A new era for public debt

1 JUL, 2025

By PIMCO

Peder Beck-Friis, economist at PIMCO, maps out the rise in public debt and its implications for the US dollar and long-term Treasury yields.

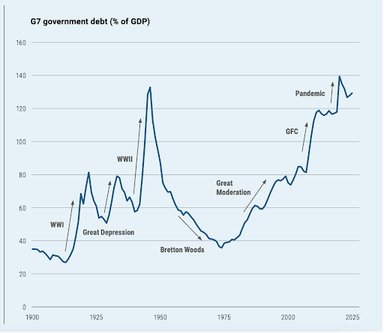

Public debt levels near historical highs

Public debt levels among G7 nations have fluctuated throughout history. They rose significantly during major crises — World War I, the Great Depression, and World War II — and then declined during the post-war boom.

More recently, the global financial crisis and the COVID-19 pandemic have pushed debt ratios to new highs. Today, G7 public debt remains near the peak levels seen at the end of World War II, highlighting the dramatic scale of government borrowing.

High interest rates, compared with the years following the global financial crisis, add to the challenge of servicing elevated debt.

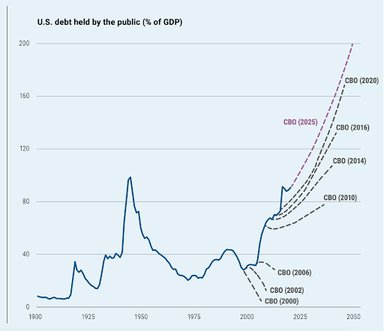

The US debt trajectory is unsustainable under current policy

In particular, the trajectory of US government debt has been on the rise for over a decade. Projections by the US Congressional Budget Office (CBO) show growing debt levels, with each new forecast pointing to a steeper path.

The latest projections suggest that, if no action is taken, US debt could approach 200% of GDP by 2050. Without policy changes, US debt will continue to rise.

The US dollar is likely to remain the dominant reserve currency

Despite the unsustainable debt path, the US dollar is almost certain to retain its status as the world’s dominant reserve currency over the next five years.

Its widespread use in global trade and finance, along with a lack of viable alternatives, supports this position. For example, the dollar accounts for around 88% of global foreign exchange turnover, reflecting its central role in international markets and reinforcing its resilience amid fiscal concerns.

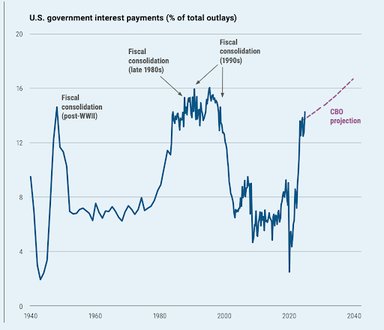

Rising interest payments could lead to US fiscal consolidation

Moreover, US debt may not necessarily spiral out of control.

As debt levels rise, so do government interest payments, which have grown significantly as a share of total federal spending. Historically, this has often triggered fiscal consolidation efforts, as seen after World War II and in the late 1980s and 1990s.

While current debt forecasts are high, these historical episodes indicate that rising interest costs could eventually prompt policymakers to tighten fiscal policy to stabilise the debt dynamic.

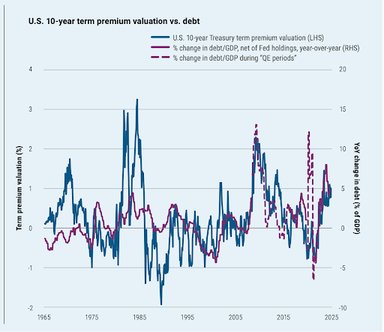

Rising debt (loosely) linked to higher term premium

Against this backdrop, it is worth noting a weak but observable relationship between rising debt-to-GDP ratios(excluding Federal Reserve holdings) and the term premium on 10-year US Treasuries — the extra yield investors demand for holding longer-term bonds.

As public debt increases, the term premium tends to rise, as investors seek greater compensation for holding long-term bonds compared to cash and short-term notes.

For asset managers, this dynamic suggests that rising public debt could lead to a steeper yield curve, affecting the valuation of fixed income assets.