The shifting trade landscape of Emerging Markets

2 JUL, 2025

Emerging Market (“EM”) countries have undergone a dramatic transformation in trade patterns since the early 2000s. The United States and other developed economies, once the dominant trading partners of these countries, have seen their relative importance decline over the past two decades. In their place, other emerging markets, particularly China, have become increasingly significant trading partners.

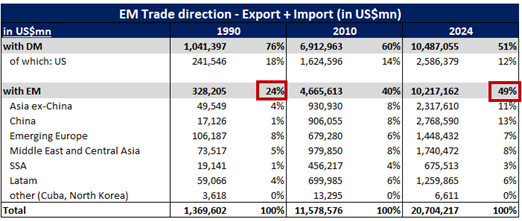

One of the most significant developments has been China’s rise as the leading trade partner for many EM economies, overtaking the United States. Concurrently, trade among EM countries, commonly referred to as South-South trade, has expanded rapidly. Intra-EM trade now accounts for nearly half of total EM trade, up from just 24% in 1990, highlighting the growing economic interconnectivity within the Global South.

In recent years, the United States has reignited a wave of protectionist trade policies, expanding tariffs not only on Chinese goods but also on imports from a broad range of global partners, including key allies. Ostensibly on grounds of national security, reshoring, and industrial policy, this new round of tariffs is once again reshaping global trade flows. However, decades of trade diversification have made emerging markets less vulnerable to U.S. economic cycles and policy shifts. The U.S. share of EM trade has declined from 18–22% in the 1990s and early 2000s to just 12% today, signalling greater resilience amid evolving global dynamics.

Figure 1: Emerging Markets trade direction

China's Ascendancy in Emerging Markets trade

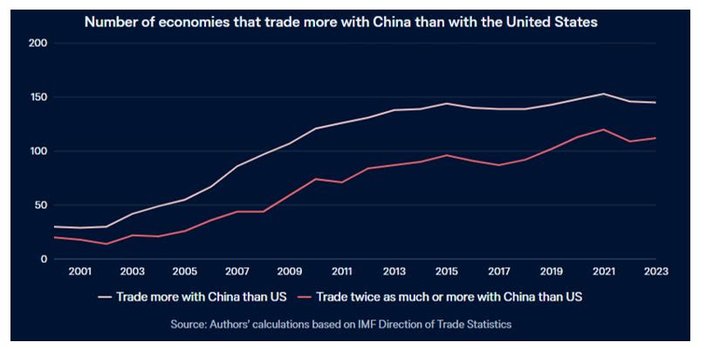

Figure 2: Number of countries that trade more with China than with the US

In 2000, the United States was the largest trade partner for over 80% of emerging market economies. By 2023, this had flipped—China had become the top trading partner for more than 65% of EM countries.

This shift was driven largely by China’s

- Rapid economic expansion, which boosted demand for global commodities.

- Accession to WTO.

- Strategic intent to expand its influence in Ems is exemplified by initiatives such as the Belt and Road Initiative (“BRI”), which has significantly deepened China’s trade and infrastructure ties with many EM economies.

For example, Brazil’s exports to China reached $104.3 billion in 2023, driven primarily by soybeans, iron ore, and oil. Similarly, Indonesia shipped $64.9 billion worth of goods to China in 2023, largely consisting of iron and steel, mineral fuels, and nickel. This deepening trade relationship with China has reduced emerging markets' reliance on the U.S. for exports and capital goods, thereby lowering their exposure to U.S. economic cycles. At the same time, it opens up greater long-term opportunities, given China’s large and still-growing economy, much of it increasingly consumer-driven, and its vast consumer base, which presents valuable prospects for EM exporters.

As part of the Belt and Road Initiatives, China has significantly strengthened its economic and political ties with many EM countries. Since the BRI’s launch in 2013, China's trade with BRI countries has more than doubled by 2023, exceeding $2.1 trillion in 2023 alone. This growth has been particularly strong in sectors such as machinery, electronics, textiles, and raw materials.

