Market outlook for the last months of 2025

20 OCT, 2025

Will the last months of 2025 bring surprises, or will European and global markets slow down a bit? Here’s what the experts say.

Late-cycle outlook and emerging opportunities

Peter Branner, Chief Investment Officer at Aberdeen

We have based our outlook on the continuation of a “late-cycle” macroeconomic environment, in which the U.S. economy is slowing but avoiding recession, while official interest rates are being cut. In China, nominal growth has cooled, but policy support remains in place, and there is a rising emergence of “AI winners” within the corporate sector. Meanwhile, we expect further rate cuts in emerging markets as the focus shifts from containing inflation to supporting growth, and the U.S. Federal Reserve resumes easing.

Significant economic and geopolitical risks should be noted. These include a deterioration in the U.S. labor market, which could lead to a broader slowdown and a recession amid a “stall-speed” dynamic. However, a mini cyclical recovery is also possible now that the peak period of tariff uncertainty appears to have passed. Political interference in the Federal Reserve could destabilize inflation expectations and ultimately trigger a bond market decline. Given the political capital the Trump administration has invested in reshaping the Fed, this House View considers the risk of fiscal dominance to have increased. This is partly reflected in a steeper yield curve and changing correlations between inflation expectations and commodity prices. On the other hand, AI-driven productivity growth could lead to sustained supply expansion over the coming years.

Paul Diggle, Chief Economist at Aberdeen, added: “Taking all this into account, we have upgraded our view on emerging market equities and remain broadly positive on corporate risk. We are optimistic on short-duration bonds as diversifiers, though we expect yield curves may continue to steepen across countries. We maintain a positive view on infrastructure and direct real estate, and we expect the U.S. dollar to weaken.”

Emerging Market Equities

Aberdeen expects Chinese equities and emerging market equities more broadly to continue performing well. Valuations in these markets remain more attractive than in developed markets, and a weaker dollar should support earnings. The Chinese equity market, in particular, is increasingly becoming an “AI story,” driven by rising capital intensity among Chinese tech companies, which could follow the trajectory of large U.S. firms. While China’s macroeconomic backdrop remains a key determinant of equity performance, policy stimulus has outweighed the slowdown in growth.

Additionally, the initial impact of tariffs on China’s economy has been smaller than expected, thanks to strong non-U.S. export markets. However, transit tariffs and anti-dumping measures will gradually weaken this offset. Falling housing prices and weak consumer confidence also pose obstacles to Chinese economic activity, suggesting further growth deceleration. Efforts to reduce industrial overcapacity may help in sectors such as solar panels and electric vehicles, while financial conditions remain loose. Overall, however, policies appear insufficient to significantly boost nominal growth.

Emerging Market Debt

Aberdeen remains moderately optimistic on emerging market debt. Sovereign and corporate credit fundamentals remain generally solid (notably excluding Indonesia), and the cycle of rate cuts is likely to continue as the focus shifts from containing inflation to supporting growth and the Fed resumes easing. Market technicals are favorable after a period of low issuance and strong demand for non-dollar assets. Emerging market spreads have tightened following a period of strong performance, with investment-grade spreads at their lowest since 2007 and high-yield spreads at their lowest since 2018. Carry in emerging market debt remains attractive.

Duration

Duration signals are moderately positive, though Aberdeen’s House View anticipates a steeper yield curve. The short end of the bond curve may price in additional rate cuts due to stall-speed risks, temporary price disruptions from tariffs, and the arrival of a more moderate Fed chair. A basic overweight in duration in a late-cycle normalization environment offers conditional diversification amid these risks. The House View benchmark for duration is a global bond index with an average maturity of just over six years.

Nevertheless, Aberdeen expects yield curves to remain steep and potentially steepen further, particularly beyond 10 years. Debt and deficit levels are high in developed economies, with pronounced fiscal pressures in the U.S., U.K., France, and Japan. Political will for fiscal consolidation is lacking, while natural buyers are scarce at the long end as central banks shrink balance sheets and many pension and life funds have surpluses.

U.S. Dollar

Aberdeen maintains a slightly negative view on the U.S. dollar. This is based on the expectation of Fed rate cuts amid a slowing U.S. economy, which will reduce rate differentials with other economies, and on growing risks around the U.S. economic cycle and institutional environment. The dollar and many dollar-denominated assets are expensive by most valuation metrics cited by Aberdeen. However, consensus among many market participants is that the dollar is overvalued, potentially limiting the extent of underperformance.

