Leveraging opportunities in emerging markets

13 AUG, 2025

Author: Ygal Sebban, director of the emerging markets equity team at GAM Investments

To invest successfully in emerging markets, it is necessary to deeply understand global macroeconomic trends, including trade flows, geopolitical changes, and the structural challenges of developed markets. Capital flows and risk perception in emerging markets are often determined by the dynamics of developed markets, so it is essential to adopt a top-down and risk-sensitive approach.

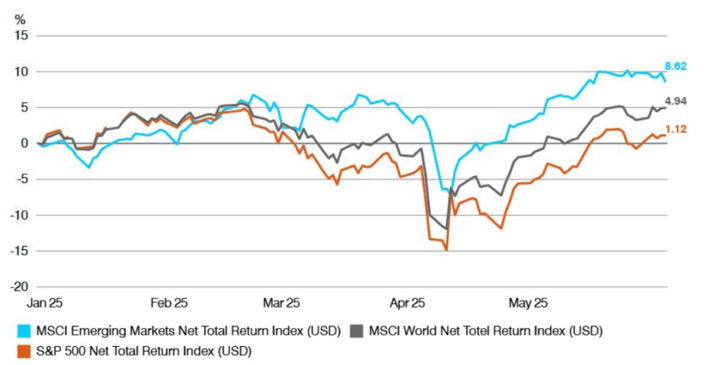

Chart 1: Year-to-date (YTD) performance of EMs versus the MSCI World and the S&P 500

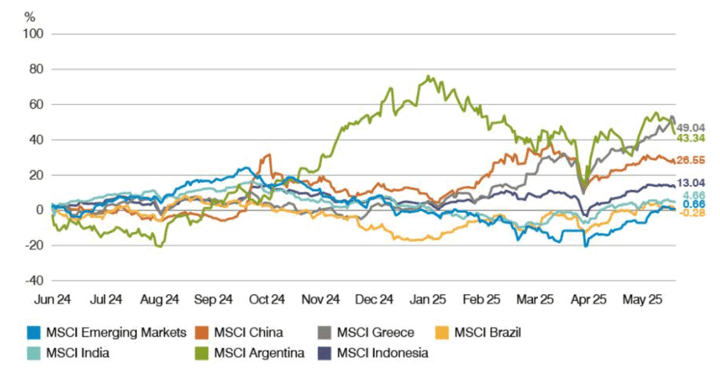

Chart 2: Divergence in the performance of emerging markets

Performance from May 31, 2024 to May 30, 2025

Emerging markets have performed well this year, outperforming global markets. The MSCI Emerging Markets (USD) index has returned 8.62% so far this year, outperforming both the MSCI World index, with 4.94%, and the S&P 500, with 1.12% (all in USD, as of May 30, 2025). This superior performance highlights the importance of selection and active management in seizing the right opportunities.

The dispersion of performance among emerging markets underscores the importance of active management. Markets in the emerging universe do not move in unison, but each responds differently to macroeconomic forces, political events, and structural changes. This divergence creates both opportunities and risks that passive strategies may overlook.

We assess emerging markets based on their relative attractiveness, determining risk-adjusted valuations, growth prospects, momentum, and quality. The main factors driving returns, such as currency, GDP growth, political stability, and exposure to global themes such as artificial intelligence (AI) and energy transition, are evaluated using proprietary models that incorporate real interest rate differentials, volatility, and balance of payments.

Current market focus: China, Greece, and Argentina

Currently, we are focusing on three markets: China, Greece, and Argentina. While Greece and Argentina are quite isolated from the trade war, our position in China emphasizes themes that are also resistant to such risks.

China

It remains a key market, backed by a shift towards more growth-friendly policies, reaffirmed in the latest Government meetings. The 5% growth target for 2025 points to the continuity of stimulus measures. We are particularly optimistic about the software and discretionary consumption sectors, and we prefer service consumption to goods consumption, particularly travel, local service platforms, artificial intelligence, and video games. These areas benefit from attractive valuations, an improvement in earnings momentum, and the advantages of two policies: "Digital China" and the "national" technology drive. Companies like Kingdee and Kingsoft have surprised on the upside with their results, driven by operating leverage and cost discipline.

Greece

It stands out for its solid risk-adjusted profitability profile following its upgrade to investment grade. We forecast GDP growth above consensus, of 2.5% in 2025, backed by prudent fiscal policy and structural reforms. Persistent primary surpluses should drive a steady reduction. We are optimistic about Greek banks, whose return on capital potential, including share buybacks, is increasingly attractive.

Argentina

It is also a country in the spotlight, thanks to its macroeconomic recovery. Since December 2023, the country has implemented bold reforms in deregulation, privatization, and fiscal discipline. A successful tax amnesty has attracted $22 billion in capital inflows, while annual inflation has dropped dramatically, from 211% at the end of 2023 to 47% in April 2025. Overall inflation is expected to continue its downward trajectory, reaching 37% in 2025 and 15% in 2026, supported by tightening monetary policy and exchange reform. With private credit expanding from a low level and banks expected to play a key role in Argentina's recovery, we see a significant upside potential in the banking sector, an opportunity we believe is not yet fully discounted.

