US Election: tight polls leave a wide range of possible market implications

5 NOV, 2024

By Thomas Hempell from Generali Investments

Thomas Hempell, Head of Macro & Market Research, Generali AM (part of Generali Investments).

- Markets seem heavily tilted towards a Trump victory, discounting also a high probability of Republican control of Congress. A Republican sweep seems quite likely if Trump wins, much less so if Harris wins.

- Given the tightness of the polls, it is quite possible that the outcome will be decided by a few votes in one or very few states.

- Post-election, sentiment tends to improve and there is a better chance of a more positive ISM momentum. The ECB easing cycle is an additional positive factor, and Chinese stimulus could alleviate some of the current negative sentiment on EMU exporters.

Polls are showing Trump making gains but the lead over Harris is very small. Bets are clearly pointing to a Trump win, but pricing may be distorted by the build-up of few large tickets. Markets appear heavily tilted towards a Trump win, also discounting a high likelihood of a Republican control of the Congress.

What matters much, especially for fiscal policy, is whether the new president will enjoy the backing of the Congress. A Republican sweep appears quite likely if Trump wins, much less so in case of Harris.

Given the tight polls in key swing states, a repeat of what happened in 2000, when the President was proclaimed only after one month of litigation, cannot be ruled out.

With either party gaining control of both the White House and the Congress, fiscal expansion and (in case of Trump) tariffs may lead to higher rates and a strong USD, putting pressures on EMs. A Trump win would favour US HY and equity at the expense of EMU.

A few hours away of the US election, uncertainty on the outcome is umprecedently high. Therefore, the range of outcome in terms of fiscal and trade policy remains wide. In what follows we recap the key issues investors should consider.

Polls versus bets

Polls continue to point to a tight race, but the advantage Vice President Harris had built after her nomination seems to be evaporating fast. Nation-wide polls and those in the seven states that will decide the election (Arizona, Nevada, Georgia, Michigan North Carolina, Pennsylvania, and Wisconsin) are moving towards Trump. The swings in betting odds has been more pronounced, although the large advantage for Trump seems to have being driven by very few, large positions. More complex models, which blend polls and macro data, like the one maintained by The Economist, show that the odds of winning have moved from 55 to 45 in favour of Harris to (at the time of writing) 50/50. The recent moves, with stronger US equity market and USD and weaker Treasuries suggest that markets have followed the evolution of polls, and are tilted towards a Trump victory, also discounting a high likelihood that the control of the Congress would enable the Republican party to implement its agenda. Therefore, a sharp correction may be on the cards should Harris win on Tuesday night.

Split vs unified government and economic policy options

A large uncertainty also surrounds the outcome of the election for the Congress, with the latest polls giving Republicans a small edge in the Senate and Democrats in the House of Representatives.

Given past voting patterns, a Trump win would be more likely associated to a full Republican control of the Congress than a split government (a situation in which the president faces at least one branch of the Congress controlled by the opposition). On the opposite, Harris seems very unlikely to enjoy the backing of both Houses.

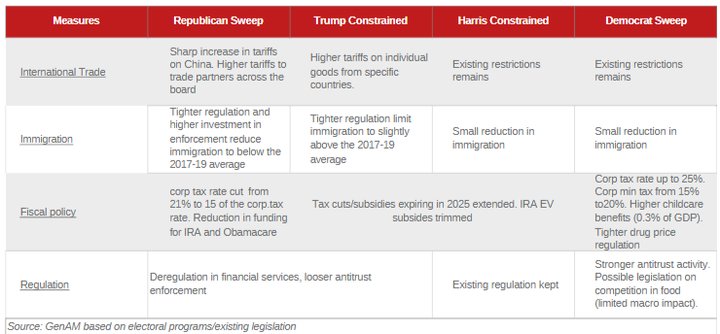

The balance of power has extremely important implications for policymaking in the most impactful issues for the economy and financial markets: trade and fiscal policies. The table below summarises the balance between policy ambitions and the constraints imposed by the division of powers. On trade, the steep and far-reaching tariff rise threatened by Trump could only materialise if the Congress overhauls trade policy. The President could impose specific tariffs on a limited set of goods or services, resulting in a much lower economic impact. The same applies to fiscal policy: the bold initiatives on taxes promised by Trump and on social expenditure by Harris need a solid backing by the Congress. In a split government scenario, the most that can be achieved is a bipartisan agreement on extending, at the end of 2025, the Tax cuts legislated by the Trump administration and the higher welfare outlays by the Biden Administration.

