MFS IM: Lessons learned during a 100-year trajectory investing

24 JUL, 2024

Author: Carlos Aparicio from MFS Investment Management

Nowadays an investor is exposed to a bombardment of information. There is a lot of noise, which often distracts and rarely proves relevant in the long term. Every quarter more than 55,000 companies listed on the markets present their results worldwide, generating short-term signals that do not necessarily measure the success or failure of a company.

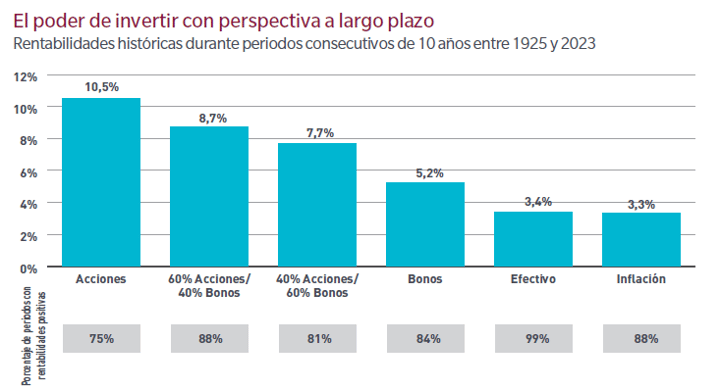

Our experience over the last 100 years has taught us that taking a long-term view allows us to set aside the noise and focus on the information that aligns with our clients' objectives. Since 1924, our philosophy as long-term investors has been an integral part of our investment process, and the strength of our analysis team gives us the conviction and patience necessary to let investment ideas bear fruit over time. History shows that time can be the best ally of investors when it comes to building wealth and generating purchasing power, as seen in the average 10-year returns for different types of portfolios compared to cash and inflation.

In 1924, information about companies was hard to come by. The Securities and Exchange Commission (SEC) did not exist and companies were not even required to publish the most basic information. These information gaps were a problem for investors, so in 1932 MFS created the first internal analysis team to find and analyze information that would help us make better investment decisions, an approach we have maintained ever since.

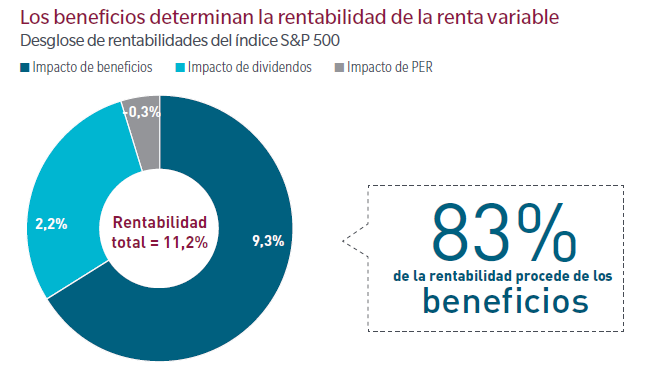

The world has changed, but our focus on fundamentals remains intact. Experience over the last century has taught us that understanding a company's fundamentals is the best way to assess its potential to generate future profits, and analysis has shown that profits are the most important driver of the evolution of equity prices.

Focus on value and not just price

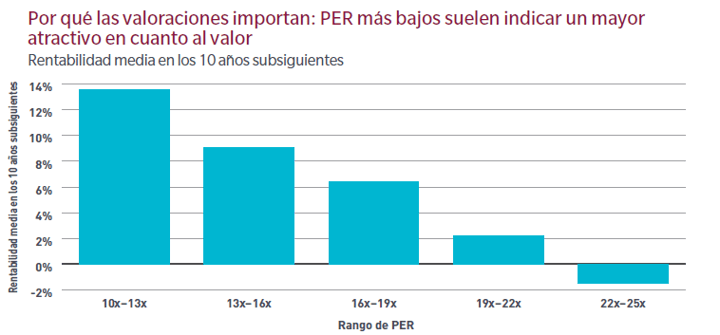

We have learned that applying a disciplined valuation approach is crucial for long-term investment success. As can be seen in the chart below, valuation has historically been a good measure to predict profitability. According to historical evidence, low initial PER multiples have tended to correspond to higher future returns. This is also true in reverse: high initial PER multiples tend to correspond to lower future returns. That being said, sometimes valuations are high for the right reasons, and our fundamental approach helps us determine if a stock is trading at its fair price.

Diversification has paid off

Helping people to invest and diversify. That was the idea that led MFS to create the first open investment fund in the US: the Massachusetts Investors Trust (MIT). At a time when a diversified portfolio was unattainable for most investors, anyone with 250 USD in their pocket could buy a share of MIT, whose portfolio included about 50 companies, including railroads, utilities, automakers, and food producers. Today, diversification is more complex and has many dimensions, including asset classes, sectors, industries, geographic regions, and currencies.

Although diversification does not guarantee profits or protection against losses, diversifying is, in essence, managing risk. We believe that investors can benefit by diversifying sources of return.

Balancing opportunities and risks

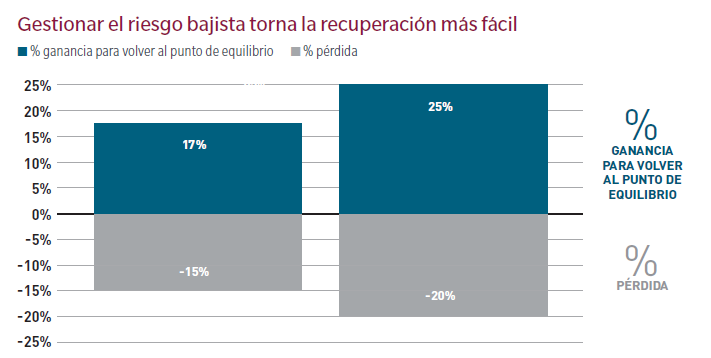

High-quality companies with sustainable profits tend to be less affected during bear market phases than lower-quality companies. Let's look at the following chart. If the stock market suffers a 20% setback, a 25% return is needed to return to the starting point. A portfolio that loses 15% during that same market only needs a 17% return to recover its losses.

We have also learned that often a correction is an opportunity to take advantage of the price retracement. Our investment team can check what has changed during a market correction and identify those companies that could be attractive as long-term buying opportunities.

In short, investors must know how to adapt to changes, but be supported by a process and a philosophy capable of withstanding the test of time.

I know all of this seems like common sense and we are talking about somewhat basic ideas, but most investors tend to invest rationally, until things get complicated, that's why it's good to remember them.

These are lessons learned over a century of investing that have helped us achieve returns, keeping the focus on responsibly allocating capital and with a long-term vision for our clients.