What is going on in the gold sector?

Updated:

4 SEPT, 2024

By Jose Luis Palmer from RankiaPro Europe

Gold has been one of the main protagonists in recent weeks. The latest macro data, the news from Jackson Hole, geopolitical tensions, have put gold back in the spotlight for central banks and even individuals.

Gold and the gold sector are not correlated with other financial assets. Therefore, they can be effective diversification assets in an overall portfolio allocation. In addition, there has been renewed interest in companies operating in the gold sector. Indeed, precious metals producers are the main beneficiaries of rising gold prices.

What is happening and where is gold evolving to? Experts react to the last market movements.

News from the gold sector

Charlotte Peuron, equity fund manager at Crédit Mutuel Asset Management

At the end of August 2024, the precious metal reached a new high, soaring above USD 2,500 per ounce, which translates into an impressive +21% rise since the beginning of the year.

So far, the main drivers that have been supporting gold are:

- Emerging market central banks seeking to diversify their foreign exchange reserves and reduce their dependence on the US dollar.

- The high demand for physical gold (bullion and coins) from Asian countries.

- High demand for jewellery

However, since last summer, demand has been spurred by short-term financial factors. Indeed, US real interest rates have fallen below 2%, a threshold at which it is attractive to buy non-yielding assets such as gold. Moreover, given the current geopolitical and economic risks, gold is seen as a safe haven asset.

Western investors, convinced since the Jackson Hole economic symposium that the Fed will begin its rate-cutting cycle in September to address the US economic slowdown, are returning to the asset class. In addition, and as evidenced by the volume of gold ETF subscriptions during the second half of the year to date (27/08/2024), which have reached close to the equivalent of 2 million ounces, the recent weakening of the US dollar is also a supportive factor. This activity has not been recorded since 2022.

We also see renewed interest in companies operating in the gold sector. Indeed, precious metals producers are the main beneficiaries of rising gold prices. At present, companies are doing very well financially because their costs are under control and their selling prices are rising. As a result, companies are generating very high or even record margins. In fact, for a selling price of $2,500 per ounce of gold, companies' margins could reach 59% on cash cost and 45% on average AISC. In recent quarters, companies have generated comfortable free cash flow and are returning profits to shareholders through dividends or share buybacks. Companies are also reinvesting this cash in mineral resource exploration to increase their reserves or, in some cases, to accelerate the construction of new mines.

The advantage of investing in gold companies, especially during periods when the price of the underlying asset is rising, is that operating and financial leverage can be captured, as well as growth in production and reserves. For investors in these companies, it also means taking advantage of merger and acquisition bonuses, something the purchase of a gold coin cannot offer.

Currently, and as is often the case, gold and the gold sector are uncorrelated with other financial assets. They can therefore be effective diversification assets in an overall portfolio allocation.

Gold demand sources

James Luke, Commodity Fund Manager, Schroders

Changes in geopolitical and fiscal trends are paving the way for sustained demand for gold, and miners of this metal could be poised for a significant recovery.

Western liquidations have been caught off guard by the purchases of central banks, investors, and households in the East. This shifting dynamic has been led by China, but it hasn’t been a reality limited to this country; demand has also increased in the Middle East and other regions.

Geopolitical and fiscal fragility—trends directly linked to demographic factors and deglobalisation, which, together with deglobalisation, characterise the new investment paradigm that we at Schroders have called the 3D Reset—are combining today to forge a path towards a sustained and global push for gold supplies. In our view, this could trigger one of the strongest bull markets since President Nixon closed the gold window in November 1971, ending the convertibility of the US dollar into gold.

