The enduring appeal of private equity

11 NOV, 2022

By Jaime Raga

Private equity and venture capital have entered a period of heightened uncertainty in 2022. With first quarter headlines dominated by Russia’s invasion of Ukraine, the focus has now turned to inflation and increased volatility of public equities which has knock-on effects for privately held companies. We expect these factors to persist in the coming quarters, particularly as the cost of debt (a key input for private-company transactions) increases with rising rates. Further, re-evaluation of acquisition pipelines at large public companies (strategic acquirors) contribute to a more uncertain exit environment for privately managed businesses. Investor demand for private equity products remains robust, but below the record-setting levels of 2021.

We believe we are now in the midst of a flight to quality with established, proven managers relatively unaffected in their ability to raise capital, while emerging managers and those with spotty track records will find it significantly harder to attract investor support.

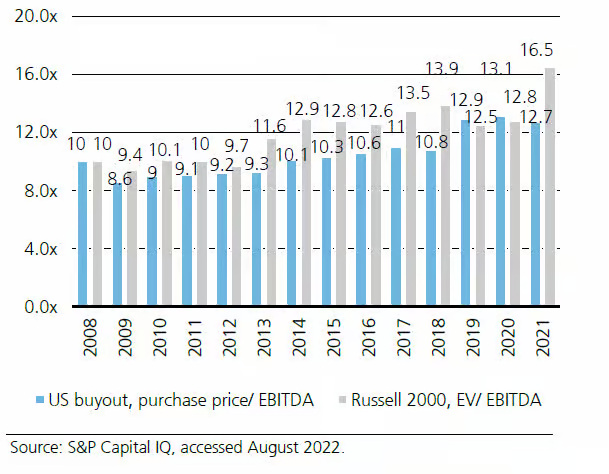

Existing private equity investments are facing these headwinds as is the rest of the market, but we believe it is an excellent time to deploy capital into new private equity funds and investments. Highlighting the relative attractiveness of the asset class, buyout EV/EBITDA multiples (the multiple of earnings a sponsor pays to acquire a company) in the US market are below the public market comparables as of 2021 (see Figure 1). Moderating entry multiples and purchase prices at the outset make companies a relative bargain for newly raised funds, and an investor committing to private equity today can expect their capital to be deployed over the next several years, quite possibly in a more attractive environment than we see today.

US buyout multiple growth has leveled off (median US multiples, buyout entry multiples and small-cap equities, 2008-2021).

Below, we look at the outlook for the most prominent private equity strategies:

Buyouts

Private company buyouts, the core of private equity, have slowed into 2022 in line with broader markets. In addition, private equity sponsors are exercising increased caution and pricing discipline in the face of concerns over global economic growth, supply chain disruptions, and the company-level impacts of inflation. Fund investors are also becoming more conservative, focused on investment pace as many funds have been fully deployed in two years versus the longer-term average of three-to-four years. We are approaching the current market environment with a focus on quality and an emphasis on by fundamental growth rather than arbitrage or financial engineering, seeking segment-leading business models with conservative leverage which are benefitting from macro trends including industry consolidation, new technologies, and demographic shifts. Further, in complex sectors such as healthcare, we continue to favor specialist investors with particular expertise in their narrower verticals.

Growth equity

Sitting between buyout and venture capital, growth equity investments are experiencing many of the difficulties of both early-stage and mature companies. High growth is commanding a lesser valuation premium than in recent years, raising the cost of capital for these companies which typically do not have balance sheets as robust as those of more mature companies. Exit paths may be constrained, and growth rates reduced in order to conserve capital. While we are convinced

of the staying power of growth equity, we have seen fundraising slow and believe a more cautious approach supporting proven managers is prudent in the near term. This includes a greater focus on companies that are break-even on a cash flow basis which could self-sustain with limited ongoing capital support in case of a protracted economic cycle.

Venture capital

Venture funds are facing outsized valuation volatility due to their outsized exposure to early stage, pre-profitability and technology-sector companies. The pace and enthusiasm for greater funding rounds at higher valuations has slowed, and many venture managers are encouraging companies to focus on cash conservation and balance sheet stability, a notable departure from the growth-at-any-cost modus operandi of the past decade. Such cost containment measures include curtailing hiring pace and marketing spend (a reversal of offering customer acquisition incentives that frequently drove growth at negative marginal unit economics). This will lead to a noticeably slower pace of growth for all but the best venture-backed companies, but should also mean that companies successfully scaling the growth curve will on average be more stable and less volatile. Public markets, often an exit route for venture-backed companies, are currently less hospitable than in quarters past led by a more cautious investor sentiment. However, when investor sentiment reverses, there may be pent-up enthusiasm and a flurry of IPOs for companies successfully navigating today’s market.

Private equity market developments

Private equity as an industry and asset class continues to grow rapidly. According to Mckinsey’s 2022 private markets annual review, it is the most-invested alternative among institutional investors, 60% of whom report having an allocation to private equity funds (including fund-of-funds). Of institutional investors surveyed by Preqin, an alternatives market research and data manager, over 50% reported an intention to increase their allocation to private equity over the longer term, compared to just 5% who intend to reduce it. It is then not surprising that growth equity and venture capital hit record fundraising levels in 2021 (see Figure 2), while private equity AUM reached a record high (see Figure 3). We do expect a pullback in fundraising in the near term as many capital raises were brought forward into 2020-2021 by the favorable market environment. Funds are now taking longer to raise, especially for less established sponsors or those that have had performance stumbles in recent years. Deal activity similarly remains elevated in 2022 but could come in under the record-setting pace of the past few years as sponsors re-assess deployment pace and reset pricing discipline in anticipation of a more volatile few quarters ahead. Availability of leverage can also constrain dealmaking as greater amounts of equity are required to complete each transaction.

Growth and VC hit record fundraising levels in 2021 (Global private equity fundraising by asset sub-class, USD billions)