What’s going on with the Magnificent 7?

30 MAY, 2024

By Jose Luis Palmer from RankiaPro Europe

The "Magnificent 7" has become a buzzword in the investment world, referring to the seven leading tech giants that have significantly influenced market dynamics: Apple, Microsoft, Amazon, Google, Facebook, Tesla, and Nvidia. These powerhouse companies have driven substantial gains in the stock market, shaping economic trends and investor sentiment. However, recent fluctuations and regulatory pressures have cast a shadow over their continued dominance. This article delves into the latest developments affecting these tech titans, examining their outlook and the broader implications for the market. As we explore what's going on with the Magnificent 7, we aim to provide insights into their future trajectory and what investors should watch for in this evolving landscape.

Cloud activities boost results

Rolando Grandi, CFA, international equity manager of La Finacière de l'Echiquier (LFDE)

The results of the Magnificent 7 have been good overall

Overall, these companies have confirmed that they are leading companies that maintain high levels of growth and structurally higher profitability than the market, showing that they are extremely attractive business models in a context of high macroeconomic uncertainty. Among the companies that stood out were Microsoft and Amazon, whose cloud activities accelerated in the quarter.

Microsoft, which had a growth rate of 28%, now stands at 31% thanks to its Microsoft Azure business. On the other hand, Amazon saw an acceleration in the growth of its AWS business from 12% to 17%. This shows that the trend of digitisation of the economy and the use of artificial intelligence are enabling an acceleration of growth for these companies.

As for companies that have not performed very well this quarter, we can think of electric vehicles and in particular Tesla, which is suffering in a context of high interest rates that is causing consumers to currently not be able to finance them at attractive interest rates, making it more expensive to buy an electric vehicle. This situation is impacting the company. Faced with this situation, Tesla decided to lower the price of its vehicles to stimulate demand and it is currently working. We expect the situation to improve in the coming months with the potential of a rate cut.

Enthusiasm is justified

We believe that investors' enthusiasm for these companies is justified, especially in a context where growth is rare and difficult. These companies have demonstrated that, despite their large size, they can show high levels of growth.

Moreover, the profitability levels of these companies - the margins - are higher than the rest of the market and they have first class management. In this sense, we are not only talking about the founders, such as the visionary Elon Musk or the entrepreneur Mark Zuckerberg, but also about professional CEOs such as Satya Nadella, CEO of Microsoft, or Andy Jassy, CEO of Amazon.

It's time to differentiate between the Magnificent 7

Investors need to start differentiating between these companies, because while they have been concentrated market performers over the last 15 months, we are seeing growth dynamics that are being different between them. Apple, for example, is experiencing very slow growth and no concrete opportunities in artificial intelligence. On the other hand, we have companies like Tesla, which are suffering in a difficult economic context, but which should improve, as well as cloud companies, which are benefiting from AI, with good results and good capacity to take advantage of this trend.

Another element we are seeing is that the market is starting to diversify performance generation, investing in companies beyond the Magnificent 7. This is a positive symptom for the market, because it shows that the market rally is going to be fuelled by other companies, usually smaller in size, but which also have high growth and profitability prospects.

Will there still be 7 Magnificent?

Chiara Robba, head of LDI Equity at Generali Asset Management (part of Generali Investments)

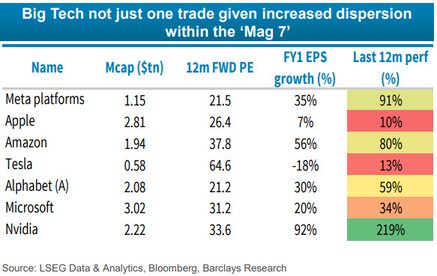

After 18 months of Tech AI euphoria in the US, it is legitimate to ask what the status is of the Magnificent 7 post the 1Q reporting. Overall, big Tech fundamentals looks solid at the moment, with the performance since the beginning of the year still driven by earnings growth rather than multiple expansion. The 1Q S&P reporting is showing a 40% EPS growth for the Tech sector indeed. Nevertheless, if we look more into detail into the Magnificent 7 (Apple, Alphabet, Amazon, Meta, Microsoft, Tesla and Nvidia), probably the two for which the first quarter reporting was not particularly strong were Meta and Tesla.

In particular, Meta traded down 15% in the aftermarket as the 1Q were solid with revenue growth +27% within the Co upper end of the guidance, but the outlook for the 2Q was disappointing and moreover, the higher total capex to finance AI investment came as a negative surprise. As a matter of fact, Meta increased its 2024 capex outlook from $30B-$37B to $35B-$40B as it accelerates infrastructure investments, and capex will further increase also in 2025.

Tesla’s shares were down more than 50% at the end of April compared to the beginning of the year, recently rebounding thanks to a 10% EPS beat on the 1Q results. There is a significant debate around the EV vehicle volumes and profitability in the coming future, so even if the reporting was marginally better than the consensus expectations, gross margin decline yoy was significantly impacted by lower pricing showing the current competitive demand outlook.

Apple and Alphabet had solid results. In particular, Apple has shown some improving trends in Greater China revenues including the i-Phone, that was an area of concern at the beginning of the year.

Clearly Microsoft and Nvidia, continues to be the outstanding AI beneficiary. Nvidia especially reported again numbers showing that the Company is growing faster than any other big cap company (1Q sales were +262% yoy with further margin expansion). Nvidia is continuing to trade at very reasonable multiples, below its 5y average at 34x P/E vs the average of 5y at 40x.

Is investor euphoria for these companies waning or do they still have a strong run on the stock market?

Post one year and half of strong outperformance of the big Tech, investors started to scout upside in other Tech names, hoping for a broadening of the AI narrative, looking at the so called “AI adopters”. This is also in a context in which, especially starting from the 2H24 the comps will be more difficult for the big seven. Nevertheless, if we have seen some catch up of performance of other stock, the market is still concentrated on the seven for their superior EPS growth expected. Moreover, in a context of scarcity of growth in the rest of the market, the concentration is expected to remain sticky on this Companies that represent also good Quality factor given their balance sheet strength. This confidence in the future is reflected also in the announced buy backs and dividend increase: Apple increased the buyback authorization to $110 bn (vs $90 bn year ago), Nvidia just raised the quarterly dividend by 150% announcing also a stock split 10:1 to help retail investors to invest in the Company.

Is it time to start differentiating between companies within this group? Are they a heterogeneous group or is the term "the magnificent seven" becoming meaningless? Should the number of companies be reduced?

We have started to see some differentiation with Nvidia continuing to exceed expectations, a significant bulk of companies in the middle, and Tesla and Meta increasing their volatility around news and results.

At the beginning of the year, some price correction in Apple (due to China I-Phone sales softening), Tesla (some price war concern on the EV) and Meta (higher capex) made some investors re-think of the number of the magnificent seven, with a possible reduction down to four/five.

I think that the Magnificent 7 will continue to outperform the rest of the market growth, but with a possible three speed: Nvidia continuing to be on the podium, a big chunk of companies in the middle, and Tesla possibly lagging behind. This is the reflection of the different combination of FY1 EPS growth expected and consequent 12m FWD P/E valuation: Nvidia expecting a more than 90% EPS growth for a 34x P/E is at the opposite level of Tesla -18% EPS growth expected for a 65x P/E.