Market implications of the Middle East conflict

23 MAY, 2024

By Duncan Lamont

More than seven months into the Israeli-Palestinian war. Matthew Michael, Investment Director, and Duncan Lamont, Head of Strategic Analysis at Schroders, explain the consequences of this conflict on the markets.

By: Matthew Michael, Investments Director at Schroders & Duncan Lamont, CFA, Head of Strategic Analysis at Schroders.

Market volatility could increase in the short term, but so far the impact on global markets has been limited. From a purely market perspective, the most immediate potential impact is higher oil and gold prices due to the risk of oil supply disruption from the Middle East and investors' search for safe havens such as gold holdings.

Oil prices have risen this year, but the rise has more to do with US production not rising as expected, OPEC extending production cuts into the second half of the year and Russian refinery capacity being disrupted by Ukrainian drone attacks. There seems to be a broad consensus that de-escalation will be the most likely outcome, even though the Iranian attacks have been much larger than expected. The risk premium in the oil market, specifically related to tensions in the Middle East, is therefore very limited at the moment. The current price is well below the highs of the 1970s and the previous bull market, both in nominal and inflation-adjusted terms.

Overall, commodity geopolitical risk premia remain low despite recent events and the upcoming US elections.

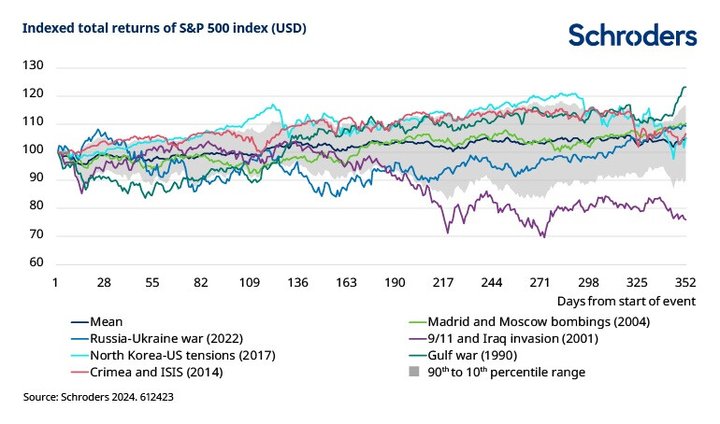

Duncan Lamont, CFA, head of strategic analysis at Schroders, analyses the background and effects of situations such as the current one on markets: ‘Stock markets tend to fall in the short term when geopolitical risk increases, as markets reassess risk. Past performance is not a guide to the future, and every situation is different, but historically they have started to recover strongly within months. Staying the course rather than reacting has worked well.'

The chart below shows the total return of the S&P 500 index in the year following other events that led to an increase in geopolitical risk.

What if the conflict escalates?

Schroders' economic analysis team analyses the potential economic impact of a wider conflict. Periodically, the team designs a series of risk scenarios designed to examine the impact of potential events and risks around some of the underlying assumptions in its baseline economic forecasts.

One such scenario is the ‘Middle East war’, which assumes that localised fighting in Israel spreads throughout the region and draws Western nations into the conflict as well. In this scenario, the war is assumed to disrupt not only major shipping channels, but also the supply of oil, causing wholesale prices to head towards $150 per barrel.

In this case, the macroeconomic impact would likely be stagflationary for the world economy. Rising inflation caused by the commodity price shock could deal a severe blow to business confidence, which would likely reduce capital spending at a time of great uncertainty. The situation would force central banks to delay the start of rate easing. Delayed easing cycles could then weigh on growth in 2025.