Investing in electrification: insights from the Polar Capital Smart Energy Fund

20 MAR, 2026

By Thiemo Lang from Polar Capital

The Polar Capital Sustainable Thematic Equity team expects electricity’s share of global energy consumption to increase from around 20% today to nearly 60% by 2050. Thiemo Lang, Senior Portfolio Manager of the Polar Capital Smart Energy Fund, discusses how the portfolio is positioned to benefit from this long-term structural shift. He also shares reflections as the Fund approaches its five-year anniversary later this year and outlines his outlook for the next five years.

The main drivers and the biggest challenges behind decarbonisation

Decarbonisation has been driven by global initiatives aimed at reducing carbon emissions by shifting to carbon-free power generation and improving energy efficiency. Decarbonisation and the electrification of end markets are closely connected.

Short-term policy and geopolitical developments can introduce volatility, particularly around subsidy regimes, trade restrictions and supply chains for critical materials. However, the Fund is designed to focus on solution providers rather than outcomes that depend heavily on policy. Many of our holdings benefit from electrification, efficiency gains and infrastructure investment regardless of the exact pace or direction of individual policy measures.

This is particularly visible in the recent surge in demand from AI data centres. More broadly, geopolitical uncertainty tends to reinforce the case for energy security, grid resilience and more localised supply chains – factors that strongly align with the Fund’s core investment themes.

The most interesting investment opportunities in Smart Energy

The most compelling opportunities today lie at the intersection of rapidly rising electricity demand and structural bottlenecks across the system. This dynamic is especially visible in AI infrastructure, where data centre operators are increasingly limited by how quickly they can secure new power connections. Grid constraints, permitting delays, the intermittency of renewables, and shortages of key electrical equipment– such as transformers, switchgear and cables – have all become significant obstacles. As a result, investment is accelerating not only in grids but also in behind-the-meter solutions, including onsite generation and large-scale battery systems that help operators manage peak loads and speed up project timelines.

Over the coming years, access to reliable and sufficient power – rather than computing hardware – is expected to become the main constraint on AI deployment. The current data centre build-out is therefore shifting focus from simply reducing “time to power” to improving overall efficiency. Because of transmission losses in the grid, power conversion inefficiencies and the intensive cooling requirements of liquid-cooled chips, the electricity needed at the source can be roughly double the amount used for computation itself. This is driving strong demand for energy-efficient electrical infrastructure, including transformers, power semiconductors, power supplies and cooling systems – areas where the Fund has meaningful exposure.

Beyond investments tied to the build-out of IT power infrastructure, the broader “electrification of everything” trend creates opportunities across transportation, buildings and industrial sectors. Assuming no major external shocks, we expect visibility in industrial electrification segments to improve significantly. With inventories currently very lean, this should particularly benefit industrial semiconductor companies supplying the automation sector.

Global energy storage systems (ESS) are expected to maintain strong capacity growth in 2026, exceeding 40% year-on-year. This expansion is supported by rising grid stability requirements, increasing electricity demand from AI-driven data centres, and continued improvements in system costs and efficiency. At the same time, expanding revenue opportunities in capacity and ancillary services markets are strengthening the investment case for storage.

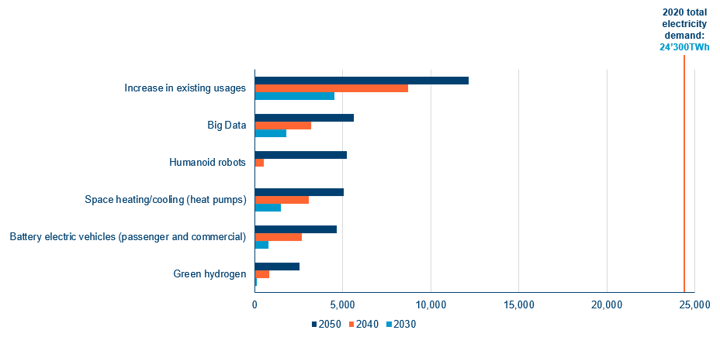

2026 is also likely to mark the first major rollouts of humanoid robots. Rapid progress in AI, together with declining hardware costs, is accelerating this shift and enabling robots to move beyond traditional industrial applications into services and households. As humanoid robots become more advanced and widespread, their energy consumption is becoming a more important factor affecting their overall economics. Energy-efficient robots will be able to operate longer on a single charge, require fewer battery replacements and incur lower maintenance costs, ultimately improving their total cost of ownership.

Implementing those opportunities to construct a diverse, thematic portfolio

The Fund is organised around four core investment clusters that capture the electrification megacycle: clean power generation, energy transmission and distribution, energy conversion and storage, and energy efficiency.

Within each cluster, we invest across a range of subsectors and geographies to maintain diversification and limit exposure to any single technology or regulatory risk. Portfolio construction is driven by bottom-up fundamental research, with sustainability analysis fully integrated into the investment process.

This framework enables the portfolio to capture multiple sources of value creation across the energy system – from upstream electricity infrastructure to downstream efficiency improvements in data centres, factories and building – rather than depending on a single technology or policy outcome. Position sizes are determined by conviction, liquidity and risk contribution, ensuring that no individual theme or holding dominates the overall portfolio.

Why do renewable power producers currently represent only a small portion of the portfolio?

Renewable power generation is a key component of decarbonisation, and the expansion of solar and wind capacity over the past two decades has been remarkable. However, as the share of solar and wind has already grown significantly in many developed markets, their intermittent nature can influence supply and pricing during periods of high generation. As a result, any further expansion of renewable power capacity will need to be supported by additional investment in grid infrastructure and energy storage solutions.

Battery-based storage solutions are well suited for daily load shifting but are not ideal for seasonal storage. One potential way to store surplus renewable electricity over longer periods is by converting it into green hydrogen. While we still believe this could become a viable long-term solution, we do not expect green hydrogen storage to see a more meaningful rollout before the next decade.

As a result, although we expect solar and wind capacity to continue expanding in the coming years, we do not anticipate growth in this segment to match the pace of investment expected in grid infrastructure and battery storage solutions.

Outlook for the next 5 years

The first five years have shown both the cyclicality and resilience of clean energy investing. The period included market rotations, rising interest rates and shifting policy environments, reinforcing the value of active management, fundamental research and diversification across the value chain.

The energy transition is not linear, with technologies and end markets evolving over time. Focusing on companies with strong balance sheets, technological leadership and exposure to multiple structural growth drivers has been key to navigating volatility while maintaining long-term thematic exposure.

The “electrify everything” trend is expected to accelerate over the next five years. AI data centres are emerging as a major new demand driver, placing increasing pressure on power generation and grid infrastructure. Solutions such as onsite generation, battery storage and grid expansion are being explored, while nuclear power is also seeing renewed interest due to its ability to provide reliable baseload power.

Beyond AI, other regions continue to see strong demand from electric vehicles, heat pumps and HVAC systems. Electricity currently accounts for around 20% of global energy use and could rise to nearly 60% by 2050, creating significant investment opportunities across multiple end markets.

Overall, the energy transition is entering a new phase – the electrification megacycle – with growing demand from AI, electrified transport, industrial automation and emerging technologies such as humanoid robots and physical AI.