Oil and the Euro have already forgotten the wars

27 JUN, 2025

By LBP AM

Author: Xavier Chapard, strategist at LBP AM

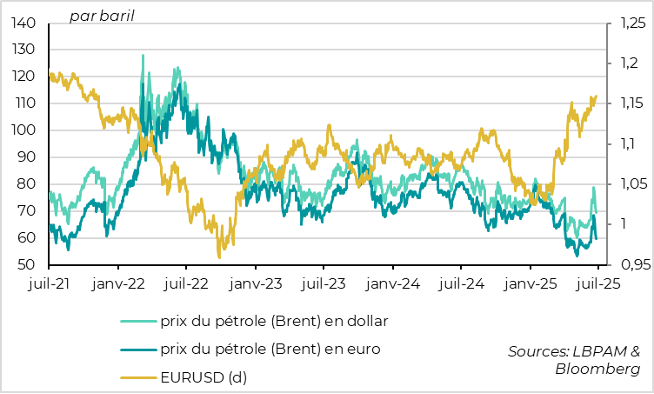

Despite weekend fears following US airstrikes, we have witnessed a rapid and widespread de-escalation of tensions in the Middle East. Iran’s limited response — with no impact on energy facilities — along with US diplomatic pressure, has opened the door to a truce between Israel and Iran. After surpassing $80 per barrel at Monday's opening, oil has already returned to its pre-Israeli-attack level, trading below $70 per barrel. Although some risks remain (such as respect for the ceasefire and the real status of Iranian nuclear facilities), this de-escalation is favourable for the global economy.

The easing of geopolitical concerns and inflationary risks, coupled with surprisingly dovish rhetoric from some Federal Reserve members, have weighed on the US dollar, which has fallen to its lowest level since 2022 against a basket of currencies. After C. Waller's statements over the weekend, a second Fed governor — this time Vice Chair Bowman — hinted at a possible rate cut as early as July. This is surprising, given that less than a week has passed since the latest Fed meeting, where it was made clear that the central bank preferred to wait for summer data before taking action, suggesting stable rates at least until October. However, both officials were appointed by Trump and may already be positioning themselves to succeed Powell at the Fed's helm next spring, meaning they are far from representing the Fed's majority. We continue to believe the Fed will wait until at least Q4 before cutting rates.

In parallel with the dollar's depreciation, the euro is finding support in expectations of increased public spending in Europe, following the formalisation of NATO countries’ military spending target increase from 2% to 3.5%, as well as the presentation of Germany’s new budget yesterday. As a result, the EUR/USD exchange rate surpassed 1.16 units for the first time since the 2022 energy crisis, also helping to reduce oil prices in euros. While the EUR/USD rebound may have been (too?) fast in the short term, its medium-term upside potential remains significant, in our view.

Meanwhile, the first surveys released in June — which were not influenced by the Middle East conflict — show mixed results, still pointing to a limited slowdown in the global economy this summer.

The preliminary PMIs published by S&P Global remain stable around 51.5 points in developed countries, following a partial rebound in May. The manufacturing sector continues to improve slowly, with its PMI slightly above 50, suggesting that price expectations are still supporting industrial activity. In services, the PMI stagnated at a moderate level, indicating that domestic demand is gradually slowing.

Fig. 1. Markets: Oil is trading at pre-Iran conflict levels, and the EUR/USD exchange rate has returned to levels seen before the war in Ukraine.

Fig. 2. Developed economies: PMI remained stable in June after May's rebound.

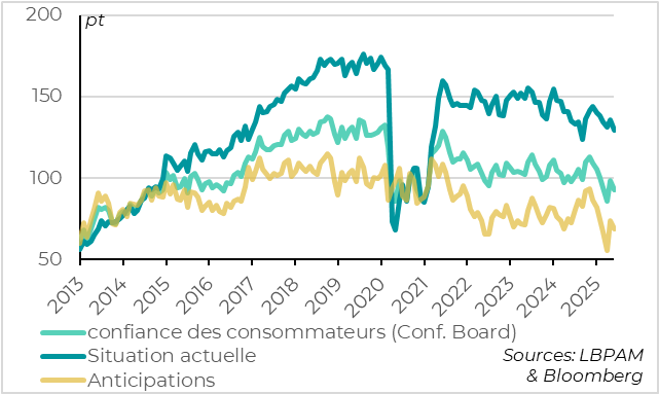

Fig. 3. USA: consumer confidence falls again