Not all bonds are the same: increasing dispersion across regions and sectors

10 JUL, 2024

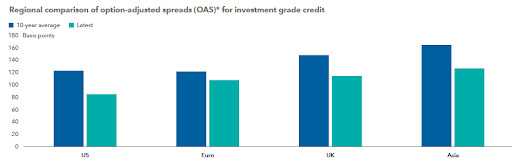

The return of income to bond markets has led to a surge in demand for the asset class. In turn, this has led to a narrowing of investment grade (IG) credit spreads. But this tightening has not happened at the same pace for all bonds, leading to valuation dispersion.

One notable area where this has occurred is between regions. Spreads in Europe and Asia are close to or below historical averages but still off their lows, whereas in the US, they are nearing minimum levels.

We also continue to see dispersion between sectors: credit spreads for financials are wider than industrials, for example. This is unusual, particularly in the US, and we would expect the gap to narrow as conditions normalise.

This ongoing sector and regional dispersion highlights that the opportunity set within investment grade has become increasingly company specific. It requires a dedicated, experienced, bottom-up research capability to help understand where companies offer potential value, while also avoiding companies where spreads could be too tight compared to fundamentals.

Furthermore, by shifting focus from the macro to the company-specific, we believe investors reduce their dependency on one particular economic outcome and can maximise unprecedented opportunities still available within IG credit.