Real Estate

Aberdeen remains moderately optimistic on global direct real estate. Following the deep post-pandemic recession, the property yield cycle is gradually recovering, despite economic and geopolitical uncertainty. There are fewer distressed assets, retail and office sectors are generating positive returns as prior structural issues fade, and data centers are performing well, becoming an increasingly important component of investor benchmarks. Investor confidence is increasingly positive, with global inflows rising year-on-year and more capital ready to invest. Liquidity is improving, and debt markets remain open. Spreads are more attractive in Europe, though the U.K. and U.S. need to catch up for prospects to improve further.

Infrastructure

Aberdeen maintains a positive view on infrastructure. However, tariffs and current energy market volatility may challenge investors in certain subsectors, particularly those closely tied to GDP, such as transport and commercial energy projects. Therefore, focusing on quality assets remains essential.

The House View also recognizes a strong overall capital-raising environment, with falling interest rates, a high global “capital reserve” for infrastructure, and structural factors supporting the sector. These include debt (tight public-sector balances requiring private capital), digitalization (AI growth and data exchange increasing demand for data centers and electrical infrastructure, alongside greater cybersecurity needs), and decarbonization (major improvements to power grids, shifts to sustainable transport, and investments in domestic energy production).

European ETFs: positive momentum carries into the final months of 2025

Renu Pothen, Consultant

The European ETF industry has been experiencing strong growth momentum in 2025, both in terms of assets under management and strong inflows.According to the LSEG Lipper report on the European ETF Industry Review for September 2025, the assets under management of the European ETF industry reached an all-time high of €2,412.8 billion by the end of September from €2,316.7 billion at the end of August. The performance of the underlying markets (+€59.3 billion) and the estimated net inflows (+€36.7billion) together contributed to the increase in assets under management of €96.0 billion for September. The total inflows in ETFs for the whole year of 2025 stood at €242.6 billion. The report goes on to further add that if the European ETFs can maintain their inflows at the current levels, the overall inflows for the whole year 2025 could reach a new all-time high, between €310.0 billion and €330.0 billion. As we head into the final months of 2025, these latest numbers continue to provide a positive outlook for the industry, which will unleash more exciting opportunities for investors.

Some of the best-performing European ETFs in the first half of 2025 included thematic ETFs focused on gold miners, defense, and European financials, particularly banks. The outlook for these ETFs remains positive and is expected to attract investor attention during the last few months of 2025 as well. Gold prices have already surpassed an unprecedented high of $4,300, underscoring its position as a safe-haven asset, especially during phases of uncertainty. The current rally, which is supported more by fundamental factors, is expected to continue through the end of 2025. Some of the major factors that are contributing to this surge in gold prices include a weakening dollar, uncertainty regarding the policy on tariffs, geopolitical concerns, and central banks globally buying gold to diversify their reserves away from US treasuries.

There have been major shifts in the defense policies of European countries, which will continue to open up more opportunities for investments into this theme. The NATO members recently committed to increasing their defense spending to 5% of GDP by 2035, a substantial increase from the previous goal of 2%. In addition to this, earlier this year, the European Union proposed an ambitious plan to mobilise €800 billion for defense spending under the ReArm Europe Plan/Readiness 2030. These initiatives not only point towards a shift in budget priorities across Europe but also create more opportunities for businesses within the defense sector.

The S&P Europe BMI Banks index has risen substantially by an impressive 73.89% year-to-date. The European Bank index has outperformed the US S&P 500 Bank index and the S&P Pan Asia BMI Banks index, both of which have increased by 25.48% and 22.25%, respectively, as per the data released in October by S&P Global Market Intelligence.The stellar performance, according to S&P Global, can be attributed to the robust quarterly profits, supported by strong non-interest income and increased trading income despite market volatility. To add to this, an increase in M&A activity within European Banks has also contributed to this upward trend. The European banks continue to be resilient even under severe economic downturns, as can be seen from the 2025 EU-wide stress test, which included 64 banks from 17 EU and EEA countries and covered 75% of EU banking sector assets.EU banks have also been maintaining strong capital positions, which allows them to support the broader economy even during adverse times. The exceptional performance of the European banking sector indicates a strong and stable financial system, making it a viable investment opportunity.

A major trend shaping the future of the European ETF market is the rise in active ETFs and their inclusion in core portfolios. Currently, active ETFs in Europe constitute less than 3% of total ETF assets, as compared to 8% in the US. A significant pillar driving the growth of active ETFs is the supportive regulatory push given by the different countries for this segment., For instance, Ireland, Luxembourg, and France have implemented measures for the development of active ETFs, including relaxation in portfolio disclosure requirements, removal of subscription tax, and listing of active ETFs.These initiatives will reduce the barriers to entry for both fund managers and investors. This highlights the need for a stronger regulatory push for active ETFS across Europe, as this will lead to more product innovations, attracting wider interest from both institutional and retail investors. The biggest advantage of active ETFs is their ability to generate alpha due to the active management strategies. This approach will allow the fund managers to enhance the portfolio returns while still offering all the unique advantages of an ETF structure.