To gauge the range of economic outcomes, we modelled the impact of proposed policies under the four possible scenarios: full majority by either party and split government. If applied in full and followed by retaliation by trade partners, the tariffs proposed by Trump would lead to a sharp increase of inflation and a sizeable drop in US GDP (more than 1% by 2029) relative to a no-change baseline, challenging the rates normalisation expected from the Fed. Repercussion will be felt elsewhere, with GDP lower by around 1.5% in China and EU exporters like Germany severely affected. The fiscal expansion proposed by Harris would result in a milder increase in inflation and higher, debt fuelled, GDP.

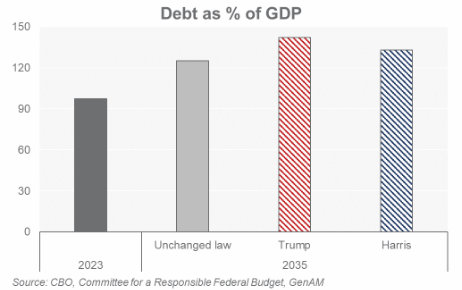

What is certain is that under none of the scenarios, Federal debt would stabilise, as no party shows appetite for fiscal responsibility. Detailed scenarios developed by the bipartisan Committee for a responsible Federal Budget, by 2035 federal debt would increase by some 45pp under Trump, if the proposed far-reaching tax cuts are unfunded, and 36pp under Harris, compared with a 28pp rise under current legislation.

A repeat of 2000?

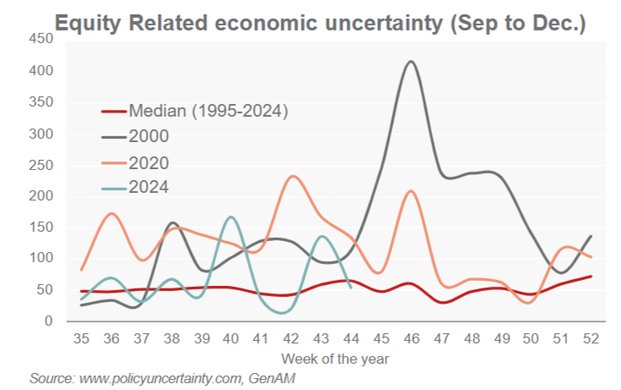

Uncertainty also involves when and how the President will be proclaimed. Given the tightness of the polls it might well be that the outcome will be decided by a few votes in a single or very few States. Then, there might be a repeat of what happened in 2000, when George W. Bush won by a few hundred votes in Florida and was proclaimed only after one month of recounting. The spike in uncertainty had a significant weigh on business and inflation expectations in the final months of 2000. The political environment has turned more polarised since 2000 and the spike in uncertainty could be much bigger.

Financial Market implications

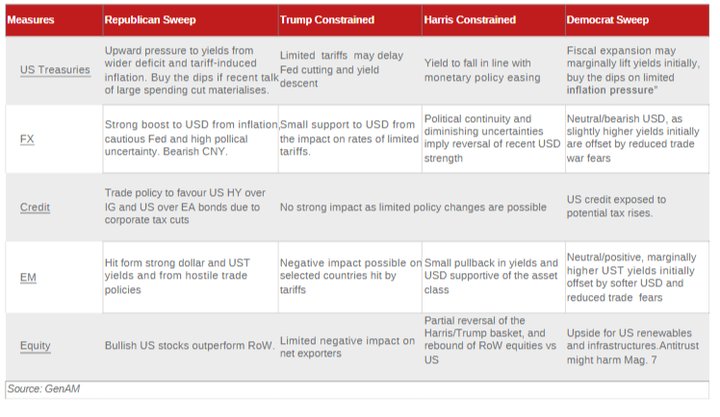

The table below sketches what could be the implications for the main asset classes, followed by a more detailed discussion.

Treasuries

A Trump presidency could prevent yields from falling, at least in the short run. The impact would be stronger in case of a sweep victory by either party as their proposed expansionary fiscal policies could be implemented in full. Additional fiscal stimulus should push up both short- and long- term yields. By contrast, the impact of new tariffs on US yields is more uncertain. While more cautious key rate cuts by the Fed could lead to upward pressure at the short end, the evolution of long-term bond yields depends on the extent to which the higher term premium is offset by weaker growth.

