Outlook for private equity in 2025: soft landings in dry powder

17 JAN, 2025

By Schroders

Author: Rainer Ender, global director of private equity at Schroders Capital

The recent challenges facing the private equity market could be overcome as rate cuts and lower inflation pave the way for an improvement in multiples.

Although there was a notable slowdown in deal-making in 2024, signs of recovery are emerging that suggest the private equity market could be more dynamic in 2025.

2024 presented multiple challenges

As in 2023, this year has witnessed wide spreads between bid and ask prices and reduced liquidity. When rates rise, the costs of financing acquisitions also increase, which lowers the EV/EBITDA. Buyers pay more to get fewer loans, which reduces the amount they want and can offer for assets.

Similarly, the rise in rates has put downward pressure on cash flows, while inflation increases costs for companies that lack adequate transmission. Sellers, on the other hand, have tried to make asset exits when leverage was cheap and multiples were increasing. This dynamic has created a mismatch between the price buyers are willing to offer and the price sellers are willing to accept.

Outlook for private equity: Reasons for optimism in 2025

Even amid these challenges, several developments suggest that the new year may bring more favorable conditions:

- Deal value is increasing. Although the EV/EBITDA multiples of large acquisitions have decreased, the overall value of deals is increasing, a trend driven by a preference for larger investments in established companies.

- Exit prices in the global market have stabilized, and there has been a recent uptick in "sponsor-to-sponsor" exits (a PE fund sells to another PE fund). However, a notable valuation gap persists, as acquisitions of small and medium-sized companies trade at a significant discount compared to their larger counterparts, a trend that suggests a difference in perceived value in the market.

We believe that many of the factors that exert downward pressure on multiples will dissipate, and the lowering of interest rates and lower inflation should lay the groundwork for an improvement in multiples.

We also believe that investors could benefit if they "follow the money" and take into account the secondary operations led by GP (general partners). Almost half of the record volume of secondary operations in the first half of the year corresponded to these vehicles, also known as continuity funds. These align the financial incentives of the GP and the limited partners (LP) and, therefore, create potential benefits for all stakeholders: the original sponsor, new and existing investors, and the company or companies in the new fund structure.

Favorable conditions for the small and medium-sized business market

We believe that conditions will also favor concentration in small and medium capitalization markets, which are diversifying. Recent history has shown their potential to achieve good results in periods of volatility, and the law of large numbers (probability theory) makes it inherently easier to generate more significant multiples in smaller companies.

Operating in small and medium markets also reduces dependence on the still stagnant IPO (initial public offerings) market for exits. In addition, after the success of efforts to help a small or medium company become a large capitalization one, exits can be made larger in the market, where there is a considerable amount of dry powder, that is, money already raised looking for opportunities.

A bulwark against volatility

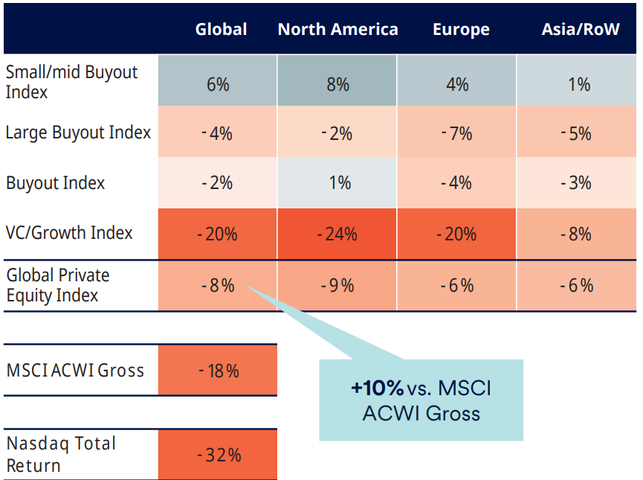

If we combine the recent period of volatility with the dotcom crash, the global financial crisis, the eurozone crisis, and the COVID-19 pandemic, we see that the Global Private Equity Index outperformed the MSCI ACWI Gross Index by an average of 8%.

What were the reasons for this?

- At a structural level, the nature of the committed capital allows companies to retain ownership of assets in times of crisis and sell them when market conditions are favorable, thus avoiding the type of "flash sales" at low valuations. In addition, the generally more rigid nature of private equity also prevents people from falling into the psychological traps of investing, such as panic selling at the least opportune moment.

- From a fundamentals perspective, private equity firms tend to present a different combination of sectors compared to listed markets, focusing on less cyclical industries such as healthcare and technology, while maintaining less exposure to banks and heavy industry. In addition, private equity tends to prefer growth and disruption, seeking companies with high expansion potential. They also prefer business models with recurring revenues that generate cash, as they tend to be less volatile.

Profitability during the inflation return period