What does the latest European sustainability legislation mean for investors?

15 JUL, 2024

By Schroders

Authors: Nathaële Rebondy, Head of Sustainability Europe & Elisabeth Ottawa, Head of Public Policy Europe at Schroders.

The latest significant milestone in European sustainable finance regulation was the publication on May 14th of the European Securities and Markets Authority (ESMA) guidelines on ESG fund names. The aim of the guidelines is to ensure that investors are protected from unfounded or exaggerated claims in fund names, and to provide asset managers with clear criteria for assessing which sustainability-related terms are appropriate to use in fund names.

Schroder's experts analyse the details of the fund naming guidelines. While also review some of the trends regarding ESG fund labels in Europe. And, following the European Parliamentary elections that took place from 6-9 June, Schroder's experts look at what has been achieved in this period and what is to come.

What makes up a designation?

Nathaële Rebondy, Head of Sustainability Europe at Schroders.

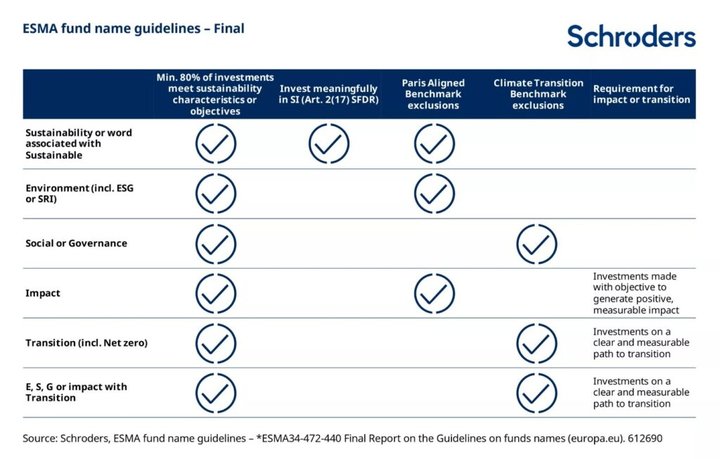

ESMA's guidelines on fund names, summarised in the table below, have several important implications. A key point is that all funds with sustainability/impact/ ESG etc. related terms in their names must ensure that at least 80% of their investments meet sustainability characteristics or objectives. This is in line with the general fund name policy in the US and goes beyond the specific sustainability regime in the UK, which requires 70%. This 80% threshold could, for example, pose a potential problem for private market funds, which tend to hold larger cash reserves in their growth and divestment phases.

Another important point is that funds with the term "sustainable" (or words related to sustainability) in the name must invest "significantly" in sustainable investments. As the guidelines do not define "significantly", this is open to interpretation. These funds must also conform to the exclusions from the Paris Agreement Benchmarks (PAB). These include, in particular, coal, oil and gas, as well as electricity production from fossil fuels, with different thresholds.

However, this "significant investment" requirement does not apply to funds that have the term "impact" in their designation. Instead, these funds must comply with the BAP exclusions and their investments must be made with the objective of generating a positive and measurable social or environmental impact alongside a financial return.

Similarly, where a fund's name combines any ESG-related or impact investment terms containing the word "transition", the requirement to "invest meaningfully" does not apply. Instead, these funds must apply climate transition benchmark exclusions and ensure that investments are on a clear and measurable path to transition.

Indeed, the term "transition" is used very specifically in the guidelines. Given that these funds are required to have investments with a clear and measurable trajectory towards transition, we understand that such funds cannot be solution-oriented, i.e. investing in companies/securities that facilitate transition, but that the investments themselves must be in the process of transition.

For example, words like "upgrading" or "transformation" will trigger the same requirements as "transition". Surprisingly, "net zero" falls into the transition category and not the environment category.

And finally, it is important to understand that the guidelines apply to both active and passive funds, regardless of the benchmark, and that they also apply to closed-end funds, even if these are no longer open to new investors.

When do the new guidelines enter into force?

Elisabeth Ottawa, Head of Public Policy Europe at Schroders.

