Investing in European defence to decorrelate portfolios

15 JAN, 2026

By Anthony Penel, European Equity Portfolio Manager at Edmond de Rothschild AM

With cyclical sectors dominating European markets, the key to building a resilient portfolio lies not only in performance, but also in diversification. Asset correlation has become a critical parameter, enabling investors to better distribute risk and protect portfolio stability amid shifting macroeconomic conditions.

According to Modern Portfolio Theory, developed by Harry Markowitz (Nobel Prize in Economics, 1990), returns depend not only on individual asset performance, but above all on correlations between assets. Adding low-correlated equities to a portfolio can reduce overall volatility by diversifying risk sources. An individual asset may be volatile on its own, but its differentiated behaviour can smooth portfolio return fluctuations and improve the risk/return profile for investors.

Since the invasion of Ukraine, the European defence sector has gradually detached itself from broader equity markets. Unlike traditional MSCI Europe sectors—driven by growth expectations, interest rates and consumption—defence stocks are supported by their own structural drivers: rising national military budgets, strategic rearmament, industrial capacity renewal and multi-year government procurement programmes. These dynamics are far more closely linked to geopolitics, international alliances and shifts in national security doctrines than to traditional economic cycles. Moreover, with the so-called “peace dividend” now under question, the sector is undergoing a structural re-rating after several decades of subdued growth.

As a result, price movements within the defence sector tend to reflect geopolitical tensions and government announcements rather than macroeconomic developments or equity valuation debates (such as AI bubble concerns or monetary policy decisions). Even worries over sovereign debt sustainability in some countries have failed to derail defence stocks’ trajectory.

It is therefore unsurprising that, since summer 2025, numerous European sovereign funds have emerged in the investment landscape. These initiatives often align with the recommendations of Mario Draghi’s September 2024 report, “The Future of European Competitiveness”, which explicitly calls for strengthening the EU’s defence capabilities.

We can now draw initial data-driven conclusions on a theme that has become a must-have in active equity strategies. Our analysis uses the Bloomberg Europe Defence Select Net Return Index, compared with the MSCI Europe Net Return Index and its GICS Level 2 sector components, notably Capital Goods, which includes most defence stocks.

Over the past 52 weeks (since November 2024), volatility readings show that European defence ranks among the most volatile sectors, comparable to highly cyclical industries such as automotive, and significantly more volatile than Capital Goods.

Volatility – Weekly, Nov 24 / Nov 25

While volatility is often viewed as a deterrent, investors should consider a sector’s decorrelation effect within portfolio allocations. A volatile but low-correlated sector can actually reduce overall portfolio volatility.

Correlation (ρ) with MSCI Europe – Weekly, Nov 24 / Nov 25*

Defence stands out as one of the least correlated sectors, on par with real estate and telecommunications, and shows the strongest decorrelation among cyclical industrial sectors.

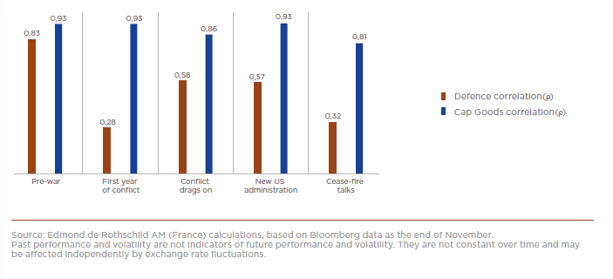

However, current market conditions differ markedly from the pre-war environment. The Russian invasion of Ukraine on 22 February 2022 marked the beginning of a new regime. Analysis across multiple observation periods shows that the statistical behaviour of the defence sector has changed significantly.

While the relative volatility of Capital Goods versus the broader market has remained broadly stable, defence sector volatility has increased, though without becoming excessive. The evolution of correlation coefficients is even more striking.

Correlation (ρ) with MSCI Europe – Weekly, Nov 24 / Nov 25

Before the war, defence stocks exhibited reasonable correlation with MSCI Europe, similar to Capital Goods. The outbreak of the conflict triggered a sharp structural break, with correlation dropping to extremely low levels (0.28, R² of 8%). After rising modestly over the following two years, the most recent period—shaped by ceasefire discussions—has once again seen defence display very high levels of decorrelation, albeit at the cost of higher relative volatility.

An analysis of seven sovereign funds investing across the eurozone, the EU and Europe—based on daily NAV data since the launch of the most recent strategy on 1 August 2025—confirms this trend. The lower the correlation with MSCI Europe, the higher the correlation with the defence theme, reflecting defence exposure within each fund.

Naturally, volatility varies depending on defence allocation, yet results remain highly acceptable, with annualised volatility ranging between 10% and 15%.

Incorporating a “defence sleeve”—driven by geopolitical rather than economic factors—helps reduce a portfolio’s correlation with global equity markets. Despite higher volatility, this thematic sub-sector enhances overall portfolio stability, cushions periods of market stress and improves the risk/return trade-off, offering investors an additional source of long-term performance and resilience.