Tap uncorrelated Asian alpha via quantitative strategies

26 FEB, 2026

By Michael Sun from Eastspring Investments

Michael Sun, Director of Quant Capability and Client Portfolio Manager, Eastspring Investments

Quantitative investment strategies have been employed in equity markets for many decades, with such approaches first taking hold in the US market and later trickling across the globe. In Asia, they have gained more traction as data availability improved and investors increasingly turned to systematic tools to navigate the region’s complexity.

Unlike developed markets, Asia is highly heterogenous. Each country has its own economic drivers, policy cycles, market structures, investor behaviour, and governance standards. This diversity implies that stock returns in the region are often driven more by country‑specific factors than by sectors. Quantitative strategies, with their systematic factor lenses and ability to process vast cross‑market datasets, are uniquely well‑suited to decoding these idiosyncrasies.

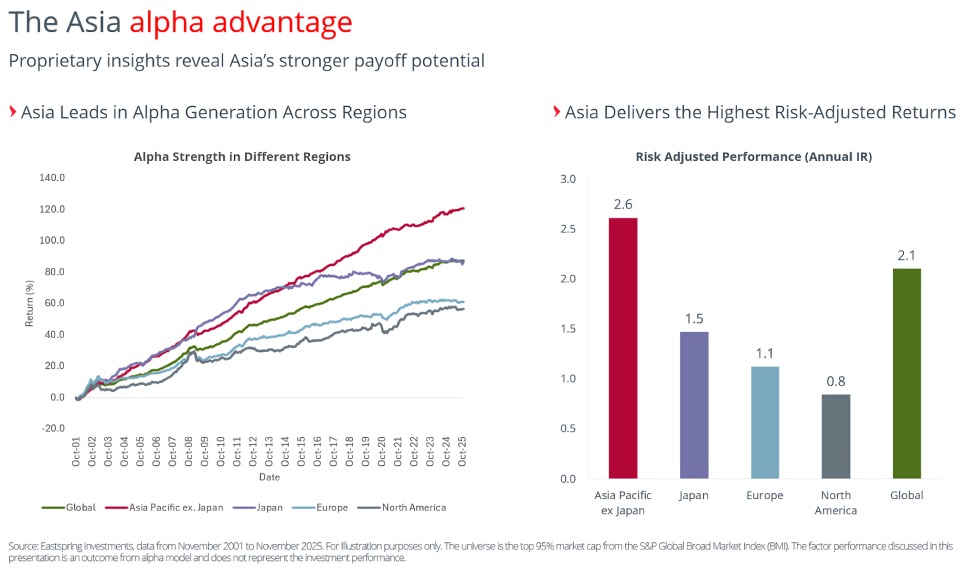

Crucially, this structural diversity is not just a challenge to be managed, but a source of opportunity. The dispersion created by differing country cycles, policy regimes and market behaviours in Asia tends to generate richer and more persistent alpha pools than in more synchronised developed markets. As the following chart illustrates, when these country/sector level inefficiencies are systematically captured, Asia has historically delivered both stronger alpha generation and superior risk‑adjusted returns, highlighting the region’s distinctive quantitative advantage.

Understanding these country‑driven dynamics is essential, especially as new risk patterns begin to take hold. Across global markets, concentration risks are rising. Asian markets are also exhibiting rising concentration, mirroring the trends seen in the US and developed markets. The effective number of stocks in Asia Pacific ex-Japan is now well below its long-term average.

This is a good reminder of the importance of diversification across sectors, regions and style factors such as value, momentum, low volatility, quality, and size (small cap). Such factors offer distinct return characteristics, enabling investors to capture broader market trends. Individual factors are expected to deliver long-term returns, but they can be cyclical in the short term. However, their returns do not move together thanks to differing economic cycle exposure.

A multi-factor strategy broadens exposure to cyclical, defensive, and dynamic factors, thereby enhancing diversification and reducing concentration risk. This approach captures long-term outperformance while smoothing short-term market swings and managing benchmark deviations. Pure defensive styles like low volatility may lag during narrow speculative rallies but they remain essential building blocks in a portfolio for their ability to cushion downside risks and deliver more consistent returns over time.

Some of the factors are geared towards alpha generation, while others serve as risk controls, each playing a distinct role in portfolio construction. Expanding the range of uncorrelated alpha sources is key to managing risk and reinforcing portfolio resilience.

Uncorrelated alpha can be unlocked by adopting a multi-factor investing strategy that selects low-correlation factors to enhance diversification and reduce risk within the portfolio. Correlation can be examined in two ways. One way is to look at the cross-sectional correlation of alpha factor exposures. For example, value and momentum typically display a fairly consistent negative relationship, largely because of how each factor is defined. Stocks with strong momentum where prices have risen rapidly tend to look expensive compared to slower moving measures like fundamentals. Conversely, stocks that have declined in price tend to look cheaper and are more likely to be classified as value stocks. The other form of correlation is the time-series correlation which examines how factor returns move together over time.

Combining traditional and alternative data with advanced algorithms has expanded the search for orthogonal alpha signals, creating a broader set of uncorrelated return drivers. Equally, it is crucial to consider the correlation between alpha factors and risk factors. The lower the correlation between them, the greater the clarity investors can achieve in risk-return analysis, leading to more efficient portfolio construction and optimisation.

Eastspring’s team of quantitative specialists has extensive experience operating in some of the world’s most diverse, illiquid, and inefficient markets. The investment process is continually reviewed to ensure it evolves with changing market conditions, while new data sources and data types are actively explored to enhance modelling capabilities and support the delivery of excess returns.

In 2026, markets are likely to remain fast-moving and volatile. Incorporating uncorrelated alpha sources reinforces the value of combining complementary factors to help manage risk and enhance portfolio resilience. Whether it is a single or multi‑factor smart beta solution with fully customised tracking strategies, the team offers cost‑efficient approaches designed to meet a wide range of portfolio objectives.