Should we fear a tech bubble?

20 JUN, 2024

Authors: David Rainville, Luca Fasan, Marie Vallaeys, Fund Managers at Sycomore AM, part of Generali Investments ecosystem

Strong performance, higher than historical valuations, Nvidia – are the main topics investors want to discuss these days, with a follow up question on whether there is still upside for the sector from here.

Our answer is simple, we believe there is still significant upside in the sector and would use any weakness as buying opportunities.

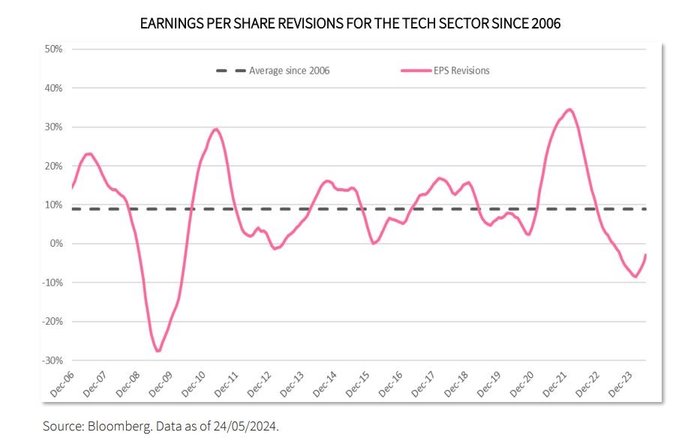

Why? We are coming out of one of the worst 18-month periods for tech fundamentals since the great financial crisis in 2008. With significant negative earnings revisions behind us, we think we can look forward to a strong cyclical recovery in technology – even when forgetting about the excitement around AI.

We are currently seeing real “green shoots” of demand in certain pockets of tech that we believe are leading indicators for the beginning of a strong earnings revision cycle in the sector. Particularly, we look at new spend on public cloud platforms (Microsoft Azure, Amazon Web Services, and Google Cloud Platform), which troughed in early fall last year, and has since been accelerating strongly (even when adjusting for AI spend).

We expect these positive developments to start impacting spending in PCs, servers and eventually on enterprise software (more in the second half of this year), which will help broaden out a potentially strong positive earnings upgrade cycle.

Furthermore, despite the incredible start of the year in January and February for the tech sector, we remind investors that Tech is not driving most of the equity market performance YTD. Specifically, tech in the U.S. is up less than 10% vs. the S&P 500 at 10.4%. The best performing sector this year is Utilities, at 11%, not technology.

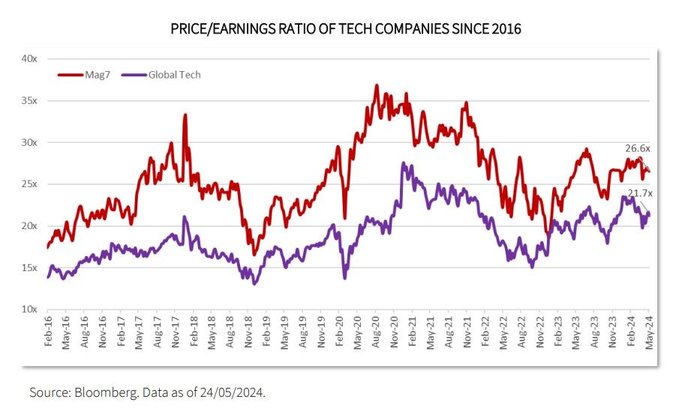

When it comes to valuation, the median tech stock globally trades on 22x P/E, against a 5-year average of 20x. However, when we look at the historical earnings revision cycles in tech, multiples do not have to expand higher for the tech sector to not only generate positive returns, but also outperform the rest of the market.

This means to us that earnings growth matters most. Hence, despite higher than historical multiples, we are upbeat about the prospects for the sector, based solely on the sheer earning power these companies can exhibit over the next 24 months.

Nvidia, the engine of AI

Nvidia has not disappointed. On the contrary, the global manufacturer of microchips used to train and operate artificial intelligence models unveiled spectacular quarterly earnings on May 22nd. The company has once again beaten consensus estimates, reporting sales of 26 billion dollars (the consensus was expecting 24 billion dollars). Widely seen as a barometer for the AI industry, Nvidia has also published upbeat guidance for the next few months. The stock has topped the symbolic threshold of 1,000 dollars but is still trading at multiples that are not yet showing signs of exuberance, in our view.

We expect Nvidia’s share of the AI microchip market to remain above 80% for several years, thanks to the company’s technological leadership over its rivals and the high barriers to entry within the industry. Going forward, the robust growth delivered by the company – in which we remain fully invested – will inevitably trickle down to the supply chain. We are therefore convinced that companies supplying components or services supporting AI graphics processing units also stand to gain.

Consequently, we recently initiated positions in Asia Vital Components, the Taiwan-based supplier of hardware components, Astera Labs, the US provider of semiconductor solutions, and Vertiv. The latter, which is based in the US, designs water-cooling technologies for data centers, which help lower the total energy consumption of these power-hungry facilities by 10%

Furthermore, we strengthened our investments in Micron, the US-based and leading manufacturer of memories, and in Wiwynn and Delta Electronics, both Taiwan companies. The first, which supplies cloud computing infrastructure, offers products aimed at improving the energy efficiency of data centers and servers, enabling them to be more environmentally-sound.

Delta Electronics develops innovative energy-efficient power products. In 2022, the group’s products helped to save 4.02 billion KWh of electricity and lower carbon emissions by 2,046 million tonnes. Delta’s goal is to achieve 100% renewable energy consumption throughout its global operations by 2030, up from 63% in 2022. The group’s founder and honorary chairman, Bruce Cheng, was hailed as “CEO - Chief Environmental Officer” and “The Godfather of Taiwan’s Tech” by the Taiwan media in recognition of his commitment to preserving the environment.

A diversified portfolio that excludes GAFA stocks

We are aware that the risk of a bubble forming cannot be excluded and therefore remain vigilant and flexible in our investment approach. We select companies we believe offer the best upside potential, adjusted for financial and sustainability risks, within promising sub-sectors. These include new ways of working, the digitalisation of industries - such as construction, or cybersecurity. Considering the upbeat forecasts on AI, we have intensified our investments across the value chain.