The strength of gold reflects the shift towards a more polarised world

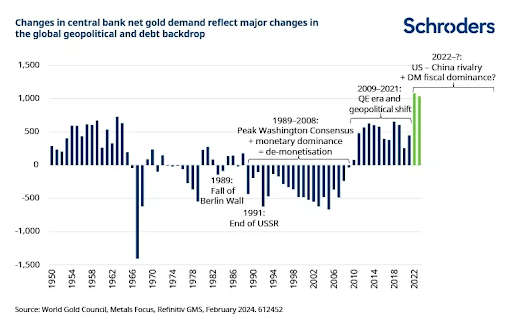

The tightening of tensions between the United States and China, and the sanctions imposed on Russia following its invasion of Ukraine in 2022, have driven record gold purchases by central banks as a reserve monetary asset. The freezing of $300 billion of Russian reserve assets clearly demonstrates what the ‘weaponisation’ of the US dollar—or in other words, the hegemony of the dollar—can truly mean. The massive issuance of US Treasury bonds to finance endless deficits also raises questions about the long-term sustainability of the debt. Central banks—China, Singapore, and Poland, the largest in 2023—have been paying attention, although record purchases have only increased gold reserves from representing 12.9% of total reserves at the end of 2021 to 15.3% by the end of 2023.

From a long-term perspective, central bank purchases clearly reflect the evolution of global geopolitical and monetary/fiscal dynamics. Between 1989 and 2007, Western central banks sold off as much gold as they practically could, although after 1999 they were constrained by central bank agreements designed to maintain order in the sales. In that post-Berlin Wall and post-Soviet Union world, where US-led liberal democracy was thriving, globalisation was accelerating, and US debt indicators were frankly quaint compared to today, the ‘demonetisation’ of gold as a reserve asset seemed entirely logical.

The 2008 financial crisis, the introduction of quantitative easing, and emerging geopolitical tensions were enough to halt Western sales and quietly attract emerging market central banks to the gold market, with an average of 400 tonnes purchased annually between 2009 and 2021. These are significant figures (>10% of annual demand), but not seismic.

In contrast, the more than 1,000 tonnes of gold (20% of global demand) purchased by central banks in 2022 and 2023, a pace that continued in the first quarter of 2024, is potentially seismic. It seems entirely plausible that the current strained dynamic between established and emerging powers, combined with the fiscal fragility looming not only over the reserve currency issued by the US but also over the entire developed economic bloc, could trigger a sustained movement towards gold.

The gold market is not large enough to absorb such a sustained movement without prices rising significantly, especially if other global players also try to enter more or less at the same time.

Gold price likely to benefit from easing monetary policy

Chris Mahoney, Fund Manager for the Gold & Silver Fund at Jupiter AM

The upward trend in gold prices has been accompanied by strong demand for the metal from central banks. Central banks have been consistent buyers of gold since 2010, during which time they have added more than 7,800 tonnes to their reserves. Central bank demand for gold has been particularly strong in recent years, with 2022 being a record year for annual central bank demand for gold. Central bank demand for gold remained high in 2023, almost matching that of 2022.

Although the People's Bank of China (PBoC) paused its gold purchases for the first time in 18 months earlier this year, aggregate central bank demand for gold in the first half of 2024 was robust. In fact, the first half of 2024 was the highest ever recorded for the first half of the year. The sustained purchase of gold by central banks over the past decade has coincided with a shift in their appetite for sovereign debt and fiat currencies. This is particularly evident with respect to US Treasuries and the US dollar, which have historically tended to dominate central bank reserves.

Starting in 2014-2015, many central banks began to reduce their holdings of US Treasuries. This shift reflects a desire by some central banks to diversify away from US government-issued instruments, reflecting both a change in the geopolitical context and a reduced confidence by central banks in the performance of these assets. The move towards gold demonstrates that central banks recognise how gold offers a store of wealth independent of any government or other central bank.

We expect central banks to remain enthusiastic buyers of gold in the future, which is supported by the World Gold Council's most recent survey of central banks: almost a third of the central banks surveyed stated their intention to increase their gold reserves in the next 12 months. The gold price is also likely to benefit from an easing in monetary policy by the US Federal Reserve. The main driver of the gold price is real interest rate expectations, with which it tends to move inversely. Lower interest rate expectations typically bring higher gold prices, so the impending change in Fed policy is positive for gold.