire has concentrated.

Like any desire, this one does not end once the objective is reached. When expectations improve, the cycle does not close – it opens the next one. A single upward revision is no longer enough; a higher, broader, more convincing revision is required. Growth is no longer enough; the quality of growth is required. The market does not seek a final equilibrium, but a continuous redefinition of what is missing. And that is why even periods of multiple compression can coexist with rising markets: because the driver is not necessarily the price paid for earnings, but the expected trajectory of earnings themselves. In a sense, we could say that over the past two years the market has priced in more the void than the fullness: more the distance between today and tomorrow than the current level of fundamentals. And this is not an anomaly; it is a structural feature.

The point, therefore, is not only to understand whether earnings will grow or not, but to understand when they will stop being the dominant object of desire. Because as long as the market continues to revise them upward, it will continue to support prices. But the moment the narrative changes, the moment that void is perceived as less interesting or is replaced by another, capital flows will follow. Ultimately, it is not earnings that drive returns, but the desire for earnings that have not yet materialized that drives investor sentiment.