Rising debt worsens sovereign risks

10 JUL, 2024

Author: Dennis Shen, analyst at Scope Ratings.

Rising debt-to-GDP ratios combined with higher long-term interest rates

Rising long-term interest rates increase the risks to sovereign debt sustainability, especially as institutional and financial market controls on excessive borrowing in rich countries are weaker than they were several years ago. The debt-to-GDP ratios of most G7 countries are likely to continue to rise. The fiscal rules of many of their governments - further weakened during the pandemic crisis - are insufficient to curb rising indebtedness, while current higher interest conditions would complicate fiscal consolidation.

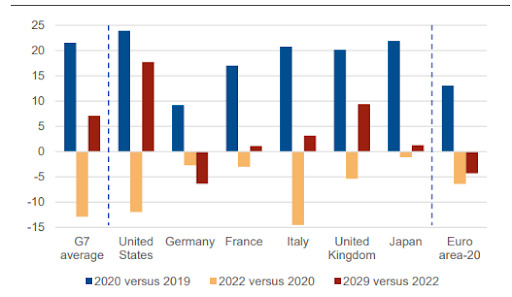

The elections in several G7 countries - France (AA rating and negative outlook), the UK (AA/stable) and the US (AA/negative) - are unlikely to result in a post-election reversal of their debt trajectories. We expect G7 general government debt to rise to 135.2% of GDP in 2029, approaching the recent 2020 peak of 139.6% (Chart 1). This increase is mainly due to the rise in US debt, the world's benchmark "risk-free" borrower.

Chart 1: G7 debt ratios declined in 2020-22, but have risen since then

Changes in general government debt ratios, pps of GDP

The US debt-to-GDP ratio will rise regardless of the outcome of the 2024 election

As the world's safest asset issuer, the US has less incentive to cut its debt despite warnings from rating agencies and fiscal watchdogs about long-term fiscal risks. Regardless of the outcome of the upcoming presidential and congressional elections, whether Donald Trump or Joseph Biden wins later this year, we expect US debt to continue to rise. The debt ceiling remains the only element within the US fiscal framework with real teeth to enforce budgetary rectitude. Unfortunately, however, it also introduces a risk of technical default every year or two.

If, at this point, an imminent threat of default is needed to force comparatively moderate cuts in the Fiscal Responsibility Act of 2023, it underscores the pressures that may be necessary to ensure a stable debt trajectory. As for our AA rating on the US, the combination of long-term debt ceiling risk, high political fragmentation and sustained high fiscal deficits are the main negative rating drivers, something we have emphasised for our negative outlook. US general government debt is projected to rise to 137.8% of GDP in 2029, surpassing the 2020 peak of 132%.

French and Italian debt on upward trajectories

Within the euro area, France is the source of heightened concerns of a deeper regional fiscal crisis after President Emmanuel Macron called early parliamentary elections. A parliament with greater representation from both far-right and far-left groups is likely to force Macron to accept a prime minister from an opposition party, creating additional political uncertainty.

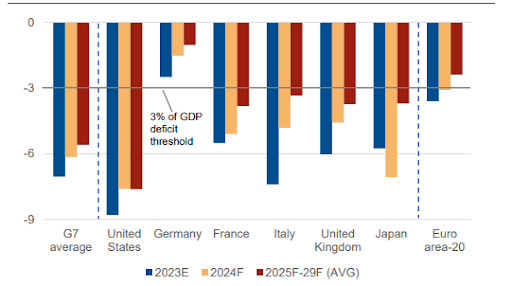

We expect deficits above 3% of GDP until 2029 (Graph 2) - even before any political changes after the elections that could hamper the planned budget consolidation. Rising French debt - which will gradually increase to 113% of GDP in 2029 from 110.6% at the end of last year - could cause further investor unease.

To avoid this, the new French government must cooperate with its country and EU neighbours and carry out consistent fiscal consolidation. The widening of the spread of 10-year OAT sovereign bonds against German bunds above 25 basis points since Macron called early elections after the European elections in early June is material. The spread could easily widen further if the sustainability of French debt is questioned.

Graph 2: G7 budget deficits to remain high, except for Germany

General government balance as a % of GDP

The chances of the French situation spilling over to the euro area are modest for the time being; Italy, however, is in the spotlight.

The infection from the situation in France to other euro area sovereign markets has so far been moderate. The lowest-rated EU member states, Italy (BBB+/stable) and Greece (BBB-/stable), have seen 10-year spreads widen by 10-20 basis points since the European elections.

Still, Italian debt is projected to increase slightly to 143.6% of GDP in 2029, from 137.3% at the end of 2023. We expect that Italy will not reach a budget deficit of 3% of GDP compatible with the Maastricht limits until 2028.

