Reasons to keep a cool head in the face of geopolitical panic

11 JUL, 2024

Author: Stanislas de Bailliencourt, Head of Fixed Income and Asset Allocation, Sycomore am (part of Generali Investments ecosystem).

Taken by surprise by Macron’s decision to dissolve the French Parliament and by the ensuing party alliances, European financial markets have been left heaving since June10th. The worst hit by this wave of panic were cyclical sectors and financial stocks. Nevertheless, in this highly uncertain environment, it is important for investors to keep a cool head.

Volatility –to which we had become unaccustomed-has made a major comeback over the past few days; these episodes are not unusual and can peak at much higher levels than those observed today.

The VIX index, also known as the “fear gauge”, indicates that volatility remains contained for the time being. Admittedly, the peak may not have been reached. Far from causing us to panic, we feel this return of volatility could offer attractive entry points for investors.

Several observations should prevent investors from panicking at this stage. First, at European level, the outgoing coalition in Parliament, made up of three pro-European groups (EPP, social democrats and liberals), has held onto its absolute majority and is likely to win the key seats in the European commission.

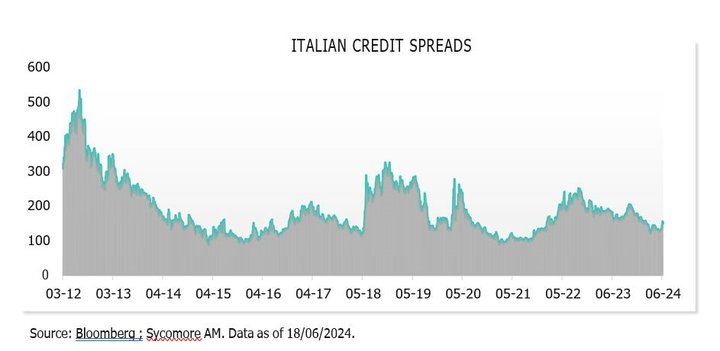

Second, looking back, Italy was in a similar situation to the one France may be in after the elections on July 7th. Giorgia Meloni, ruler of populist party Fratelli d’Italia, took over as Prime Minister in October 2022.

On economic matters, she has led a centre-right policy rather consistent with her predecessor, Mario Draghi. The country currently benefits from the large funding plans backed by the European Union.

Contrary to all expectations and as shown in the graph below, Italian credit spreads only widened moderately, while financial stocks listed on the Milan stock exchange have generally outperformed since the election of Giorgia Meloni.

In France, current and future public expenditure (infrastructure, defence, etc.) leaves the next government with very little room for manoeuvre.

Indeed, on Wednesday June 19th, the European commission announced that it had launched an Excessive Deficit Procedure against seven EU country members, including France. To avoid a fine, these countries will have to lower their deficits from 14 to 20 billion euros every year.

Financial markets can also be very good at exerting fast pressure on a government. Liz Truss, UK Prime Minister for just a few weeks, suffered the consequences in 2022.

Her ‘flash in the pan’ premiership came to an end when she was forced to step down after presenting a controversial budget considered to be ‘unfunded’.

We believe widening spreads offer an entry point - reminiscent of the Italian experience in 2018 or 2022, when far-right parties won the elections.

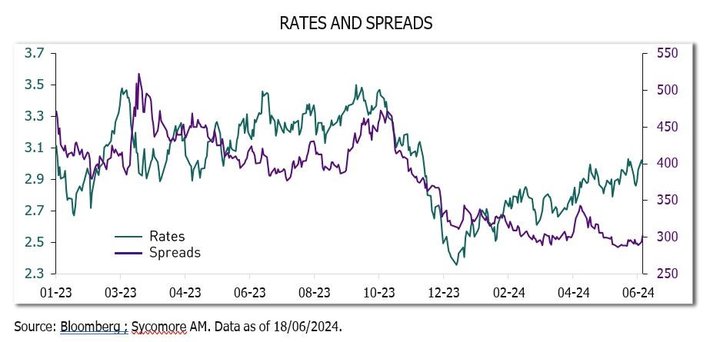

The France-Germany 10-year bond spread, an excellent risk indicator, remains rather modest and principally driven by a ‘flight to quality’ causing German bonds to retreat, rather than by a massive French bond sell-off. Interest rates, on the other hand, have risen sharply year-to-date, offering attractive yields.