The titles and sectors that are outperforming the Magnificent 7

9 DEC, 2024

By Duncan Lamont

Author: Duncan Lamont, CFA, Head of Strategic Research, Schroders

In 2023, I had stated on several occasions that the Magnificent 7 (Nvidia, Apple, Microsoft, Alphabet, Amazon, Meta Platforms, and Tesla) were dominating global stock markets in terms of performance. Some continue to support this thesis even today. They couldn't be more wrong.

This year, a significant percentage of global companies have outperformed most of the Magnificent 7. All of this is not only due to the recent recovery in China. Even in the United States, a similar percentage has outperformed these companies.

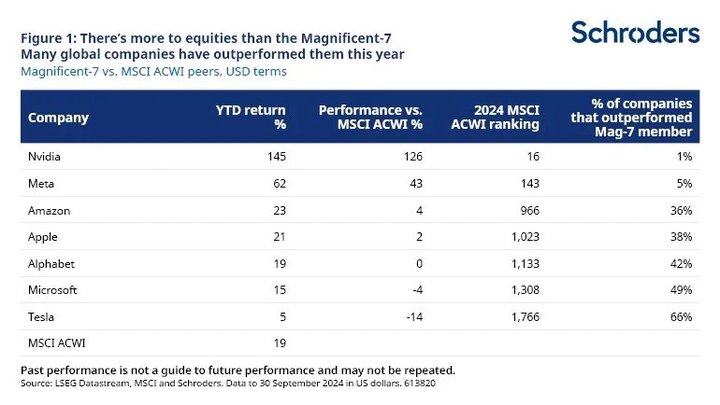

Beware: many of the Magnificent 7 are undoubtedly excellent companies. Some of them have accumulated returns for so long, while still growing more and more, that detractors have been regularly forced to show humility. I do not mean to say that they are bad investments, but simply to underline that they are not the only valid investments: suggesting this would be shortsighted. As Figure 1 shows, with the exception of Tesla, all have achieved good returns this year. But other companies have shown even better results.

A similar trend is also found at the sector level. On all major markets, this year the best performance was that of the US utility sector, normally considered less attractive, which achieved an impressive gain of 32%. Financial stocks also performed well in many parts of the world. The same goes for Japanese and British industrial stocks, which showed similar results. Emerging Asian countries also proved solid. In short, tech stocks are only part of the story: the markets also have more to offer.

The theme, in this case, is that of expansion. While last year's returns, beyond the Magnificent 7, were mediocre on a comparative basis, this year there have been many opportunities, often overlooked. All this goes beyond the movements of stock prices. If we consider the next 12 months, it is expected that, for almost half of the companies listed in Europe and Japan, there will be a double-digit growth in earnings per share in terms of local currency. This figure is equal to that of the much-celebrated United States. The United Kingdom is no less. The figures for emerging countries are even higher (over 60% expect double-digit growth). This is because these are nominal figures and inflation is significantly higher on many emerging markets.

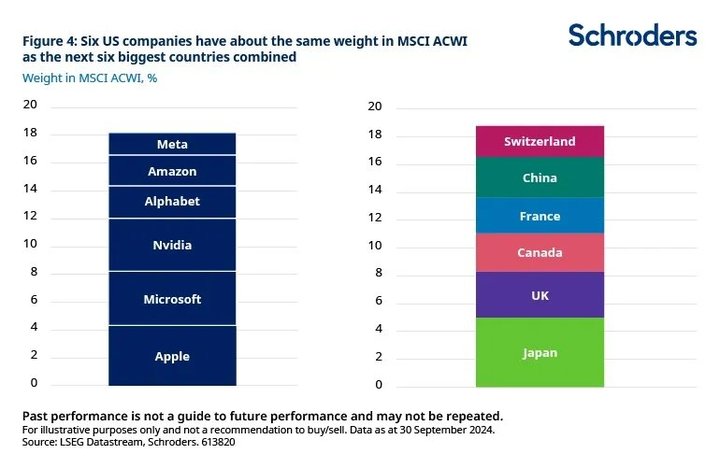

The problem for equity investors is that, although performance is expanding, their respective portfolios are not. The six largest US companies (Magnificent 7, excluding Tesla) represent a share of the global stock market greater than the combined weight of the next six largest countries: Japan, United Kingdom, Canada, France, China, and Switzerland. Six stocks, six countries. Their weight of 18.1% is equal to that of the 2,000 smallest companies in the global market combined.

This translates into a high risk concentrated in a handful of titles, with little exposure to the wider set of opportunities. Moreover, these other companies are much more affordable in terms of valuations, both in the United States and globally. The equal-weighted version of the stock market, which measures the average large-cap company (instead of being influenced by their relative sizes), highlights this opportunity in terms of valuation. Even small cap stocks are cheap compared to historical trends.

In any case, the expansion of performance compared to the Magnificent 7 should not be a surprise. It is rare for a company among the top 10, or even among the top 100, to remain at the top for consecutive years. Prices show an excessive upward trend, fueling overly optimistic growth expectations. Other companies are overlooked and their stock prices languish, fueling overly gloomy expectations. This situation can last for a certain period of time, as more and more investors are sucked into a cycle characterized by exaggerations, until, finally, the rope breaks. The winners of the past are overtaken by those who had been forgotten and fall in performance rankings.

Historically, periods of high index concentration (where a small number of companies have prevailed) have heralded periods where the largest companies have underperformed the average company. There are opportunities beyond the mega-caps, but portfolios have an increasingly reduced allocation.

My concern

The proportion of passively managed assets worldwide has never been so high. The reasons are absolutely known and understandable. However, it is worth for investors to at least reflect on what all this really means on the current market. Six stocks, six countries. Six stocks, 2,000 stocks. Today's global stock markets offer huge opportunities, but rarely have passive portfolios been so little exposed to them. Individual decisions may be understandable, but I fear that the timing may be inopportune. Time will tell if I am right.