As the European ETF industry completes twenty-five years, it is poised for tremendous growth in the coming years. This is not just about assets under management and inflows, but also about innovative product structures that span across asset classes and geographies, as well as dynamic asset allocation strategies. As we are at the fag end of the year, the outlook for thematic and actively managed ETFs remains positive, as they do have the potential to enhance long-term returns. However, investors need to navigate the evolving landscape cautiously while designing their core/satellite portfolio strategies.

Profitability recovery amid tariff pressures

Loomis Sayles, an affiliate of Natixis IM

The initial impact of significantly higher tariffs has already been largely reflected in the markets. In the short term, we anticipate that the tariffs will likely moderately hinder economic growth.

Central banks around the world are attentive to the risk of implementing overly restrictive policies, which opens the door to additional rate cuts and a possible economic acceleration toward 2026. Inflation could face upward pressure as price increases from tariffs are passed on to consumers. However, we believe that the Federal Reserve (Fed) will likely overlook these “transitory” price increases that affect only certain imported goods.

There is potential for a significant recovery in global corporate profitability in 2026. U.S. markets, as measured by the S&P 500 index, have shown fundamental leadership based on profitability during 2025. Consensus earnings estimates from a bottom-up approach for emerging markets, Europe, and Japan imply year-on-year growth rates of 10% or more for 2026. Given our procyclical stance, it is encouraging to see global indices firmly in growth mode.

Any equity investments must be viewed through the lens of a weak dollar

Mark Hawtin, Head of the Liontrust Global Equities Team, Liontrust Asset Management PLC

The outlook for the rest of 2025 continues to present plenty of opportunities for differentiated and diversified returns in equity markets. We believe that the path to the best returns will likely continue to lie outside the concentrated M7 trade; they now account for 40% of the S&P market capitalisation and this has proved troublesome for active managers bent on finding better alternatives. The evidence of the first nine months of 2025 suggests this is becoming easier.

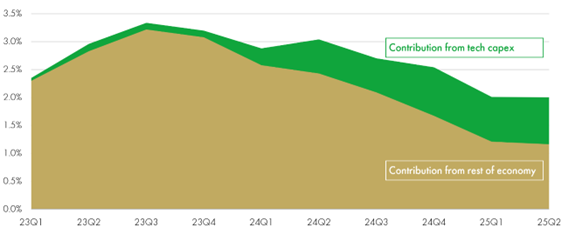

At the same time, risks are building around the world both in terms of the geopolitical and the economic. Much of the US data remain weak, yet headline GDP numbers print at robust levels. The chart from Bridgewater shows one reason for this – the level of capex investment in AI is having a meaningful impact on headline GDP numbers although this has little impact on the low-end consumer.

US real GDP growth contribution from tech capex (%)

This backdrop adds to the need to work carefully on the risk/reward balance of many trades that have worked well for so many years. While, thematically, we remain positive on the potential for AI and for short-term infrastructure investments, we are concerned that we are in the throws of a bubble. The recent trend of vendor financing highlights this risk and, while in the early stages, acts as a warning sign. Trying to predict the impact of this factor and what the outcome will be is tough but experience is a vital asset; it is surely more valuable to have lived through the boom/bust dynamics of a bubble than merely to have read about them. According to Morningstar analytics, only 4% of the 1,700 US large cap equity managers actually managed money through the dotcom era.

The performance outside the US capex trade has been strong, [see table in the first section of the newsletter found here for a further explanation], so we believe there are plenty of opportunities to invest across multiple themes, geographies and sectors to mitigate against individual risks.

Our base case is that equity markets globally will remain little changed in the final quarter of the year but there will be plenty of ways to enhance returns beyond the index level. These include the fact that defence spending remains a key theme in Europe, the catch-up trade in Chinese tech/AI versus the US, Japanese digitalisation and emerging markets equities on the back of a weaker US dollar, which provide the geographical diversification for concentrated US portfolios.

Within the US, we take the view the winners of the next 10 years will not be the same as the last 10 and so companies that use AI effectively across multiple sectors offer interesting opportunities. Within technology, we remain cautious on the longevity of the AI capex cycle and favour selective names that support the trends in AI rather than the titans that build it.

The path of the US dollar is a critical component of many investment themes today and we expect the currency to remain weak on the back of government debt levels and the debt servicing bill that is now close to the 4% of GDP level seen by many as an exit velocity level. Assuming this to be the case, any equity investments must be viewed through the lens of a weak dollar, and this is perhaps the biggest factor in deciding geographical exposures as well as other adjacent ideas like the continued success of investingin stores of value like gold, gold miners and crypto.