Possible stagflation will shape the course of central banks

10 APR, 2026

By Thomas Hempell from Generali Investments

By Thomas Hempell, Head of Macro & Market Research, Generali Investments

The global economy, although it has so far proven resilient, is facing a stagflationary shock driven by rising energy prices linked to the war in Iran. High uncertainty and risks of supply chain disruptions are weighing on activity. Europe and Japan/Asia are particularly exposed due to their heavy dependence on energy imports. Therefore, the duration and severity of disruptions in energy supply are crucial for the global outlook.

In our base scenario, the war ends and oil and gas supply gradually recovers. Energy prices would fall from current levels but would still end the year well above the roughly $60 per barrel priced into futures at the beginning of the year. The increase in energy prices—and, with some delay, food prices—will temporarily push inflation sharply higher. In the euro area, inflation had just fallen below the ECB’s 2% target before the war. The crisis should ease—but not derail—global growth: the euro area’s recovery will be delayed, but not completely halted. The United States, as a net energy exporter, is less exposed, although confidence there will be affected.

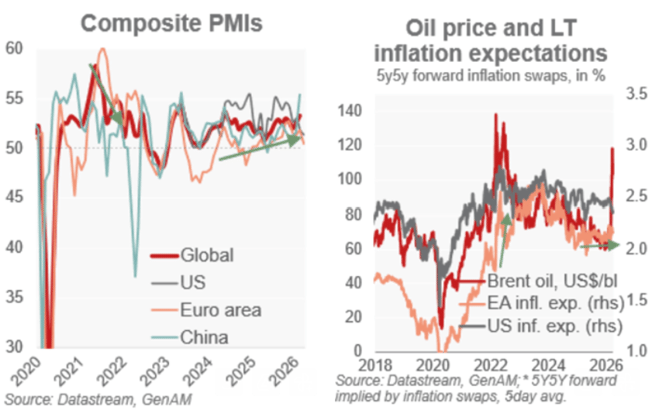

Central banks are likely to look through the temporary spike in inflation. The threshold for aggressive monetary tightening is much higher than in 2022, reflecting key differences: the global economy is growing solidly, energy price increases are so far more moderate (especially for gas), and the risk of second-round effects is lower, given better-anchored inflation expectations and less accommodative policies (see charts on the left). The Fed could still implement one final 25 basis point cut by late summer. The ECB may keep rates unchanged on fundamental grounds, but is nevertheless more likely to deliver a “precautionary” 25 basis point hike to avoid appearing complacent.

Risks are clearly tilted to the downside. A prolonged conflict lasting two to three months, with a sustained closure of the Strait of Hormuz and lasting damage to regional energy infrastructure, would likely trigger a mild recession in the euro area. Stronger second-round effects and unanchored inflation expectations would force the ECB into aggressive tightening, while the Fed would likely also respond, albeit more cautiously.