These markets offer attractive opportunities backed by favorable macroeconomic trends, reform momentum, and positive earnings outlooks.

China: Still a market to invest in

We continue to see selective opportunities in China, especially in areas backed by structural trends and proactive policies. The macroeconomic environment has changed significantly, and the Government has prioritized growth and private sector confidence over the previous focus on "common prosperity".

Since September 2024, China has shown coordinated support in its monetary, fiscal, real estate, and capital market policies. Liquidity conditions have improved and we see signs of stabilization in the real estate market, which could contribute to improving overall confidence, although it is still unlikely to return to pre-pandemic activity levels.

We are optimistic about China's prospects, driven by the GDP growth target of 5% for 2025, a combination of more accommodative policies, which includes a fiscal deficit of 4%, and specific support for consumption, the real estate sector, banking, and capital markets. Recent meetings on economic policy continue to indicate that new stimulus measures are being considered.

We focus on the software and discretionary consumption sectors, where we see attractive risk-adjusted returns. In discretionary consumption, we lean towards areas driven by services, such as travel, local platforms, artificial intelligence, and video games, which trade at the lower end of their five-year valuation ranges and show an improvement in earnings momentum. The recent results of major internet and e-commerce companies have exceeded expectations, driven by strong operating leverage and product innovation.

In the software sector, China's advanced AI capabilities, illustrated by DeepSeek, and national strategies, such as "China Digital", as well as technological localization continue to support growth. Although we remain attentive to geopolitical risks and tariffs, which can affect exporters, we avoid the most exposed areas and focus on topics less vulnerable to external impacts.

Tariffs and emerging markets: risks and responses

Despite several changes in US tariffs, such as temporary reductions or technological exemptions, and signs of negotiation between China and the United States, international trade remains under pressure. Tariff rates are significantly higher than anticipated at the beginning of the year, which hampers international trade, business confidence and, ultimately, global growth. However, we believe that the secular trends of emerging markets remain intact, which gives them resilience in a changing landscape.

While tariffs pose challenges for EMs, their impact varies by country, and several countries have demonstrated their ability to respond effectively. Although tariffs can alter trade flows, put pressure on exporters, and increase production costs, their severity largely depends on the economic structure and sectoral exposure of each country. We believe that the direct impact of tariffs is more pronounced in economies that impose them, such as the United States, than in emerging markets in general. Most emerging markets do not import significant consumer goods from the United States, so inflationary effects tend to be limited. Instead, the main consequence is the pressure on emerging market exporters to the United States, a risk that we actively manage by avoiding the most exposed companies and sectors.

However, emerging markets are not uniformly vulnerable. Demand-driven economies, such as India and Brazil, are more insulated than others dependent on exports, like Mexico or Vietnam. China, for example, has responded with specific stimuli, tax relief, and the acceleration of its transition to higher value sectors, such as software and artificial intelligence, areas that benefit from political support and localization trends.

In broader terms, tariffs are accelerating the divergence between the growth trajectories of emerging markets and developed markets, often to the benefit of the former. By promoting self-sufficiency and regional trade, they are reinforcing structural changes that are already occurring in many emerging markets. For investors, this creates new opportunities in markets focused on innovation, internal growth, and resilience supported by policies.

A weaker US dollar: what it means for emerging markets

Historically, the weakness of the US dollar has supported the profitability of emerging markets, as both show a strong inverse correlation. This benefits the assets of emerging markets through three main channels:

- Capital flows: the depreciation of the US dollar attracts the entry of foreign capital, as investors seek higher returns, which in turn supports business profits and economic expansion.

- Debt: a weaker dollar reduces the burden of dollar-denominated debt for governments and companies in emerging markets.

- Commodities: commodity prices are crucial, as many emerging markets are commodity exporters. Commodity prices tend to rise when the US dollar weakens, which provides an extra boost to economic performance.

In addition, a weaker dollar gives central banks in emerging markets greater policy flexibility, allowing them to relax monetary conditions or maintain rates. Conversely, a stronger dollar usually forces emerging markets to tighten their policy defensively, as seen in 2018.

Looking ahead, we anticipate further depreciation of the US dollar, supported by fiscal stimuli and inflation expectations. Structural factors, such as concern about the fiscal sustainability of the US and the undervaluation of emerging market currencies, should also provide a medium-term boost to emerging market currencies.

Positioning for what's to come

Emerging markets continue to offer attractive opportunities for investors who know how to navigate their complexity with discipline and deep knowledge. Although global headwinds persist, such as tariffs and geopolitical tensions, many emerging markets are demonstrating their resilience thanks to structural reforms, domestic demand, and alignment with transformative global trends, such as artificial intelligence and the energy transition. The weakness of the US dollar further improves the outlook, as it favors capital flows, eases the debt burden, and boosts economies linked to commodities.

Combining top-down macroeconomic analysis with bottom-up stock selection and focusing on sectors backed by policies and led by innovation, our goal is to identify the most attractive opportunities and actively manage risk. In our view, the changing landscape of emerging markets is not only susceptible to investment, but is becoming an essential component of a forward-looking global portfolio.