Trick or Treat in the Luxury Sector?

17 OCT, 2024

By Kevin Thozet from Carmignac

Author: Kevin Thozet, member of the investment committee at Carmignac.

After two years of extraordinary growth, the luxury goods sector has found itself under pressure in recent months. Revenue has decelerated and is expected to flatline until the end of the year. And equity prices, after reaching all-time highs, have come down. This ‘normalisation’ has left some investors fearful, seeing them slide down the ‘slope of hope’.

Optimism around a resurgent Chinese consumer has faded. So too has the hope for indefinite revenue growth at 3x GDP rather than the (still enviable) 2x GDP. Add to this, rising production costs, expensive digital transformations and flaring geopolitical tensions, and on the surface, it seems like a pretty eerie picture.

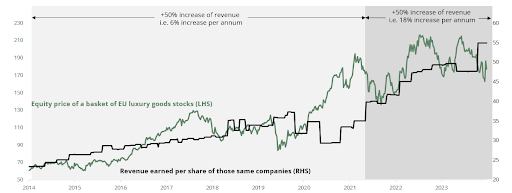

Chart: Evolution of share price and revenue performance of a basket of EU luxury goods stocks

But dig a bit deeper, and it’s clear the wolf isn’t at the door.

The million-dollar question

For investors, the pace at which sales pick-up will be paramount. But the anguish is not only linked to the top-line, EBIT matters too. Growth at 2% or at 6% will make a great difference.

In the luxury sector, fixed costs typically account for two thirds of total costs – and rising. Real wages are positive, commodity prices are high and in much of the west, leases are indexed to inflation.

For a company like Hermès, where sales grow above the 5% bar, cost deleveraging is unlikely, so not much of a scare. But for groups where expenses are growing faster than sales, it is more of a challenge.

Earnings season and a decisive French budget

The luxury sector has a reputation for cutting expenses at cycle lows and overspending at cycle highs. And here we are again. Sales have peaked for most luxury companies and margins are slowing everywhere.

Further spooking investors is France’s decision to increase corporate tax to “find” €60 bn to fill a 6% deficit given this increases the widespread risk of missed earnings across the sector. Indeed, Barnier’s draft budget for 2025 introduces a “temporary” 5% to 10% increase in corporate tax for those largest groups. And as Milton Friedman said, “nothing is so permanent as a temporary government program.”…

Our estimation is that such measures will shave 2% to 4% off the earnings per share of France-based luxury groups in 2025. Not to mention the potential adverse effects of an additional income tax (Exceptional Contribution of High Revenues – aka CEHR) on the wealth effect of those most inclined to buy luxury goods.

At LVMH – often seen as the sector’s archetype - third quarter revenue is broadly expected to grow by 2.5%, driven by leather goods and perfume/cosmetics (primarily in the US) and an improving trajectory in wine and spirits, albeit still negative. At face value, this sounds OK. But our take is a tad more cautious. The pace of deceleration may have been underappreciated and its investments (Formula 1 sponsorship, the Olympics, seven-to-eight figures fashion shows) at a historical top-line peak have been on the high side. The spectre of cost deleveraging could rear its ugly head.

Kering and Burberry are in somewhat similar positions, but with revenue decelerating by double digits, cost deleveraging could be massive. Any cuts could be painful, as they would weigh further on the (already negative) growth outlook for groups at the bottom of the class.

In contrast, L’Oreal, which generates 40% of revenue from luxury, is less impacted by cost deleveraging as the proportion of variable costs (50% of total costs) is higher than elsewhere. Although the group should see its top line revenue decelerating from high single digit, and earnings growth move to mid to low single digit, this is consistent with the historical blueprint of the French cosmetics group.

And top-of-the-class, Hermès should see revenue growing at 10% everywhere but Asia ex-Japan and France. Its leather goods and ready-to-wear divisions will be doing most of the heavy lifting. Contrary to some its peers, price hikes don’t equate to gouging and as a result, have not alienated shoppers.

From bogeyman to ally

While the short-term challenges faced by some luxury groups is likely to be more ‘trick’ than ‘treat’, the longer-term outlook is more positive. The start of a global rate cutting cycle and recent policy actions in China should limit downside potential.

For those investors willing, and able, to look beyond the ‘wall of worry’, 2025 is poised to be an appealing year for the sector driven by several tailwinds.

Firstly, Chinese offshore demand should be revived by the middle-class confidence boost resulting from the fiscal and equity market shot (China accounts for 25% of the sector demand). Secondly, the improved economic trajectory of the US and Europe And thirdly, the sector is blessed by the lack of elasticity of sales volume to price changes.

In the absence of an economic ‘hard landing’, 2025 should see revenue move from “slowing to normalisation” to “growing towards normalisation”. Thus casting a much more positive spell on the sector.