US Treasury: the perfect recipe for the fair value of the 10-year yield?

25 JUN, 2024

AUTHOR: Jeffrey Cleveland, Chief Economist at Payden & Rygel

The yield of the US ten-year bond represents one of the most important and influential interest rates in the world and its recent trajectory has puzzled investors: from 3.87% at the beginning of 2023, it first fell to 3.31%, then rose to 4.99% last fall, to then end the year at the starting level. Today, the yield of the ten-year Treasury is around 4.50%. Returning to the "fair value" of the 10-year Treasury is the dream of any bond investor and is only possible if the historical-economic variables are related, trying to identify the three components that define long-term yields, that is, the expected inflation at 10 years, the short-term interest rate curve (adjusted for inflation), and the extra remuneration that investors require to subscribe to long-term bonds.

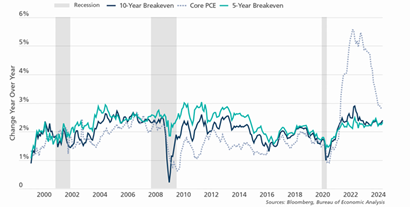

As for the first "ingredient" of the recipe, it is possible to trace the market expectations for inflation at 10 years through the 10-year breakeven inflation rate, in turn given by the yield differential between Treasury Inflation-Protected Securities (TIPS) and nominal Treasuries. Today inflation expectations remain solid (see chart below), as investors trust in the return of inflation close to the 2% target. However, in our opinion, it is necessary to broaden the perspective and consider that before the third millennium, long-term inflation rates were around 6% in the United States and 10% in the United Kingdom, so the last three decades could represent "anomalies" on the macroeconomic front globally.

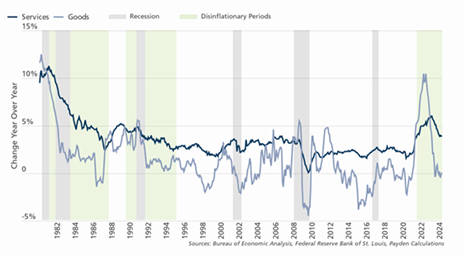

Therefore, there is a hypothesis that, in the post-Covid era, inflation will settle at higher levels than in the last twenty years. After all, once the peak is reached, prices have historically taken some time (from five to seven years) to slow down and the last mile of the disinflation path has often proved to be the most tortuous, due to the slow receding of service prices (see figure below). To date, with the normalization of supply chains, we have witnessed a rapid drop in goods prices, while those of services seem less reactive. In any case, the powerful combination of fiscal and monetary policies of the Covid era if, on the one hand, has led to the explosion of inflation, on the other hand, has tested the solidity of the labor market which today seems in good health. This could lead employment-oriented policymakers to prefer the current situation to the stagnant growth of the 2010s and therefore to opt for a higher inflation target than in the recent past. As investors, it therefore seems prudent to consider a slightly higher breakeven inflation level, around 2.5%, compared to 1.6% in the 2010s.

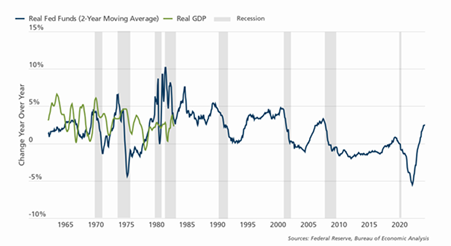

Moving on to the second "ingredient", to trace back to the "fair value" of the 10-year Treasury, it is also necessary to consider the expected short-term interest rate curve, adjusted for inflation. The trend of the Fed Funds rate can be a great starting point, even if in the short term the path of rates can vary greatly as a result of both monetary policy decisions and market expectations on the evolution of rates (so-called Forward Guidance). For this reason, to estimate the trajectory of short-term rates, the best way, rather than analyzing the market's implicit forecasts for the trend of the nominal rate on Fed Funds, is to consider the trend of non-monetary factors such as the expected return on investments, which varies in relation to the expected real growth and which represents one of the main drivers of real interest rates (see chart below). For example, the lower or even negative short-term rates we witnessed in the 2010s reflected stagnant economic growth and a pessimistic sentiment about the economic situation and the return on investments.

As of today, sentiment should be improving, reflecting a more favorable economic situation. Also, real production could settle at higher values compared to the last decade, thanks to the increase in workforce which in the last three years has grown at an average annual rate of over 1.4%, against 0.7% of the 2010s. A decisive role in the increase in real production is then played by productivity, which measures how much is produced by a single worker for each hour worked and which in the last 12 months has grown by 2.9% (against an average of +1.3% in the '10s). If we analyze the productivity of the US workforce in the post-war period[1], we notice how four high and low growth regimes have alternated: the last high growth regime occurred from 1997 to 2005, after 25 years of low growth. More than capital or labor force, the growth of real production will be influenced above all by new ideas, which we are sure will not be lacking in the era of AI and large language models ("Large Language Model"). For this reason, we are convinced that, on the wave of an increase in real production (+2% approximately) we will witness a real interest rate higher than the previous decade, around 2%.

After analyzing inflation and short-term interest rate, the final ingredient is missing, the premium that investors want to see recognized for locking their capital for ten years, certainly not a short period. Economists use various financial and macroeconomic variables to estimate the "term premium" and one of the most common models is the 10y Term Premium by Adrian, Crump and Moench, which in October 2023 reached 0.34%, the highest value since 2015. Given the uncertainty in the post-Covid era surrounding the next decade, we think it is prudent to consider a higher term premium than in the past. Especially in light of the statements from the US Treasury, which has already forecasted $6.3 trillion of new public debt to be issued in the next three years, an enormous figure considering that in 2009 the entire stock of debt in circulation was equal to $6.3 trillion.

In conclusion, investors should be compensated for inflation, inflation risk and other collateral risks, as well as rewarded for the real growth of the economy. Assuming that inflation and real interest rates stabilize at higher levels over the next ten years (respectively +2.5% and +2.0%) and that investors require a higher term premium (0.5%), putting these three variables in perspective, results in a "fair value" of the 10-year Treasury at 4.7%-5.1%. Obviously, no one has a crystal ball, but by observing History and economic variables it is possible to have a clearer idea of the overall picture.