The European Commission last month recommended an excessive deficit procedure for France and Italy, among other countries. While this does not eliminate access to the TTIP, it does raise the eligibility hurdles. As a result, the ECB could rely more on communication and the flexibility of the emergency pandemic purchase programme (PEPP) as the first lines of defence of the euro area's financial stability.

The lack of an independent monetary policy means that euro area borrowers remain more vulnerable to massive bond market sell-offs than countries outside the monetary union, such as the United States. Although policy innovations introduced in the Eurosystem since the euro crisis and the pandemic, such as the PEPP, have partly improved the ability of monetary union policymakers to deal with asymmetric shocks, the greater susceptibility of euro area borrowers to market risks does not spare them from market risks.

However, the greater susceptibility of the euro area to changes in investor sentiment is likely to reduce the moral hazard arising from expectations that a G7 country can necessarily rely on the support of the monetary authority in the event of financial turmoil. The UK's mini-budget crisis was quickly resolved following the Bank of England's intervention. The tighter financial markets for euro area countries may partly explain the comparatively more benign public debt projections, with the average ratio falling to 87% of GDP in 2028 from 88.7% in 2023. This includes a deficit forecast of slightly below 3% of GDP at the euro area level by 2025.

UK: rising debt risk to sovereign rating

The UK, rated AA with a Stable rating outlook, is in a similar situation to the US, facing a significant increase in general government debt to 110% of GDP in 2029 from 101% in 2023. Memories of the mini-budget crisis two years earlier are unlikely to be enough on their own to ensure a tight fiscal policy after the parliamentary elections.

The Labour Party, the general election winner, has ruled out raising income tax, corporation tax or social security contributions. This limits the party's budgetary room for manoeuvre to stabilise the debt trajectory, short of relying on very high inflation and/or unrealistic growth expectations. Public spending in the coming years is likely to be significant. Without government policies to curb borrowing, this debt trajectory could put further long-term pressure on the state's credit rating.

Japan outlook upgraded

Meanwhile, we have recently revised our outlook for another G7 country: Japan (rating A) to Stable from Negative, as more durable inflation, breaking a very long history of deflation, supports the outlook for government debt.

Debt-to-GDP has declined from the highs reached after the Covid crisis.

Indeed, the average debt-to-GDP ratio of the G7 countries has declined from its pandemic peaks. Globally, general government debt ratios have declined from 2020 to the present. This includes the euro area as a whole, which fell from 97% of GDP at the 2020 peaks to 89% at the end of last year. The US deleveraged from 132% to 122% over the same period, as did the UK from 106% to 101%, while Italy's debt corrected sharply from 155% to 137%. Japan's debt also fell to 252% in 2023 from 258% in 2020. This was due to an unusually strong post-pandemic recovery as economies reopened and a subsequent phase of high inflation.

This earlier correction of the debt-to-GDP ratio provides governments with some additional fiscal space to absorb increases. Most G7 governments can, theoretically, sustain much higher public debt ratios than other states because of their significant debt tolerance.

However, the change in the outlook for rates to stay higher for longer is a game changer. The increase in debt-to-GDP raises questions about long-term debt sustainability and limits governments' budgetary room in the short term. Before the pandemic crisis, the prevalence of ultra-low rates ensured that interest payments fell even as governments increased their borrowing. Today, the proportion of government spending servicing public debt increases as older, low-cost debt is refinanced at higher rates, even without changing the volume of borrowing.

G7 economies with growing public debt - such as France, Italy, the United Kingdom and the United States - must find ways to strengthen their fiscal frameworks and achieve adequate fiscal consolidation, even given their institutional advantages. Each faces more onerous spending on defence, digitalisation, the environment and social welfare, creating inevitable pressures on balance sheets.

Germany is an outlier: is fiscal discipline undermining long-term growth?

By contrast, among the G7 countries set to cut their public debt ratios is Germany (AAA/Stable Outlook), where historical fiscal prudence is maintained with balanced budget rules and debt restraint. Unlike most other G7 governments, Germany has set fiscal deficits below 2% of GDP this year and in the coming years. This fiscal discipline gives the government room to further reduce debt, even as the role of inflation in supporting recent debt declines diminishes.

However, Germany faces the challenge of needing significant investment to modernise public infrastructure and adapt its industrial base to challenges, from the shift towards greater reliance on renewables and non-Russian natural gas supplies to rising protectionism hampering export growth. A stronger German economy would in turn help boost growth in neighbouring economies and support the sustainability of its higher debt ratios.