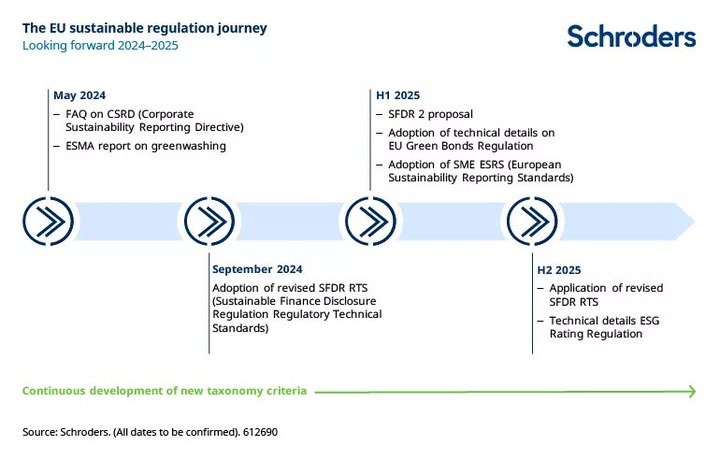

The guidelines need to be translated into all official EU languages and will enter into force three months later. Therefore, we expect them to enter into force in the third or fourth quarter of 2024 for new funds. Existing funds will have a transition period of an additional six months, so they will apply in the first or second quarter of 2025.

The asset management industry will now digest the guidance and we do not rule out further work by ESMA in the coming months on Q&A as firms seek further clarity.

What's on the horizon for sustainable EU regulation?

The EU parliamentary elections were held from 6 to 9 June. The results in some countries have produced some surprises. Overall, the big pro-European parties (EPP Conservatives, S&D Social Democrats and Renewal Liberals) continue to hold a strong majority in the European Parliament. Several key MEPs for European regulation of sustainable finance will remain in their seats. This means that we can expect continuity on the sustainability agenda.

Looking back, the EU has met the target set in 2018 to include every element of the investment chain in sustainable regulation. However, there are still some important updates to come in the next two months. We look forward to the publication this month of a Q&A with Frequently Asked Questions on the Corporate Sustainable Reporting Directive (CSRD). An ESMA report on greenwashing has just been published. It is not a legislative report, but it will certainly inform the European Commission's considerations on a future Sustainable Financial Disclosure Regulation (SFDR).

Looking ahead, we expect the revised SFDR RTS (regulatory technical standards) to be adopted in September. This has been delayed due to the elections, which means that their entry into force is unlikely until the second half of 2025.

At the earliest, early next year, we expect a proposal for SFDR 2, as well as technical details on the EU green bond regulation and more information on sustainable reporting standards for small and medium-sized enterprises.

And an ongoing project over the next few years is the development of the new taxonomy criteria, which are still being refined.

Changes in European country sustainability labels

Nathaële Rebondy, Head of Sustainability Europe at Schroders.

European national labels continue to be important for fund distributors. This year, the guidelines on national labels have been updated, in particular the French "Label SRI", the Belgian "Towards sustainability" and the Austrian "Umweltzeichen". Some of these labels have existed for many years.

The latest updates mainly concern strengthening the requirements around fossil fuels and exclusions. There are also more precise requirements related to active ownership, namely commitment and voting. But, of course, not all labels have introduced the same changes.

This will lead asset managers to take a hard look at their funds with these labels. They will have to consider whether it still makes sense to keep the label(s) from a commercial point of view. For example, European funds are sold in other jurisdictions, such as Asia, where client demand may be different.

Products need the right labels for the right markets. This should be based on clients' interests and assets. If a significant change in investment strategy is necessary to maintain a specific label in a particular market, this may not be the right outcome for fund investors in other parts of the world.

We therefore anticipate that the number of funds carrying these labels may decline in the short term, although there could be an upturn again in the future if new funds are launched that meet the labelling requirements from the outset.

There is a lot of fragmentation in labelling regimes and we are still waiting for a label that can work across Europe to improve consistency.