Which areas of US equities perform best when interest rates start to fall?

25 SEPT, 2024

By Tina Fong

After the Fed announced a half-point rate cut and with further rate cuts likely in the coming months, Tina Fong, Strategist at Schroders & Ben Read, Schroders economist analyse which sectors and styles of equities tend to perform well after the first rate cut.

By: Tina Fong, Strategist at Schroders & Ben Read, Schroders economist

Historically, as US inflation approaches the Federal Reserve's (Fed) 2% target, momentum and technology stocks have generally performed more robustly.

However, it is important to note that this is only one element of the overall picture. Falling inflation gives the central bank room to cut rates. Indeed, typically a year after the Fed's first rate cut, US equities have posted double digit returns. At the same time, the growth environment matters especially when recessions lead to a more aggressive rate easing cycle.

Given that interest rates are likely to fall in the coming months, which sectors and styles of the stock market tend to do well after the first rate cut?

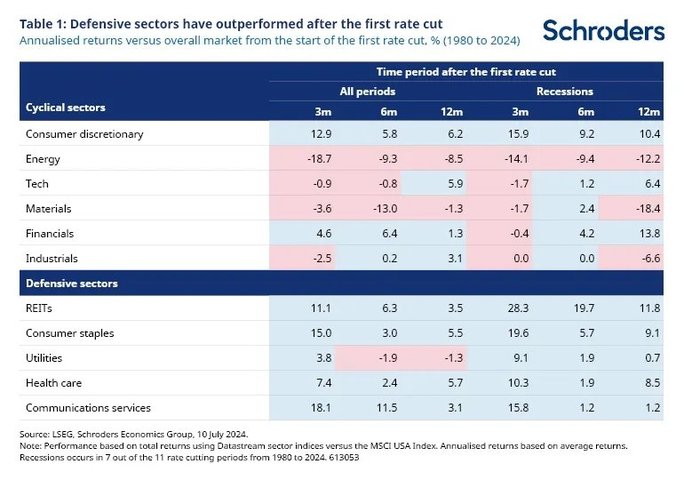

Defensive sectors tend to outperform their cyclical counterparts.

To analyse sectors, we have grouped them into cyclical and defensive sectors based on their sensitivity to the global market. For example, cyclical sectors, such as technology, tend to outperform when the market rises, but also underperform when the market falls.

Table 1 shows that defensive sectors have tended to outperform their cyclical counterparts after the first Fed rate cut. This is especially evident during recessions, probably because investors seek market sectors that are more likely to withstand a weaker growth environment and benefit from more aggressive rate cuts.

However, most cyclical sectors tend to perform poorly in the three months following the first rate cut, especially when it occurs during a US recession. However, one year after the start of the easing cycle, cyclical sectors tend to offer higher returns.

Initially, cyclical sectors sell off following rate cuts, probably in response to a backdrop of weaker growth and inflation. But at some point, these areas of the market become attractive, as valuations of these assets become cheaper and investors expect rate cuts to boost economic activity and corporate earnings. That said, the financial and consumer discretionary sectors have been the exceptions, as they have generally performed well even in the first few months after the first rate cut.

The technology sector, curiously, performs worse than the broader market in the first few months after the rate cut. But its performance has been negatively skewed by the large sell-off that occurred during the tech bubble recession in the early 2000s. If we ignore the period, technology stocks tend to have positive returns when rates are cut.

How do equity styles perform during rate cut cycles?

The ‘momentum’ style has, on average, been the best performing sector of the market during past rate cuts (table 2). These stocks have performed very well prior to the rate cut cycle and the rebound in investor confidence after the first cut will only add to that performance.

To a lesser extent, quality and growth stocks have generated positive returns during rate cut cycles. This is consistent with our previous analysis on how well these equity styles perform in a low inflation environment. Growth, quality and momentum stocks perform worse when the rate easing cycle occurs in a recessionary environment. This could be because investors rotate towards the more defensive areas of the market, such as the minimum volatility (min vol) style.

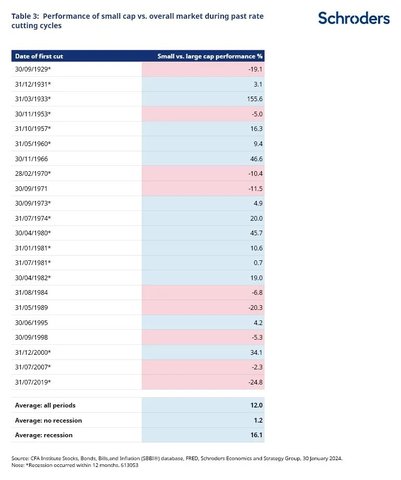

Even small caps tend to do well after the first rate cut during recessions. Small caps may benefit from the more aggressive rate cuts that occur in recessions. However, it should be noted that our analysis depends on the time horizon. For example, analysis of small-cap companies since the 1920s shows that in most cases they have outperformed the market one year after the first rate cut (table 3).

But after the mid-1980s, small caps have typically performed worse than the broader market after the first rate cut (this is the initial period of our analysis). The difference is probably due to changes in the sectors that make up the small-cap universe, where the proportion of financials and real estate has increased and exposure to technology and consumer discretionary has been reduced. Clearly, sector exposures in equity styles are dynamic and the investment manual of the past is no guarantee of future performance.

Conclusion

Given our expectation that there will be no recession in the US and following the Fed's rate cut announced last week, momentum, growth and quality stocks are likely to outperform. This conclusion is consistent with our analysis of these equity styles in a low inflation environment. At the same time, defensive sectors, relative to their cyclical counterparts, are also likely to do well in a falling rate environment.