Time to buy Value stocks

13 JUL, 2023

By GMO

By Tommy Garvey, a member of the asset allocation team at GMO.

The first, and most compelling, reason to buy Value stocks now is because they represent an excellent investment opportunity – in both an absolute sense, and also relative to the broad market. Simply to return to its median level of relative valuation, Global Value would need to outperform Growth by an excess of 50% from here.

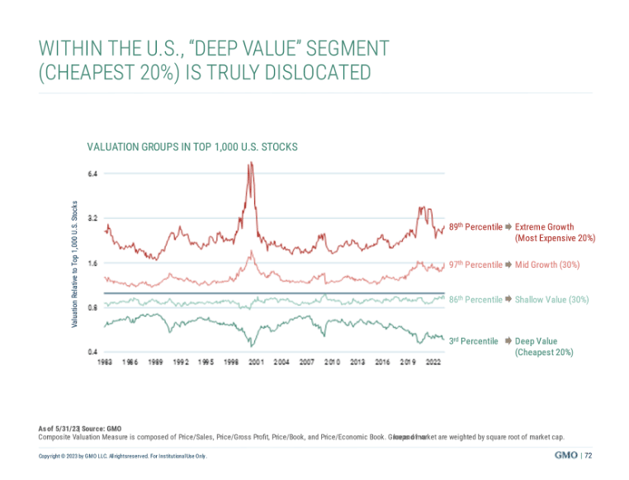

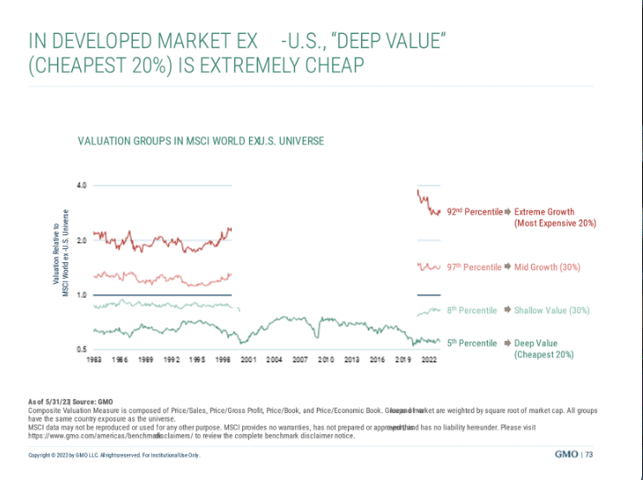

However, we believe that a focus on the cheapest 20% of the market, or Deep Value, could yield even better results. This is particularly true in the U.S. where we observe that Shallow Value actually looks expensive on a relative basis compared to history.

Cheap does not mean junk

Importantly, leaning into cheap does not mean leaning into junk. When we talk about Value stocks, we do not just mean low Price to Book, or a similar basic (but flawed) metric, but rather stocks that are trading cheaply with regards to their quality and fundamentals. Indeed, we believe that it is possible to build a diversified portfolio of stocks from the Deep Value cohort that has both higher ROE and lower leverage then the broad Value index.

Even if it is not junk, surely Value will do badly if we enter a recession?

A core concern for investors contemplating taking advantage of the incredible cheapness of Deep Value stocks today is the potential for a near-term recession. A common perception is that Value stocks are more cyclical and therefore more vulnerable to economic downturn.

We find that this conventional wisdom is false: empirical evidence shows that value stocks actually tend to outperform in recessions. While plenty of value stocks will end up disappointing investors when a recession comes, historically they have not been any more likely to disappoint than their growth counterparts. It is the disappointing growth stocks that are the biggest headache for investors, since their disappointments call into question their premium valuations. Value stocks, by contrast, have the charm of low expectations. No one is expecting all that much from them, so they have less to lose in an economic environment in which companies of all stripes wind up having a tough time.

Take a second look

Our analysis suggests that the prospect for deteriorating economic conditions in no way impairs the thesis that Deep Value is priced to significantly outperform the rest of the market. In a market that seems fraught with risk, deep value stocks are underheld by most investors, despite their extraordinary valuations. We would encourage anyone holding back on buying Value due to recession fears should find comfort in history and take a second look before passing on this wonderful opportunity.