Where we really are in the AI cycle

9 JUL, 2026

By Xuesong Zhao from Polar Capital

By Xuesong Zhao, Lead Fund Manager of the Polar Capital Artificial Intelligence Fund

Three and a half years after ChatGPT launched, it is tempting to assume the AI cycle is well advanced. We believe the opposite. In our view, 2026 looks less like the middle of the cycle than its beginning. This is the point at which AI moves from a productivity tool used by relatively few to a general-purpose technology that reshapes how work is organised, and where value is created, across every sector of the global economy.

The easiest way to underestimate AI is to mistake the interface for the capability. For most investors the mental model is still the chat window: a tool that drafts emails, summarises documents and writes code. Those productivity gains are real, but anchoring to the current interface systematically underestimates both the scale of the underlying capability and the duration of the cycle ahead.

Consider the early decades of electricity. When the telegraph was commercialised in the 1840s, investors were right to be excited, but the telegraph was not the right preview of what electricity would become. It was one narrow application of a far more general capability and it gave little hint of the electric light, refrigerated food, the factory motor or the wholesale reorganisation of industries that followed. The most meaningful productivity gains from electrification also only arrived once factories were redesigned around distributed power, instead of bolting electric motors onto layouts inherited from the age of steam.

Today’s chat interface is the telegraph: a real but narrow use of the underlying capability. That capability – machine cognition that is becoming abundant and increasingly autonomous – is the electricity. Much of the value may accrue not to the technology itself but to the companies in every sector that reorganise around it, and that reorganisation has barely begun. This is why we believe the cycle is closer to its start.

The agentic inflection

The critical development of the past 12 months is the arrival of agentic AI that completes work autonomously across extended, multi-step tasks. Enterprises run on repetitive, complex workflows that are too involved for a single prompt yet do not need human judgement at every step. Unlike a chatbot, agentic AI can plug into existing systems and own these processes end to end.

The evidence is concrete. The length of task an AI agent can reliably complete has been doubling roughly every four months, from under a minute in 2022 to nearly 15 hours for Anthropic’s Claude Opus 4.8 today. Goldman Sachs estimates agentic AI could drive token consumption 24x higher than current levels. Google is processing 3.2 quadrillion tokens per month, a 330x increase in two years. This is an accelerating step-change in AI consumption that, in our view, the market continues to underestimate.

Still early in a long cycle

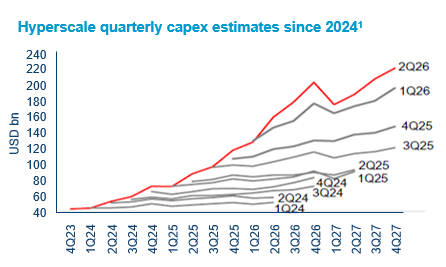

AI spending today represents approximately 1% of global GDP. Historical precedent suggests peak intensity could reach 2-5% over a cycle lasting at least 5-10 years. Morgan Stanley sees a potential $10trn AI infrastructure buildout over the full cycle, roughly 10x the mobile and cloud capex of the previous era. Set against $44trn of knowledge worker expenditure and $60trn of corporate operating costs, today’s spending looks like an early instalment rather than a peak.

Frontier lab revenue trajectories make this viscerally clear. Anthropic’s annualised revenue run rate was $1bn 16 months ago and crossed $47bn in May 2026 – to our knowledge, the fastest B2B revenue ramp in the history of software. This is not being driven by speculation. NVIDIA’s Blackwell B200 GPU spot prices have nearly doubled in two months and leading labs are raising per-token pricing – this is a profile of a market where real demand is outrunning real supply. The structural case for the cycle to continue is compelling: scaling laws have held for over a decade, the cost of a given level of intelligence is falling by roughly 10x a year and AI is now beginning to accelerate its own development.

Our positioning

The Polar Capital Artificial Intelligence Fund is a global equity strategy with $4.2bn in assets under management, at 10 June. Approximately 40% of the portfolio is in the technology sector enabling AI; the remaining 60% is in industrials, consumer, materials and those non-technology sectors where AI is already driving measurable earnings change.

On the enabling side, the portfolio targets bottlenecks in the AI supply chain such as networking, high-bandwidth memory, thermal management and power infrastructure. On the other side sit companies being reshaped by AI in sectors far from technology. Delta Air Lines now prices around 20% of its ticket inventory algorithmically; Tesco is building a high-margin retail-media business on its data. Neither is a technology company, and that is the point.

Avoiding the losers matters as much as owning the winners. We sold the Fund’s entire exposure to business analytics and application software, around 17% of the portfolio, as AI progress raised the potential for enterprises to rebuild much of that functionality themselves, at a fraction of the cost. Software has long sat between people and their data; as compute increasingly initiates the transaction itself, that position is exposed.

The Fund offers disciplined exposure to all parts of the AI ecosystem, the enablers and the durable beneficiaries, backed by more than eight years of dedicated AI investing and over 1,000 company meetings a year. We believe AI will transform every sector and this will be one of the most compelling structural opportunities in global equities.

Past performance is not indicative or a guarantee of future results.

This is a marketing communication. For investment professionals only. For information purposes only. This material is not intended to provide advice of any kind. Issued by Polar Capital LLP and Polar Capital (Europe) SAS. Polar Capital LLP is authorised and regulated by the United Kingdom’s Financial Conduct Authority (“FCA”) and the United States’ Securities and Exchange Commission (“SEC”). Registered address: 16 Palace Street, London SW1E 5JD. Polar Capital (Europe) SAS is authorised and regulated by France’s Autorité des marchés financiers (AMF). Registered address: 18 Rue de Londres, Paris 75009, France. Some information contained herein has been obtained from third party source and has not been independently verified by Polar Capital. All opinions and estimates constitute the best judgement of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital, and may not be achieved.