Where Is Gold Headed? Navigating Geopolitical Tensions and Economic Scenarios

9 NOV, 2023

By Nitesh Shah from WisdomTree

By Nitesh Shah, Head of Commodities and Macroeconomic Research, WisdomTree

As we go to publish this outlook, gold has clearly been given a lift from geopolitical stress. The war between Israel and Gaza has driven many to search for safe-haven assets and gold is a top

contender.

However, in the weeks leading to this publication, gold was getting flanked by the twin headwinds of an appreciating US Dollar and a bond sell-off. Gold held relatively well against such pressures but began to wilt, with the 50-day moving average (DMA) price falling below the 200-dma toward the end of September. That is what technical analysts call a “death-cross”. However, despite its ominous name, that technical marker often signifies a new base. And true to that, gold has rebounded significantly, despite those bond and currency headwinds intensifying.

While we don’t know how prolonged or severe the war will be, destabilisation in the Middle East

serves as a reminder that geopolitical, financial or economic stress can flare up at any moment and

the best time to have an ‘insurance asset’ is before the event takes place. Gold is thus a valuable

strategic asset.

While institutional demand for the metal has been muted for months, retail demand, especially in

China and Turkey, is very strong. Central banks have also been very active in the gold markets this

year and we don’t expect that trend to subside. Although demand in those pockets maybe seems

like a reaction to localised concerns, we believe that globally, institutional investors are likely to be

increasingly concerned about global risks – geopolitical and financial – and seek more hedging tools.

We acknowledge that the fight for institutional investor attention is going be difficult when

defensive assets like US Treasuries are proving a yield (to maturity) of over 5% on the 2-year and

close to 5% on the 10-year, compared the zero-yielding asset that is gold. However, gold has proven to be a very effective hedge against financial, geopolitical, and inflationary risks. While many thought that inflationary risks were under control a few weeks ago, a resurge in energy prices has led many to question that assumption (and once again should support the demand for hedging instruments).

Geopolitics and gold

Gold is also viewed as a ‘safe-haven’ asset, meaning that during periods of economic uncertainty or heightened geopolitical risk, investors have historically turned to the precious metal for protection, pushing its price up. As such, gold can act like a form of portfolio insurance and help provide downside protection during market turmoil. Our analysis shows that when the Geopolitical Risk (GPR Index) has risen 1 standard deviation above its historic average (indicating heightened geopolitical tension), gold has risen 9% year-on-year (y-o-y) on average, while the S&P 500 Equity Index has fallen 8.6% y-o-y in those months 1. Figure 1 shows how gold has performed after a range of key financial and geopolitical events.

Figure 1: Gold’s performance after financial and geopolitical events

Source: Bloomberg, WisdomTree.

We stress that we don’t know how long or severe the current turbulence in the Middle East will be,

but historically gold has served a valuable hedging tool.

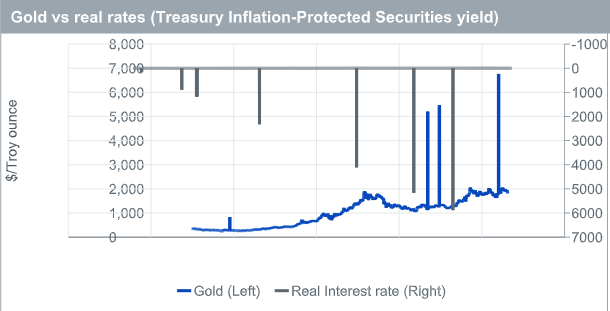

Bond markets and gold

Markets are expecting Federal Reserve (Fed) policy interest rates to be ‘higher for longer’. In

contrast to most rate cycles, when cuts start to come into play shortly after the last hike, bond

markets are expecting a long pause at the top. That has driven 10-year nominal Treasury yields to

the highest level since 2007 and real yields to their highest since 2008.

Gold, however, is holding its own, with the yellow metal continuing to defy the historic real yield-

gold relationships.

Figure 2: Gold vs. real rates (Treasury inflation-protected securities yield)

Source: Bloomberg, WisdomTree. 30/01/1997 – 24/10/2023.

In past editions of our Gold Outlook, we have commented on bond yield curve inversions (10-year

yields below 2-year yields) and their predictive power of recessions. Gold tends to perform strongly

in recessions. The lag between an inversion and a recession can be long and usually more than a

year. We are at least 15 months into the current inversion, and we are not yet in a recession.

However, markets are jittery and expressing anxiety about what is to come. In recent weeks, the

yield curve has become less inverted. However, that shouldn’t be interpreted as a positive sign for

the economy. Firstly, historically we have seen yield curve inversion usually unwind around the time a recession starts.

Secondly in the past, most dis-inversions have occurred as a result of shorter yields (2-year yields) declining, in an event called “bull-steepening”. Right now, we are seeing the dis-inversion due to longer yields (10-year yields) rising. This “bear steepening” from an inverted curve is not very common. The very few past examples don’t offer us good insights into what that

means for the economy or gold.

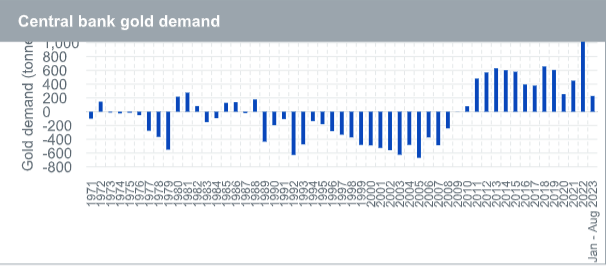

Central banks’ demand for gold

After hitting an all-time high in 2022, central bank demand for gold has maintained strong

momentum. Figure 3 shows annual official sector gold buying since 1971 and cumulative purchases in the first eight months of 2023. Between March and May 2023, Turkey’s central bank was selling gold into the domestic public markets to satisfy strong bar, coin and jewellery demand following a temporary partial ban on gold bullion imports. That ban was put in place to soften the economic blow from the earthquake in February 2023. Since the import ban’s reversal, the Turkish central bank has resumed a strong buying programme and we have seen three consecutive months of buying (June – August 2023 purchases of 43 tonnes). However, because of the sales, cumulative Turkish official sector flows were negative (January – August 2023 sales of 70.5 tonnes). We suspect Turkey will be very active in replenishing its reserves. The People’s Bank of China has reported 10 consecutive months of gold purchases, amounting to 217 tonnes, over November 2022 – August Prior to this period, China had not reported any purchases since 2019.

Figure 3: Central bank gold demand