Shifting trends favor European Banks vs. US Banks for the first time in years

7 OCT, 2023

By Greg Schantz, CFA, Senior Credit Research Analyst, and Julian Wellesley, CFA, Senior Credit Research Analyst at Loomis Sayles.

For the first time since before the global financial crisis, European banks appear to be in a stronger position than US banks. Moody’s Ratings recently downgraded several regional US banks, citing funding cost pressures, capital weakness, and a deteriorating outlook for credit quality, including commercial real estate (CRE). We have long shared the same concerns about smaller US banks, and in our view, the downgrade adds to the contrast between US banks and their overseas counterparts. From the shifting regulatory landscape to liquidity, we see several key differences that contribute to our more favorable outlook for European banks relative to US banks.

The regulatory landscape

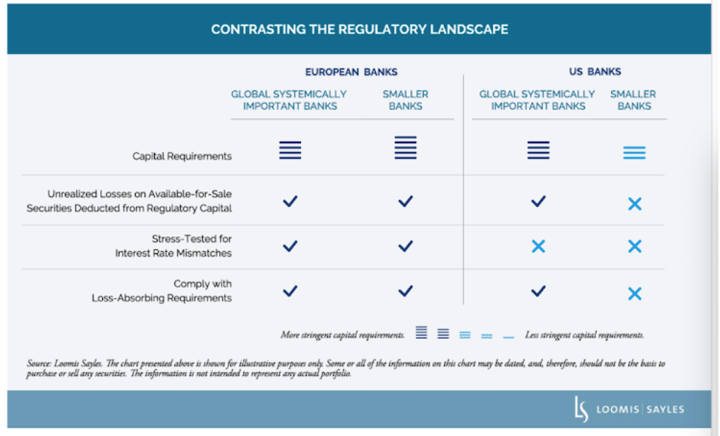

The US takes a substantially different approach to regulation compared to most global banking systems, particularly when it comes to smaller banks. The table below highlights a few key differences in the regulatory landscape for US and European banks.

Capitalization

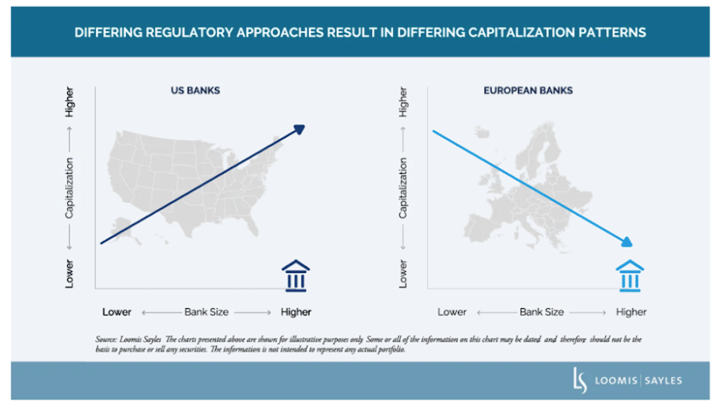

We believe capitalization favors European banks, particularly among smaller banks. US and European systemically important banks (GSIBs) have similar capital ratios (the percentage of a bank's capital to its risk-weighted assets) due to similar regulatory frameworks. For smaller domestic-only banks, capital ratios are significantly lower in the US than elsewhere around the globe.

Unrealized losses on securities eroding economic capital is a major concern for some US banks because they built up deposits during the pandemic and invested much of them in securities that have since fallen in value. The risk of unrealized losses is less material outside the US. European banks saw a similar increase in deposits, but many chose to increase cash positions instead of investing in securities. The difference in regulatory treatment of unrealized losses by small banks strongly favors European banks in our opinion, though the US has proposed new regulations following a number of bank failures.

Liquidity

Liquidity strongly favors European banks over US banks, in our view. European GSIBS have substantially higher liquidity coverage ratios (LCR), the proportion of a bank’s highly liquid assets relative to its short-term obligations, than US GSIBs.

US banks actually overstate liquidity coverage ratios in our view, since they include held-to-maturity Treasury and agency securities in high-quality liquid assets that, if sold, would force that bank to realize all unrealized losses in its held-to-maturity securities portfolio. In addition, some US banks are seeing a substantial outflow of deposits as depositors move from smaller banks to larger banks or out of the banking system altogether. Outside the US, most banks are experiencing little to no decline in deposits. We believe European banks will likely see some deterioration in their LCRs as government-provided funding (e.g. TLTRO[i]) is repaid, but we expect the impact to be modest and well planned for.

Asset quality

We think asset quality trends also favor European banks. Criticized loans[ii] at US banks have increased in each of the past two quarters, while similarly classified loans for European banks (known as stage 2 loans) have modestly increased in some jurisdictions but declined in others. CRE is a major focus for many investors at the moment, and US banks generally have significantly more exposure to the asset class than European banks. Among US banks, GSIBs have low exposure averaging about 9% of total lending, while smaller regional banks have substantial exposure approaching 30% of total lending. The majority of large European banks have diversified lending profiles of which CRE typically accounts for less than 10%.

On the other hand, European banks have far more exposure to residential mortgages, a potential area of concern given short-term fixed durations that are resetting at substantially higher rates in places like the UK, Sweden, and Norway. US banks are less exposed to residential mortgages due to the longer-term fixed nature of the market and their ability to sell mortgages to government agencies. Despite the concerns around higher rates, residential mortgages are full recourse outside of the US, meaning the lender can seize other assets from the borrower to repay the debt and have typically held up well in all but the most severe housing bubbles.

Profitability

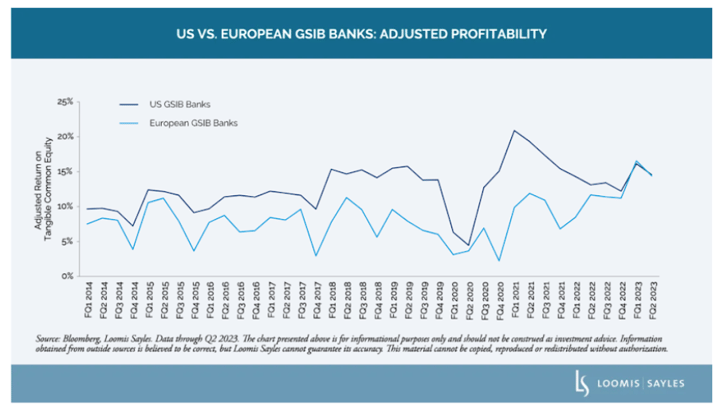

Profitability has substantially favored US banks over the past decade, thanks in large part to negative interest rates in Europe. More recently, the tables have turned and European bank profitability has improved while US bank profitability has deteriorated; a trend we think will continue in the months ahead. Many European banks’ net interest margins are rapidly expanding as they benefit from the end of negative interest rate policies and very low deposit betas. Earnings growth is strong enough that a number of countries have implemented a windfall tax on bank earnings. US banks, especially regional banks, are seeing their net interest margins decrease as funding costs associated with pressure from deposit outflows rise significantly. Even the inverted yield curve weighs more on US banks’ net interest margins as the long-term nature of the residential mortgage market makes it more expensive to borrow at short rates and lend at long rates. Finally, we believe provisions for credit losses will likely be higher at US banks with significant exposure to CRE.

A potential opportunity in Yankee bank bonds

For investors, the trends above suggest to us that European banks are positioned to outperform US banks in the months ahead. Yankee bank bonds (bonds issued by non-US banks in the US, denominated in US dollars) tend to trade at wider spreads than their US counterparts. We believe that with careful research, Yankee bank bonds could present an attractive opportunity for value-oriented investors.