Why global quality growth looks compelling again

Updated:

26 JUN, 2026

By Ryan Rajkumar from ECP Asset Management

Global equity fund flows in Europe started strongly in 2026 as confidence returned on the back of falling inflation which enabled the ECB to pivot interest rates toward 2%. However, March brought a sell-off following nervousness over high AI capex, steep valuations and of course, the conflict in Iran. Rather than a wide-scale sell-off, this was characterized by a rotation away from tech-heavy areas of the market, such as global large-cap growth, US large-cap growth and technology funds, into global large-cap blend funds, with a mix of value and growth exposures, as well as investors sitting on uninvested cash.

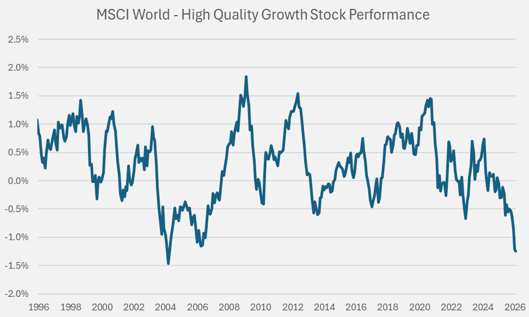

Jared Pohl, Co Founder and Portfolio Manager at ECP Asset Management, a global quality growth manager, argues the sharp sell-off in Quality Growth that we experienced over the last year creates a rare, highly attractive entry point, as history suggests once Quality Growth rebounds, it tends to considerably outlast the drawdown that preceded it.

High Quality Growth has sold-off aggressively

Historical precedent suggests that quality outperformance will mean revert

Indeed, the team's view is that virtually all sub-categories within the quality segment have been under simultaneous pressure, while earnings across our global quality growth portfolio have held up with minimal earnings downgrades. This has been evident within the Technology space for instance.

Technology Re-Rate provides Opportunities

Our portfolio consists of three buckets of tech exposure - Payments, Software and General Technology - all have sold off in recent months. As sentiment shifts, there is selective upside. We see the best upside potential across payments and software names in particular.

Pohl feels that the de-rating has been more sentiment-driven rather than fundamental and that the portfolio's low sensitivity to rising input costs and a potential consumer slowdown provides additional resilience.

Low Energy Cost and Low Consumer Sentiment exposure

60% of the portfolio has a very low exposure to direct and indirect energy costs and other cost increases. Those that are exposed have considerable pricing power to help offset these costs.

70% of the portfolio has a low exposure to the impact of a slowdown in consumer confidence and spending. Some portfolio companies that have very high brand qualities have been able to withstand a slowdown – Ferrari and Deckers Outdoor Corp being examples here.

Another reason for optimism within the quality growth space can be evidenced following the latest quarterly earnings season.

Visa’s share price was up around 8% following its Q2 result to levels last seen in mid-January on the back of revenue growth of 17% - its highest since 2013 - helped by a resilient global consumer spending environment and value-added services growth.

Raspberry Pi Holdings PLC continue to rally following strong full-year financial results. Arm Technology Investments also boosted its stake in the company to 13% through a secondary share sale. Meanwhile, memory shortages are leaving competitors unable to meet demand. Raspberry Pi is exploiting this gap by ensuring steady device supply for its industrial customers, placing the company in a prime position to grab major market share.

TSMC achieved a stellar 66% gross margin this quarter, cementing its role as the backbone of the AI economy. Despite rising electricity costs and global expansion hurdles, the company's outlook remains exceptionally strong. Driven by the ongoing surge in AI demand, management raised its full-year 2026 revenue growth forecast to over 30% and is launching its most aggressive factory expansion yet.

Three markets. Three compelling reasons to be there now

Annabelle Miller, Portfolio Manager at ECP, is currently visiting key stakeholders at a range of current and prospective portfolio companies in Taiwan, Korea and Japan for extensive discussions on what we believe are the picks-and-shovels of the AI revolution, which we hope will provide scope for further differentiated alpha-generation within our concentrated portfolio.

It is the ability to source differentiated ideas, with idiosyncratic factors borne out of a deep research-driven five stage committee-led investment process across a stable, collegiate team that sets our approach apart in an already crowded area of the global equity marketplace.