Market concentration in three charts

21 NOV, 2025

AUTHOR: Diana Wagner, Equity Portfolio Manager at Capital Group

With the S&P 500 index near historical highs, has the peak of dominance of the Magnificent Seven ("Mag 7") group of stocks been surpassed? It seems so, and this represents a healthy move away from the extreme concentration that had raised concerns about risks to investors' portfolios.

After three years in which the Magnificent 7 represented most of the annual return of the S&P 500, now there are increasingly more companies contributing; as of September 30, stocks not included in the Magnificent 7 accounted for 59% of this year's return. A new breadth of the market could support the rebound of the S&P 500 index after the crash recorded at the beginning of 2025. The index has recorded a 36% increase from the low reached on April 8.

The increase in valuations of companies included in the index and greater clarity on tariffs and interest rate cuts could help support the US stock market, which has underperformed compared to the European and other areas. Looking to 2026, we believe there are favorable winds that should stimulate earnings growth and support the market, such as the stimuli derived from tax reform and greater political certainty. There are numerous opportunities outside of the Magnificent 7 and the growth we have begun to observe this year is destined to continue.

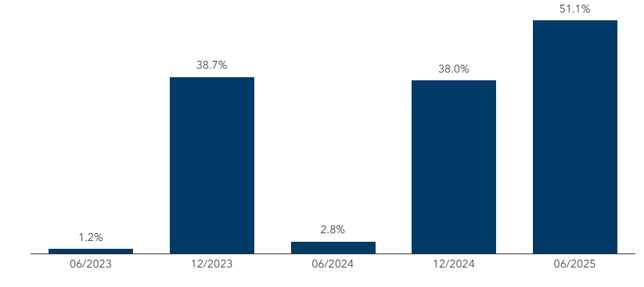

The market breadth is widening

The market breadth is increasing after hitting a low in June 2023, when the Magnificent 7 dominated the returns of the S&P 500. On a semi-annual basis until June 30, 2025, the percentage of stocks that recorded returns higher than the median of the Magnificent 7 reached 51%, equivalent to 251 stocks. This is an increase from 1% in June 2023, when this only concerned five companies. Another significant signal: since April 2, when the White House announced proposed tariffs against other countries, the percentage of equity shares traded above their 200-day moving average has risen from 16% to 64% at the end of last month.

June 2023 marked the peak of concentration

Percentage of all other S&P 500 index titles above the weighted average yield of the Magnificent 7

Past results are not indicative of future results. Source: FactSet. The percentages reported below are based on six consecutive six-month periods between June 2023 and June 2025 and represent the percentage of titles in the S&P 500 index not belonging to the Magnificent 7 that recorded a total return higher than the weighted average of the total return of the Magnificent 7. Data as of June 30, 2025.

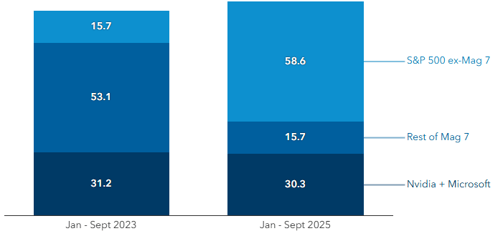

Nvidia is changing the equation

The meteoric rise of Nvidia — which holds almost a monopoly on data center semiconductors at the base of the artificial intelligence boom — has pushed giants like Apple, Microsoft and Alphabet (Google's parent company) to compete for the title of the world's most valuable company, with a valuation of 4.5 trillion dollars. The market breadth would potentially be greater if not for Nvidia's dominance. From the beginning of the year to September 30, Nvidia contributed 20% to the total return of the S&P 500. Nvidia's dominance has reduced the impact of the other Magnificent 7, except for Microsoft with 14%.

S&P 500 stocks excluding the “Magnificent 7” have become the main contributors to the benchmark index return

Contribution to the total return of the S&P 500 index (%)

Source: FactSet. The rest of the Magnificent 7 includes Alphabet, Amazon, Apple, Meta, and Tesla. The S&P 500 stocks excluding the “Magnificent 7” represent the other 493 companies in the index. Data as of September 30, 2025.

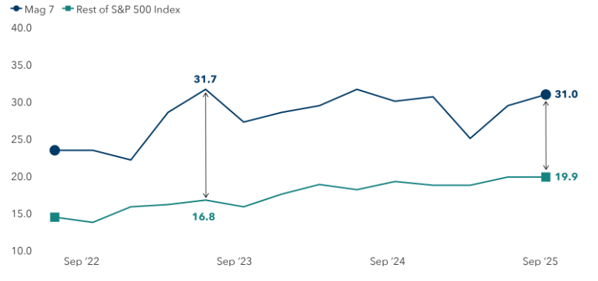

Valuations are less divergent

After a significant divergence two years ago, the price/earnings ratio is slowly increasing, indicating that long-term growth projections are getting closer. As of September 30, the Magnificent 7 were trading at 31 times expected annual earnings, compared to 20 times for the other 493 companies. What seems to be emerging is a stabilization of optimism for the Magnificent 7 and an increase in confidence for the rest of the market. Investors are showing a greater willingness to invest in the earnings growth potential of other companies. This suggests a more balanced risk/reward profile between the mega-cap tech and the broader market, making valuation rigor increasingly important.

Valuations outside the Magnificent 7 have increased

Expected price/earnings ratio for the next 12 months

Source: FactSet. The expected price/earnings (P/E) ratio is calculated by dividing the share price by the consensus estimates on expected earnings over 12 months. The expected P/E ratio of the Magnificent 7 is the market capitalization weighted average. Data as of September 30, 2025.

Where the market could expand

Market pressures - such as the impact of artificial intelligence, the slowdown in production outside of data center development, and rising interest rates - have compressed valuations in some sectors. Take for example companies whose stocks have fallen due to the euphoria generated by artificial intelligence, such as IT consulting firms and software providers. These could benefit from companies intending to integrate agent-based artificial intelligence or exploit the data embedded in their own software. The investment cycle in artificial intelligence is expected to be massive, with a potential increase in opportunities for companies in the coming years.

Nvidia, for example, predicts a cumulative expenditure of 4 trillion dollars by 2030. If this were the case, the magnitude of the expenditure could benefit some utilities capable of supporting the energy demand of data centers, along with semiconductor manufacturers and lesser-known companies that provide electrical, mechanical, and hydraulic equipment. However, in the industrial sector, the artificial intelligence boom and uncertainties related to tariffs have created a divergence in stock prices and valuations.

Many end markets are struggling from 2023 and companies operating in the transportation, equipment rental, and corrugated cardboard sectors are looking for efficiency improvements to increase margins. If the market continues to expand, banks could take part in it. Regulatory authorities are considering a plan to relax capital requirements that could increase loans across all sectors. Banks have had to face stricter restrictions after the 2008 financial crisis. We could witness a new market expansion, whether it is an improvement in scenarios outside of companies linked to artificial intelligence, or a recovery of the industrial economy.