The Rise of South-South (Intra-EM) Trade

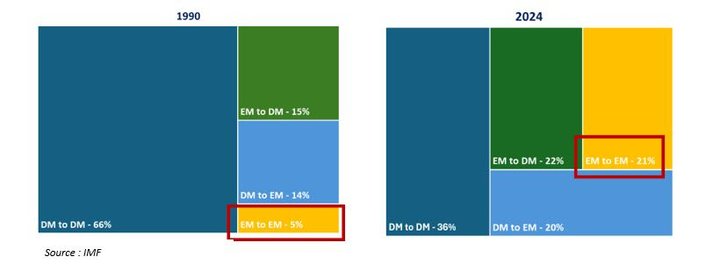

Another defining trend is the surge in trade between EM countries, also known as the Global South, themselves. South-South trade has grown from about 5% of total global trade in 1990 to 21% in 2024, signalling deepening economic ties within the Global South.

Figure 3: Distribution of Global Trade

A substantial portion of South-South trade involves China, which has grown 162-fold between 1990 and 2024 and now accounts for 13% of total EM trade. Still, trade among EMs excluding China has also expanded significantly—rising 31-fold over the same period, compared to a 10-fold increase in trade with developed markets. As illustrated in the Figure 1, intra-EM trade (excluding China) now represents 38% of emerging markets' total trade, highlighting the growing importance of broader South-South economic linkages.

Key Drivers:

Regional Trade Agreements (RTAs) have facilitated increased intra-EM trade; countries trading within their own region generally face lower tariffs due to RTAs.

- Several RTAs have been established in the past 5 to 10 years across regions, such as Africa Continental Free Trade Area (AfCFTA) in Africa, USMCA in North America, Eurasian Economic Union (EAEU) agreement in Eurasia for post-Soviet states, RCEP in Asia and CPTPP in Trans-Pacific region. This comes in addition to other longer-established regional blocs, such as ASEAN and MERCOSUR.

- Trade within RTAs is generally expected to be more resilient relative to trade with other countries. One reason is that such agreements provide mechanisms that can contribute to economic stability, recovery, and resilience.

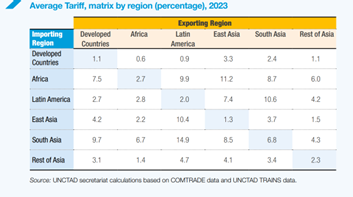

- The U.S. withdrawal from key multilateral trade agreements, such as the RCEP and the CPTPP, particularly during the first Trump administration, created space for emerging markets to take the lead in developing alternative trade frameworks and redirect trade flows. Prior to the U.S. tariff hikes imposed on Liberation Day, trade between emerging market regions often faced relatively higher tariffs, limiting competitiveness. For instance, exports from Latin America to South Asia face average tariffs of 14.9%. However, with the recent rise in U.S. import tariffs, EM countries may increasingly redirect trade toward other EM regions, fostering greater South-South integration.

U.S. tariffs on China, especially during the 2018–2019 trade war, prompted many companies to shift production to other emerging markets such as Vietnam, India, Indonesia, and Mexico. This redistribution of manufacturing has increased trade in intermediate goods among EMs and positioned several non-China emerging economies to benefit from the next wave of global supply chain realignments.

Conclusion: A Redrawn Trade Map

Emerging Market countries are no longer merely responding to the actions of advanced economies. Instead, they are:

- Increasing trade with each other.

- Deepening strategic partnerships with China.

- Gradually decoupling from U.S.-led trade dynamics.

Looking ahead, over the next 10–20 years, this evolving trade architecture has the potential to enhance EM resilience through diversified partnerships, shift the global balance of economic power, and support greater autonomy in EM policymaking and development strategies.

The sustained momentum in intra-EM trade and the diversification of trade flows represent a positive structural shift for investors. As this trend continues to unfold, both investors and policymakers will need to reassess long-held assumptions about global trade, acknowledging that the Global South is increasingly positioned to shape its own economic future.