Overall, the highest yields are expected in the event of a Trump victory combined with a Republican sweep in Congress (transatlantic yield spread to widen further in this scenario). A Harris victory combined with a split Congress would likely to result in the biggest drop in yields. However, it should be noted that Trump's increased chances of success have already contributed to a rise in yields, limiting the additional market reaction in the event of a Trump win. Also, the assumptions of a bolder fiscal stimulus in a red sweep may eventually be challenged. In the final weeks of the campaign, Trump, and his ally Elon Musk, have talked about massive spending cuts to reduce the size of government. If true, this would clearly question the current market assumptions of a bolder fiscal expansion. In all, we tend to see the 4.5%-5.0% range (10-year UST) as a buying opportunity in case of a post-election sell-off on a Republican sweep.

US Dollar

A Trump victory would boost the USD, with the inflationary pressures from tariffs and a likely more cautious Fed favouring a higher US yield advantage vs. major peers. Higher odds of a Trump victory have already boosted the USD over recent weeks. Global policy uncertainties and rising political tensions (risk of a tit-for-tat trade war) are likely to raise safe-haven bids, also to the benefit of the greenback. Prospective tax cuts and political pressure on foreign producers to boost production shares in the US would raise US FDI inflows and thereby the USD, especially in case of a ‘red wave’ with Congress backing Trump policies. A Harris victory would work into the opposite direction. Since her policies would be less disruptive, i.e. leaning more towards continuity, the FX reaction may be more muted, though.

Credit

Aggressive trade policies tend to favour US High Yield (HY) over Investment Grade (IG), due to their domestic versus global focus, and the US market over Europe. Moreover, US banks could benefit from significant deregulation in a Republican sweep, while healthcare might face challenges from price reforms under both Republican and Democratic sweeps, with lower risks in a split outcome. Fiscally, corporate tax cuts in a Republican sweep could provide substantial benefits, though potential reflation from tariffs poses more risk to equities than bonds, with High Yield being less exposed than Investment Grade.

Emerging Markets

A Republican sweep would be the worst scenario, even more since spreads and local debt yields have performed gently over the past month. EM fixed income would be hit by a stronger USD, upside pressure on core rates but also by changes in foreign and trade policies. The 2016 election could serve as a template, even if the bar for surprise is now higher. Initially EM FX high-yielders and local rates performed poorly but both external and local debt recovered in 2017 with spreads even going tighter despite higher US rates. EM began to suffer afterwards when protectionism risks materialised. In the current environment, the short-term risk is to see some EM FX high yielders underperformance and the depreciation of the Chinese Yuan. The currencies of Mexico and other open economies like the Czech Republic and South Korea would underperform. EM external debt would be more immune, with the spread reaction likely contained but the expected US yield rebound affecting total return. For EM local rates, curves should globally steepen but we could also see divergence in EM responses. Some central banks in Asia and Central Europe would have room to cut to lean against tariff hikes while in LatAm we should see defensive rate hikes or more hawkish rhetoric to preserve financial stability.

Equity

Historically, both the US and EMU equities tend to gain post-election as uncertainty drops. In a Trump split scenario, we see positive 3m and 12m total returns, for both the US and EU, driven by macro fundamentals and Central banks easing. EMU has a higher risk profile, could underperform initially, but with higher 12m TR potential given the current valuation.

The Goldman Sachs Trump basket, axed on cyclicals such as energy, financials, and domestic industrials, has recovered massively since mid-September (+10%, and 8% YTD), given strong data and higher chances of a Republican win. The basket should continue to perform well even if the Republicans do not take control of the Congress. EU net exporters (Auto, Electronic equipment) have suffered, down 10% YTD and in a perspective of Trump victory we see no appeal for them. Our trade fear indicator also points to continued risk for EU cyclicals vs. Defensives, which add to the negative earnings revisions for Autos - albeit they recently reached a cyclical low that has only been tested 5 times since 2009.

The Democratic basket (focused on renewables, healthcare, and Infrastructures) has lagged behind (-9% since mid-Sept., -2% YTD), and it has less chance of recovering if Harris wins, given the low probability of a Democratic majority capable of implementing the announced policies.

For now, we suggest a balanced allocation between EU cyclicals and defensives. First, post-election, usually sentiment improves and there are higher chances of a more positive ISM momentum. The ECB easing cycle is an additional positive, and the Chinese stimulus could alleviate some of the current negative sentiment on EMU exporters. EU firms based in the US (industrials, healthcare, staples) should perform in line with EMU, which we expect to do decently well next year, only temporarily affected by a Trump win. Indeed, EMU has already underperformed the US by 13%, with the risk premium over the US at historic highs.