Investing in emerging markets for income?

5 MAR, 2024

By Jose Luis Palmer from RankiaPro Europe

Autor: Raheel Altaf, EM Fund Manager

Investors tend to view emerging market equities as a growth asset. Historically, of course, emerging economies have usually grown faster than developed ones. But this superior growth hasn’t always translated into better share price performance. There are many reasons for this, but – put simply – the economy isn’t the stock market. While the number of companies one can invest in has risen quite dramatically in the last decade as a result of new companies coming to the market, there are also a large number of well-established businesses. Increasingly, these have appealing characteristics for investors. For example, we would argue that emerging equities should also be considered for their income distribution. Policy developments in a number of economies suggest dividend payouts could become more attractive. We are finding many businesses with outstanding shareholder yields on offer.

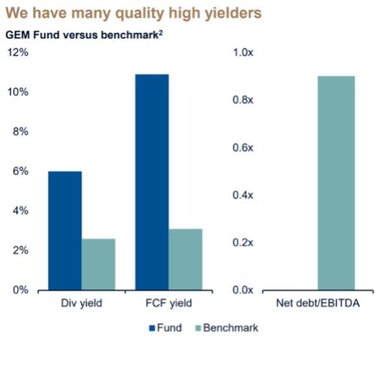

The dividend yield on the MSCI GEM index was 2.9% at the end of 2023. This headline yield masked a wealth of opportunities - our fund’s yield was 5.5% at the same period[1]. As the chart below shows, not only are we invested in higher yielding companies than the market, but these businesses also have attractive cash generation to support dividend payments and have relatively less debt on their balance sheets.

What is behind these attractive dividend yields?

Given the diverse universe of emerging market stocks, there are a broad range of reasons for high dividend payouts. Healthy balance sheets, improving cashflows and shareholder policy reform make the dividend story in emerging markets a compelling one.

Conservative management – Asian companies

Tough experience has taught Asian managements to be conservative. We see little evidence of reckless expansion or M&A activity. Instead, we find lots of companies with strong balance sheets using their healthy cashflows to pay out dividends or for share buy backs – a sensible strategy when share prices are depressed.

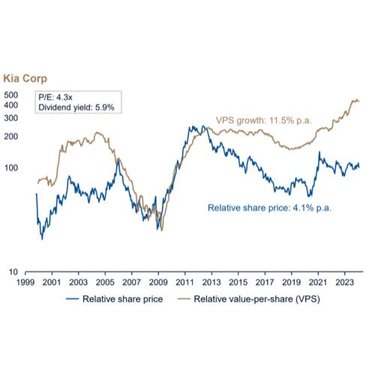

For example, we have a big position in Kia Corporation, Korea’s second largest car manufacturer. Kia delivers a nearly 6% yield and has also been buying back shares. Over five years, Kia aims to purchase up to KRW 0.5 trillion (over $373m USD) worth of shares each year and cancel at least 50% of the repurchased shares.

The framework we use to identify Kia as an attractive opportunity, is one that we can apply to any company in our investible universe of almost 3,000 stocks. We believe that share prices ultimately follow fundamentals. We track ‘value-per-share’ (VPS), a combined measure of earnings, cashflow, operating profits, dividends and asset value per share. When this is improving, we should expect the share price to keep pace. At times it doesn’t, this may be because investor attention is on shorter-term risks. In our opinion, an opportunity is created when the share price lags the fundamental improvements. Kia has made significant inroads in the electric vehicle space. This ‘good news’ is yet to be reflected in the share price. At the same Kia it has an attractive and sustainable dividend yield, which is helpful against volatile market conditions.

Legislation - China’s state-owned enterprises

Investors tend to focus on China’s headline growth figures, which have been disappointing. This means they miss how the country is trying to reform its capital markets in part to encourage sensible investing at home and attract global capital.

One little-noticed theme is how the government is reforming state-owned enterprises, setting new performance targets often focused on return on equity, including requirements to return set proportions of cashflow in dividends. This has resulted in some favourable outcomes for shareholders.

One example that we hold is Sinotrans, one of the largest logistics companies in China. Sinotrans played a key role in China’s ‘Belt and Road’ initiative by providing international rail freight connections across routes as widespread as China-Germany and China-Laos. It now offers marine, rail and air freight forwarding, international express, shipping agency, and other services. Sinotrans trades on a P/E of 4.4x and a dividend yield of 8.3% and is growing its value per share at 22.2%[2].

Buybacks

Korea has seen some interesting developments. Signs of progressive shareholder return policies have created some enthusiasm towards the beaten down areas of the market. Korea’s finance minister vowed to narrow the ‘Korean discount’, encouraging companies to boost stock valuations. On the corporate side, buybacks and dividends are surprisingly positive.

In some instances, buybacks are occurring in companies where no dividend payments have ever been made. In part this reflects the fact that managements have confidence in their businesses and view the depressed share price as an attractive way to allocate capital.

In China, online retailer Vipshop has continued to grow its profits and improve margins, despite the macro weakness in the economy. Buybacks have been generous, with the company announcing $500m repurchase facility in 2021 and increasing it by $500m in 2023.

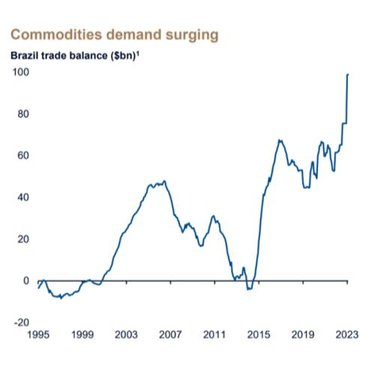

Commodities demand – Brazil

Other emerging markets are booming. With its abundance of energy and commodities, Brazil is a prime example. As an agricultural heavyweight, supplying soya beans, corn, beef, coffee and sugar to many parts of the world, its economy is thriving. This is evident in its record trade balance. Exports have been supported by a bumper harvest, while imports are down due to increasing self- sufficiency in energy. Brazil is also one of several emerging markets whose monetary policy has diverged from developed markets as inflationary pressures ease. Brazil’s central bank was early to take a hawkish stance on inflation in the wake of the Covid pandemic and started raising interest rates in March 2021, a full year ahead of the Federal Reserve. Having got ahead of the curve, it started to cut interest rates in August 2023 and has carried on doing so.

As a result of this booming economy, substantial dividends are available in the Brazilian market, offered by companies with good growth prospects and attractive valuations.

The financial sector has benefited from commodity demand, particularly in agriculture. One beneficiary is state-owned Banco do Brasil, the leader in the fast-growing agribusiness sector. This is leading to higher loan growth and lower non-performing loans.

Banco do Brasil has a strong market position in a higher yielding credit environment, with around 60% share of rural loans. Yet the stock is trading on a p/e of 4.2x with a dividend yield of over 9%. This is not far behind the level of a 10-year Brazilian government bond yield, but on an equity that is very undervalued and which has been growing its value per share[3] at over 20%. We expect the share price to keep pace with the improving outlook.

Emerging markets – an attractive combination of growth and income?

While the favourable income characteristics we’ve described above can’t be ignored, we would still advise investors to look to emerging markets for long-term growth. In general, high dividend yields tend to be associated with mature companies with low growth rates. Yet we find a number of companies in emerging markets that continue to grow rapidly, but also generate an attractive income. This favourable growth and income combination is likely to create value for investors over the long run.

[1] Source Artemis, Bloomberg MSCI 31 December 2023

[2] Source: FactSet, Artemis as at 18 January 2024

[3] Value-per-share (VPS) is a combined measure of earnings, cash flow, operating profits, dividends and asset value per share.