US high yield: Playing the short game

18 JUN, 2024

By Bryan Petermann

Author: Bryan Petermann, Portfolio Manager at Muzinich & Co

The last two years have been volatile for investors, primarily due to the Federal Reserve’s (Fed) rate-hiking programme, which began in March 2022.

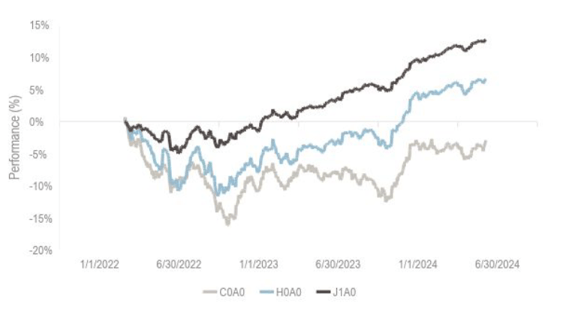

This year, markets are still being impacted by rate volatility due to continued economic growth and stubborn inflation that are delaying rate cuts. This has caused longer-duration fixed income assets to underperform their shorter-duration siblings (Figure 1).

Figure 1: Longer duration fixed income has underperformed

What is short duration high yield?

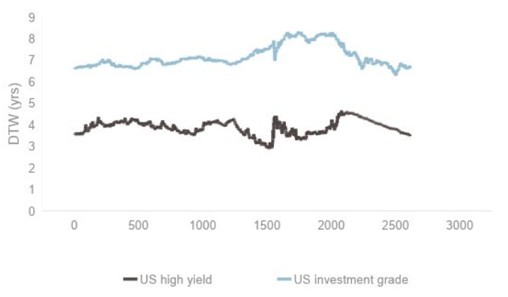

The US$1.3 trillion US high-yield market has a shorter duration (duration to worst – DTW) than US investment-grade (IG) corporates. Several factors influence duration, most notably bond price, coupon, call schedule and maturity. However, US high yield has produced a shorter duration relative to investment grade by 2.24-4.96 years on a consistent basis over the last 10 years (Figure 2).

Figure 2: US high yield is shorter in duration than US investment grade

ICE BofA ML US Corporate Index (C0A0). Indices selection represent best proxy for asset classes

being discussed. Index performance is for illustrative purposes only. You cannot invest directly in

the index.

Short-duration high yield (SDHY) is an even shorter duration subset of the high-yield market. There is no specific definition of short-duration high-yield bonds, but indices typically focus on either a duration range (e.g., 0-3 years) or a maturity band (e.g., 0-5 years).

The constituent base of DTW-based indices is inherently more volatile than maturity-based indices, since changes in bond prices can cause bonds to enter or exit the index at every reset. Both indices have experienced an average DTW of 1.68-2.27 years over the past 10 years.

Duration is not inherently good or bad for bond investors, it is just a measure of how sensitive a bond or portfolio is to changes in interest rates. The shorter the duration, the less sensitive it is to changing interest rates. As SDHY bonds are less sensitive to interest rate fluctuations relative to IG bonds, coupon income and changes in spreads are more important for their total returns.

SDHY bonds can be considered a purer example of credit risk than longer-duration fixed income assets, which are more tied to underlying economic conditions, their impact on government bond yields and the resulting impact on bond prices and total returns.

Smoothing your return profile

At this point in the cycle, it is difficult to reliably predict how interest rates will perform over any near-term timeframe. Fixed income investors are likely to see continued rate volatility, and hence total return volatility, until the direction of interest rates crystallizes. In our view, this provides an opening for SDHY investments for four main reasons:

1. Healthy economic backdrop: The US economy is expanding, and capital markets are open, both of which reduce the potential for unexpected defaults and credit losses across the asset class.

2. Regular-market-duration comparable: SDHY bond yields and spreads are more or less in-line with the full market, with DTW numbers around two years shorter.

3. Value opportunity: SDHY bond dollar prices, meanwhile, remain below par, an unusual situation in a growing economy, providing an opportunity to realize positive convexity over the near term if bonds are called prior to maturity.

4. Less volatile: Historically, SDHY bonds have proved less volatile than their longer counterparts, meaning investors should see smoother return streams.