Between climate, infrastructure and yield: Project Bonds are reshaping bond investment

12 MAY, 2025

Author: Emma Otmani, CFA – Junior Portfolio Manager chez IVO Capital Partners

When a new airport opens, a solar park begins producing energy, or a highway network expands to connect a region, these developments don’t happen spontaneously. Behind every essential infrastructure project lies a significant financing challenge. Governments, often limited by budgetary constraints, cannot fund these initiatives on their own. This is where project bonds come in—offering a financing solution that allows investors to actively support the development of strategic assets while benefiting from attractive returns.

Project Bonds: an investment tool anchored in economic reality

Project bonds are specialised debt instruments issued to directly finance strategic infrastructure projects such as ports, airports, renewable energy projects (solar, wind, hydroelectric), and energy projects like FPSOs ("Floating Production Storage and Offloading").

What are the benefits of Project Bonds for nvestors?

1. Tangible and strategic assets

In a world marked by persistent uncertainty, owning physical and strategic assets provides a resilient investment approach. The infrastructure financed by project bonds—such as ports, airports, renewable energy facilities, and transport networks—is essential to the economic development of emerging markets. These investments improve connectivity, enhance access to vital resources, create local employment opportunities, and strengthen the energy and industrial sovereignty of their regions.

Project bonds benefit from a robust security framework, often supported by multiple guarantees that reduce credit risk and bolster investor confidence. These instruments are typically secured by the underlying assets they finance, offering tangible collateral in the event of default (“senior secured notes”).

Moreover, such projects frequently receive backing from major international financial institutions, including the World Bank and the European Bank for Reconstruction and Development (EBRD), which reinforces their long-term viability and economic stability. Project bonds also align investor interests with those of local stakeholders, ensuring both sustainable development and disciplined infrastructure management.

2. Clearly defined financing, predictable cash flows, and aligned amortization

Projects are typically defined and secured through long-term contracts—such as airport concessions or power purchase agreements (PPAs)—that establish terms with offtakers. Unlike corporate bonds, which may finance a wide range of objectives (e.g., capex, acquisitions, or dividends), a project bond is dedicated to financing a specific project. This results in greater transparency and tighter control over financial flows.

Instead of a bullet repayment at maturity, project bonds are often structured as amortizing or sinkable instruments, with gradual principal repayments scheduled over the life of the bond. These repayments are aligned with the project's expected cash flow generation, significantly reducing refinancing risk at maturity.

The financing structure typically includes reserve accounts to ensure sufficient cash is available to service the debt. Project sponsors are also financially committed to the venture, providing strong incentives to maintain the project's economic viability. Finally, strict financial covenants outlined in the offering memorandum impose limits on additional debt and reinforce sound financial management, protecting the overall stability of the issuer.

3. Diversification advantage and attractive yields for a secured profile

Project bonds offer exposure to sectors that are often underrepresented in traditional developed market high-yield bond allocations. These instruments are frequently rated investment grade or financed by infrastructure funds through private debt structures. In emerging markets, however, project bond ratings are often constrained by the sovereign ceiling, meaning issuers are affected by their geographic location regardless of their individual credit quality.

In addition, project bonds tend to offer an attractive yield premium, partly due to the "new issue premium." Since many of these issuers are newcomers to the bond market, they must offer higher yields to attract investors, creating an additional income opportunity.

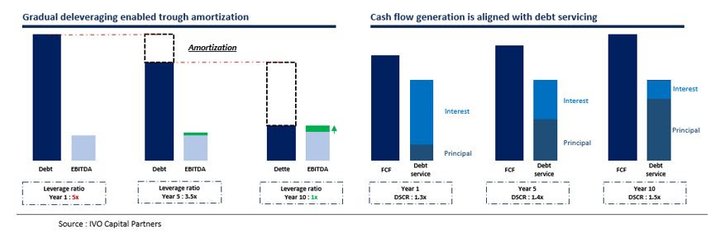

At first glance, project bonds may appear highly leveraged, which can raise concerns among some investors. However, a closer analysis reveals a built-in deleveraging mechanism. While initial leverage is high—reflecting the immediate injection of capital into the project—the structure ensures rapid debt amortization. The cash flows generated by the project are directly allocated to debt service, enabling consistent repayment over time. This alignment between cash flow generation and debt reduction results in a more controlled risk profile than initial metrics might suggest, while still delivering attractive returns.

What are the risks of Project Bonds for investors?

Project bonds are typically backed by concession contracts or power purchase agreements (PPAs) involving public or semi-public entities. However, these arrangements carry certain risks. Regulatory changes, amendments to concession terms, or a refusal by the off-taker to fulfill contractual obligations can undermine the economic viability of the project and impair the issuer’s ability to service its debt. This risk is especially pronounced in jurisdictions with unstable legal and regulatory environments. To mitigate it, investors must carefully evaluate the robustness of the contractual framework, the quality and enforceability of guarantees, and the track record of public-sector counterparties.

In addition to regulatory and contractual uncertainties, project bonds are exposed to risks inherent in each phase of the project lifecycle. From design and construction to operation, each stage presents distinct challenges. The construction phase is generally the most hazardous, as unforeseen delays or cost overruns can significantly impact the project’s financial viability, with recovery dependent on future cash flows once operations commence. As such, it is critical to assess the financial strength of the project sponsor and the technical expertise of the operator to ensure they have the capacity to successfully deliver the project.

Project Bonds: a lever for sustainable financing?

Emerging markets account for 85% of the world’s population and approximately 75% of global greenhouse gas emissions. Financing green infrastructure—such as wind farms and solar power plants—through project bonds not only supports local development but also helps enforce rigorous governance standards. By incorporating Environmental, Social, and Governance (ESG) criteria, project bonds offer investors a way to pursue responsible investment strategies.

These instruments are particularly well-aligned with several of the United Nations’ Sustainable Development Goals (SDGs):

- SDG 7: “Ensure access to affordable, reliable, sustainable and modern energy for all.” Project bonds reduce reliance on fossil fuels and promote clean power.

- SDG 9: “Build resilient infrastructure...” They support essential infrastructure in underserved regions.

- SDG 11: “Make cities...resilient and sustainable.” Improve urban living standards.

- SDG 13: “Take urgent action to combat climate change...” Contribute directly to the global energy transition.

Moreover, these bonds often include robust ESG reporting requirements, ensuring transparent allocation of funds and alignment with sustainability objectives.

Example of Project Bonds for energy transition: The rise of renewable energy in India

India exemplifies the dynamic energy transition taking place in many emerging economies. By the end of 2024, the country had reached approximately 203 GW of installed renewable energy capacity, with an ambitious target of 500 GW by 2030. This rapid growth reflects both strong political commitment and increasing interest from international investors. It also highlights a substantial need for green infrastructure—including solar farms, wind farms, and energy storage solutions—which can be effectively financed through project bonds.

Companies such as Continuum Energy, Greenko, and Sael are at the forefront of this movement. These Indian firms develop and operate large-scale renewable energy projects, often supported by long-term power purchase agreements (PPAs), making them well-suited for structured bond financing. Project bonds in this context offer a dual benefit: delivering financial returns while advancing environmental goals.

By channeling capital into sustainable infrastructure, these instruments directly contribute to the achievement of key United Nations Sustainable Development Goals—namely, access to clean energy (SDG 7), sustainable industrialization (SDG 9), and climate action (SDG 13).