Weakening of the US dollar: Has the end of its hegemony arrived?

6 MAY, 2025

The US dollar is experiencing its worst start to the year since 1995, depreciating more than 8% against the world's major currencies and marking six-month lows. Factors such as the Trump administration's aggressive tariff policy, the increase in the fiscal deficit, and the loss of confidence in US institutions have led to capital outflows and a revaluation of rival currencies such as the euro and the yen.

The weakening of the dollar not only complicates the competitiveness of US exports, but also alters the global balance, impacting everything from commodity prices to the decisions of central banks in Asia and Europe.

The question now being asked by the markets is whether this setback marks the beginning of the end of the dollar's reign as the international reference currency. Experts from international asset managers Wellington Management and J. Safra Sarasin Sustainable AM give us the key.

Marco Giordano, Investment Director at Wellington Management

The erosion of the institutional integrity of the United States can further weaken the status of the dollar as a reserve currency and alter global capital outflows. One risk that the Trump administration may run is that, due to the loss of confidence, countries may be less willing to negotiate than in the past. This risk has accelerated with the administration's tariff announcement and is unlikely to dissipate even if some of these tariffs have been paused for 90 days before their application. There is a higher probability of increased economic nationalism and capital repatriation. We expect this announcement to be the trigger, or at least the accelerator, of net capital outflows from US financial assets to global fixed income, which should imply much higher risk premiums and higher long-term bond yields for the US. In the rest of the world, this could be a significant technical factor to support non-US financial assets, with European, Japanese, and Chinese fixed income potentially benefiting from US outflows.

The currency and US Treasury bonds have already more than completely undone the movement since the November 2024 elections. The euro, yen, and Swiss franc have continued to appreciate in their cross against the dollar, as investors take refuge in safe currencies amid growing geopolitical uncertainty.

The US dollar will face headwinds due to concerns about growth and the disappearance of exceptionalism

Claudio Wewel, currency strategist at J. Safra Sarasin Sustainable AM

In the short term: the dollar has shown a downward trend in recent weeks, as US activity indicators have signaled weakness due to high political and macroeconomic uncertainty. In contrast, hard data remains solid, with a resilient US labor market. We have adopted a cautious stance towards the dollar, especially after President Trump's announcement of very high reciprocal tariffs on US trading partners, which, in our opinion, represents a significant risk of recession. The net speculative position remains balanced between dollar bears and bulls.

In the medium term: Trump's likely political agenda suggests that the Federal Reserve's rate cut trajectory will be moderate, but increasing growth risks could force the Fed to make more cuts than the market currently anticipates, which should contribute to headwinds for the dollar in the short term. With American exceptionalism fading, the US should experience capital outflows that will continue to pressure the dollar downwards. In this context, we are less likely to see the dollar gain ground in the event of a global recession this time. The Trump administration's plans to make reserve dollar assets less attractive to foreign holders constitute another downside risk.

In the long term: the combination of high political uncertainty and the ongoing large external financing needs of the U.S. constitutes a structural headwind for the dollar, in which most of the currencies of the G10 countries and emerging commodity markets should continue to rebound against the dollar, which is highly valued.

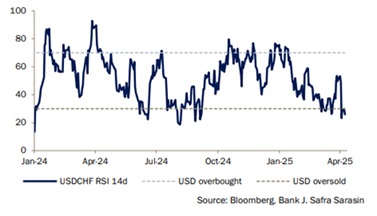

Short-term factors and market sentiment

Relative Strength Index (RSI)